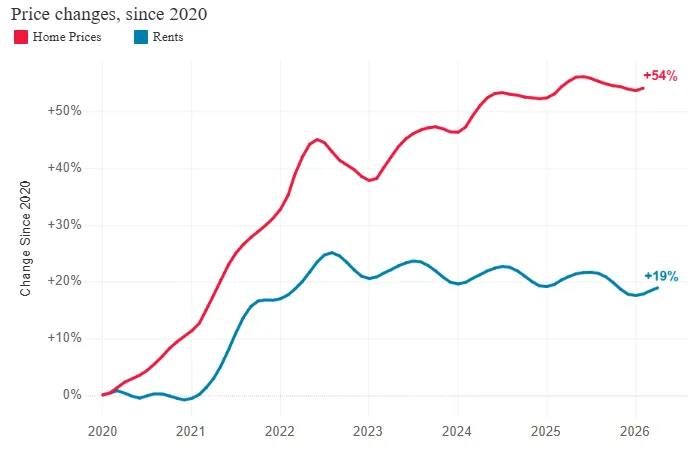

- Home prices increased 54% nationally between January 2020 and January 2026, while apartment rents rose just 18%, according to Apartment List and Case-Shiller data.

- Miami posted the strongest gains across both categories, with home prices up 77% and rents rising 33% over the six-year stretch.

- The widening disconnect between ownership and rental costs signals shifting affordability pressures and could influence future multifamily demand and investment strategies.

A widening gap between home prices and apartment rents is redefining housing economics across the US. New research from Apartment List shows that for-sale housing values have substantially outpaced multifamily rent growth in every major metro since the start of the pandemic, creating a disconnect that continues to shape affordability, renter behavior, and investment decisions.

Between January 2020 and January 2026, national home prices climbed 54%, according to the Case-Shiller National Home Price Index. Over the same period, Apartment List’s national rent index showed rents rising just 18%. The divergence reflects dramatically different market dynamics between the ownership and rental sectors over the past six years.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Source: Apartment List

Pandemic-Era Demand Shifts

The split traces back to two major turning points in the housing market. First came 2020, when the onset of COVID-19 temporarily froze many urban rental markets as remote work, migration trends, and historically low mortgage rates accelerated demand for single-family homes. Buyers rushed into suburban and Sun Belt markets, pushing prices sharply higher.

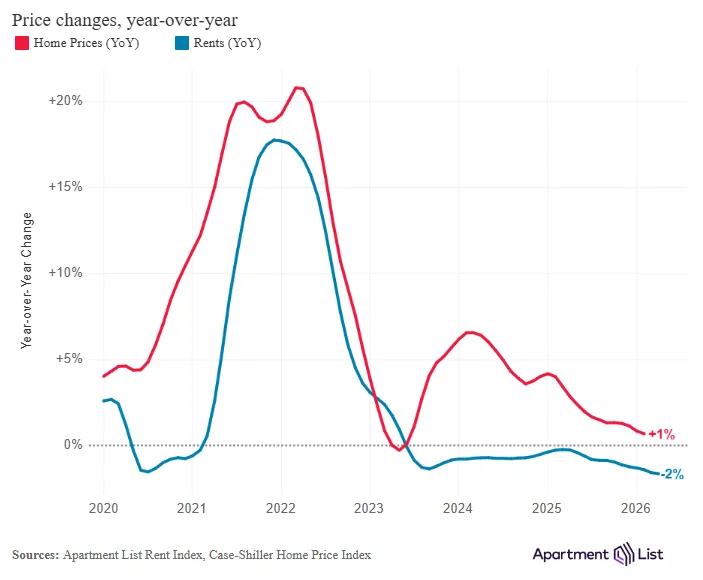

The second inflection point emerged in 2023, when a wave of multifamily deliveries hit the market. Developers completed a record number of apartment units nationwide, particularly in high-growth metros, leading to softer rent growth and, in many markets, outright rent declines. Apartment List noted that rent growth has remained negative since that supply surge began.

The Details

The data compares “same-store” home price and rent indices nationally and across 20 major metros, helping control for changes in housing stock composition over time. The analysis combines Case-Shiller home price data with Apartment List’s multifamily rent index.

Miami led the country in both categories. Home prices there surged 77% between January 2020 and January 2026, while rents rose 33%, the strongest rent growth among tracked metros. Charlotte, North Carolina, recorded the largest spread between the two metrics, with home price growth exceeding rent growth by 51 percentage points.

The national figures illustrate how much more expensive homeownership has become relative to renting. While rents certainly rose during the pandemic era, home prices accelerated at a pace that far exceeded wage growth and pushed affordability to historic lows in many markets.

A Growing Affordability Divide

The disconnect between rent growth and home price appreciation highlights how different supply conditions have become across housing sectors. Multifamily construction accelerated rapidly following the pandemic, particularly in Sun Belt metros where population growth and investor demand fueled development pipelines. That supply wave has also helped improve renter affordability in several high-cost urban markets as asking rents soften and concessions increase.

For-sale inventory, meanwhile, remained constrained. Existing homeowners held onto low-rate mortgages secured during 2020 and 2021, limiting resale inventory and keeping upward pressure on prices. According to Freddie Mac’s 2025 housing outlook, the US continues to face a structural housing shortage despite elevated apartment deliveries.

The gap also reflects diverging capital market conditions. Institutional investors poured money into single-family housing during the pandemic-era boom, while apartment operators increasingly faced rent growth normalization as new supply entered lease-up phases.

Why It Matters

The widening spread between home prices and rents could reinforce renter demand over the long term. As ownership costs move further out of reach for many households, renting may remain the more financially viable option even as apartment supply expands.

That dynamic matters for multifamily investors evaluating future demand trends. Slower rent growth has pressured apartment valuations in some markets since 2023, but sustained homeownership affordability challenges could create a longer runway for renter retention and household formation in multifamily properties.

The data also underscores regional divergence within the broader housing market. Sun Belt metros like Miami and Charlotte continue to experience outsized pricing pressure despite substantial apartment development, suggesting population growth and migration trends remain powerful demand drivers.

What’s Next

The trajectory of both home prices and rents will likely depend on interest rates, new housing supply, and broader economic conditions through 2026. Multifamily completions are expected to slow after the current development cycle peaks, which could stabilize rent growth in many markets.

At the same time, elevated mortgage rates and limited housing inventory continue to constrain home affordability. If ownership remains financially inaccessible for large segments of renters, apartment demand could stay resilient even in markets where rents have softened.

For CRE investors and operators, the key question is whether the current affordability gap becomes a temporary post-pandemic distortion or a longer-term structural feature of the US housing market.