- HUD is expanding beyond traditional affordable housing financing into workforce and middle-income multifamily projects serving households earning up to 120% of area median income.

- Walker & Dunlop’s 2026 HUD Outlook report says faster processing timelines and revised environmental policies are improving FHA loan execution and lowering costs.

- The shift positions HUD as a larger player in multifamily capital markets as elevated construction costs and refinancing demand reshape development economics.

Multihousing News reports that HUD is becoming a bigger force in multifamily finance as developers and owners look for stability in an uncertain lending environment. According to Walker & Dunlop’s “2026 HUD Outlook” report, policy updates and operational improvements are pushing the agency beyond its traditional affordable housing niche and into workforce and middle-income housing finance.

The timing matters. Elevated borrowing costs, tighter construction lending, and looming loan maturities are forcing developers to rethink capital stacks. HUD-backed financing, once viewed as cumbersome or limited in scope, is increasingly appealing because of its long-term fixed-rate structure and government-backed certainty.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Broader Multifamily Mandate

Walker & Dunlop says HUD now supports housing serving residents earning up to 120% of area median income (AMI), expanding the agency’s reach into workforce housing. That change addresses one of multifamily’s fastest-growing pressure points: renters who earn too much for subsidized housing but still struggle with market-rate rents.

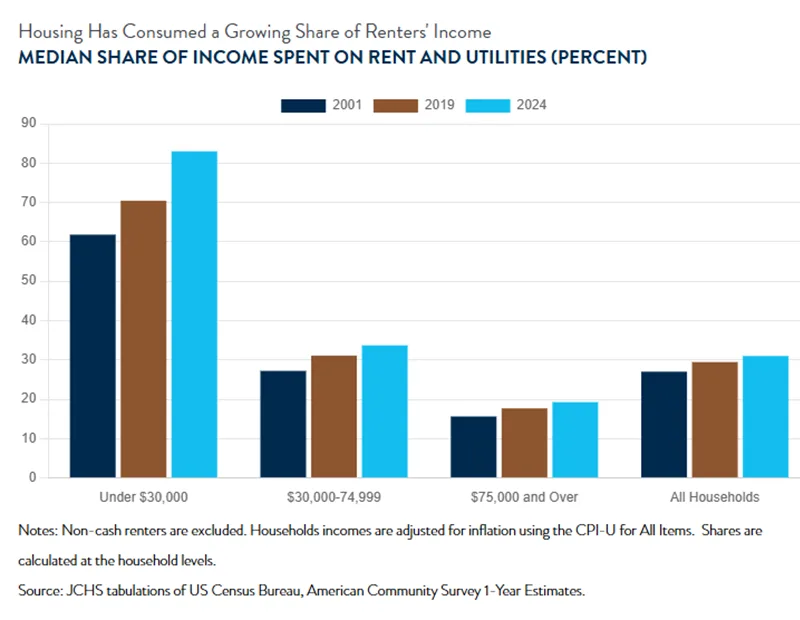

The affordability squeeze has intensified in recent years. According to Harvard’s Joint Center for Housing Studies data cited in the report, 48.7% of households earning between $45,000 and $75,000 were cost-burdened in 2026, up from 39.2% in 2019 and 24.4% in 2001. Developers targeting middle-income renters are also facing elevated construction costs, labor shortages, and higher equity requirements that continue to suppress new supply.

The Details

Walker & Dunlop’s report highlights several operational changes inside HUD that are improving FHA-insured multifamily loan execution. Processing timelines have shortened. Underwriting now focuses more heavily on risk. HUD also scaled back environmental review requirements to reduce costs and improve certainty.

HUD reinstated prior guidance on buried pipelines and fall hazards. The agency also narrowed noise analysis requirements. In addition, it reduced standards tied to high-voltage transmission lines and vibration reviews. Walker & Dunlop says those changes remove some third-party reports. They also align HUD’s environmental review process more closely with conventional financing standards.

HUD is also promoting modular construction to improve affordability and shorten development timelines. Walker & Dunlop says the agency views modular delivery as a way to reduce construction risk. The approach could also improve project feasibility in today’s high-cost environment.

HUD is also considering revised build-to-rent guidance. The changes would allow new developments to qualify for financing support. Recently completed rental communities could also qualify if they are less than three years old.

Why Workforce Housing Is Drawing Capital

Multifamily developers are increasingly favoring long-term debt over floating-rate and short-duration loans. Many owners refinancing maturing debt want protection from future rate volatility. Elevated borrowing costs and tighter bank lending continue pressuring capital markets.

As a result, government-backed lending is taking on a larger role in multifamily finance. Historically, affordable housing specialists relied most heavily on HUD financing. Now, Walker & Dunlop says the agency is becoming “a core component of sophisticated capital strategies” for more institutional and private developers. That shift comes as policymakers also continue adjusting multifamily incentives and insurance structures to improve financing accessibility across the housing market.

The opportunity is especially significant in workforce housing. Demand continues outpacing supply across many Sun Belt and high-growth metro markets. CBRE’s 2026 multifamily outlook showed the strongest renter demand in middle-income segments. At the same time, high development costs continue limiting new supply.

Why It Matters

HUD’s growing role could provide an important liquidity source for multifamily developers at a time when traditional construction and permanent financing remain selective. Lower-cost, long-duration debt may help projects move forward that otherwise struggle to pencil under current market conditions.

The shift also reflects a broader evolution in housing policy. By extending financing support deeper into workforce housing, HUD is acknowledging that affordability challenges now reach well beyond low-income households. That could expand the pipeline for middle-market multifamily development while helping stabilize financing availability during a slower construction cycle.

What’s Next

Developers and lenders will be watching whether HUD can continue improving processing efficiency while scaling loan volume. Market participants are also monitoring potential expansion of build-to-rent eligibility and additional modernization efforts tied to environmental reviews and underwriting standards.

If interest rates remain elevated through 2026, HUD-backed financing could capture a larger share of multifamily originations, particularly for workforce housing and projects seeking predictable long-term debt execution.