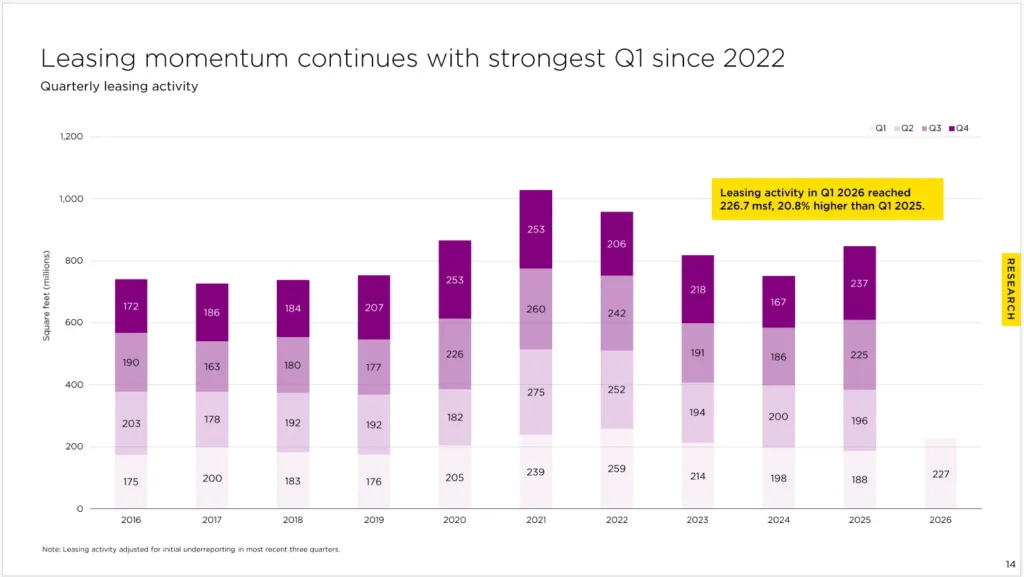

- US industrial leasing reached 226.7M SF in Q1 2026, marking the sector’s strongest first quarter since 2022, according to Savills.

- Vacancy held at 8.2% nationally as developers delivered less new supply and tenants resumed leasing larger blocks of space.

- Rising oil prices tied to the war in Iran could pressure occupier demand, creating a new risk factor for the industrial recovery.

The Commercial Property Executive reports that industrial demand is showing signs of stabilization after two years of softer leasing activity and elevated vacancies. According to Savills’ Q1 2026 industrial report, tenants leased 226.7M SF during the quarter, up 20.8% from a year earlier and the strongest first-quarter performance since 2022.

The rebound comes as the sector works through a massive wave of post-pandemic supply. While absorption remained positive, new leasing demand has yet to meaningfully compress vacancy levels nationally. Savills researchers say improving fundamentals and slowing development activity could finally shift the balance later this year.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Post-Pandemic Reset

Industrial landlords spent much of 2024 and 2025 absorbing the consequences of the pandemic-era construction boom. Developers raced to meet surging ecommerce and logistics demand during 2021 and 2022, pushing deliveries to record levels across Sun Belt markets.

That pipeline is now cooling. Savills reported 63M SF of industrial completions in Q1 2026, down sharply from 98.1M SF during the same period in 2025. Total space under construction also fell to 273.7M SF from 305.9M SF year over year.

At the same time, leasing activity is regaining momentum. Savills noted that tenants are once again pursuing larger blocks of space, helping sustain positive net absorption despite softer economic conditions.

The Leasing Rebound

National industrial vacancy stood at 8.2% in Q1 2026, unchanged from the previous quarter but up from 7.8% a year earlier, according to Savills. The flat reading suggests demand growth is finally catching up to the pace of new supply deliveries.

Savills Vice President and Head of Industrial Research Mark Russo said the leasing recovery is notable given ongoing macroeconomic pressure, particularly rising energy costs linked to the war in Iran. Russo also noted that negotiating leverage varies widely depending on geography, portfolio composition, and building size.

The report predicts vacancy should gradually decline over the next 12 months as completions slow further and absorption improves.

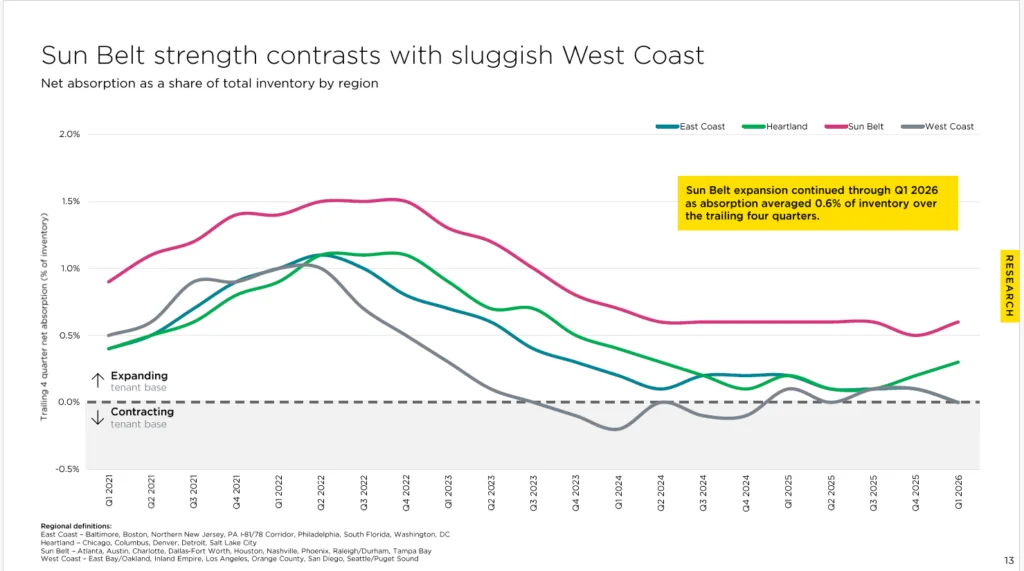

Sun Belt Industrial Markets Still Lead

The Sun Belt remains the industry’s primary growth engine, even if demand has normalized from pandemic peaks. Markets including Atlanta, Austin, Dallas-Fort Worth, Houston, Nashville, and Phoenix posted absorption equal to roughly 0.6% of inventory during Q1, more than double the pace seen across Midwest markets, according to Savills.

Houston led the nation in development activity with 22.9M SF under construction during the quarter. Dallas-Fort Worth followed with 18.8M SF underway, while Atlanta ranked third at 17.7M SF.

Coastal markets remained comparatively sluggish, with both East Coast and West Coast metros recording limited absorption during the quarter.

Ecommerce and Manufacturing Support Demand

Despite concerns around energy prices, industrial real estate continues benefiting from several structural demand drivers. Ecommerce penetration resumed growing after slowing in recent years, reaching 16.6% of total US retail sales in Q1 2026, up 110 basis points over two years, per Savills.

Amazon’s US logistics footprint also surpassed 500M SF in 2025 for the first time, underscoring the scale of long-term warehouse demand. For comparison, Savills noted the entire Chicago industrial market totals roughly 1B SF.

Manufacturing investment is also accelerating. According to the report, investors deployed $60B into US manufacturing projects in February 2026, more than double the level recorded a year earlier. Some of that demand will flow into build-to-suit projects, but it could still provide additional support for industrial occupancies nationwide.

Why It Matters

The industrial sector appears to be moving past its supply-driven slowdown, but the recovery remains uneven. Developers are finally pulling back on speculative construction while occupier demand improves, a combination that could stabilize rents and vacancies heading into 2027. That shift is also changing how landlords structure deals, with more tenants negotiating flexible lease terms as trade and tariff uncertainty reshapes supply chain planning.

Still, rising oil prices create a meaningful wildcard. Savills noted that periods of elevated energy costs historically correlate with weaker industrial demand, particularly for transportation, logistics, and distribution users sensitive to shipping expenses.

What’s Next

Industrial fundamentals will likely hinge on whether leasing momentum can outpace economic uncertainty during the second half of 2026. Market watchers will be tracking oil prices, manufacturing investment, and ecommerce growth closely as landlords attempt to regain pricing power.

If construction activity continues slowing while absorption remains positive, the sector could enter 2027 with tighter vacancies and healthier fundamentals than many expected just six months ago.