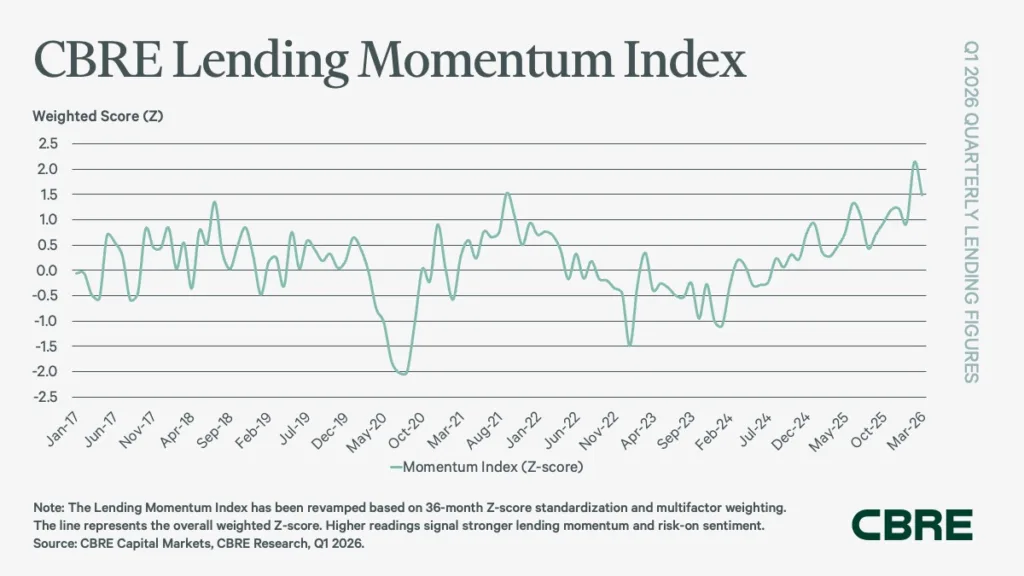

- CBRE’s Lending Momentum Index rose to 1.5 in Q1 2026, marking the strongest commercial real estate lending environment in five years.

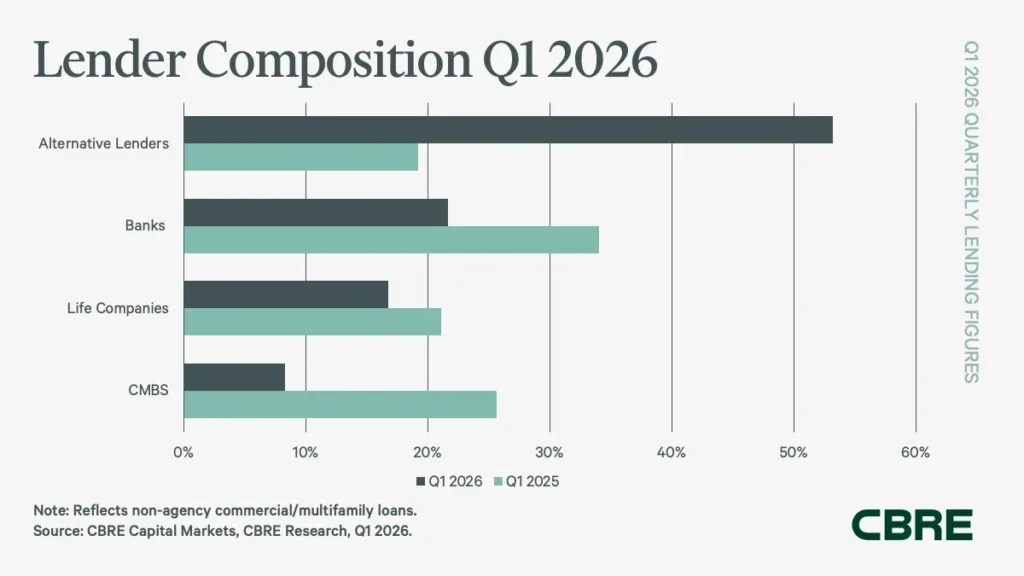

- Alternative lenders captured 53% of non-agency loan closings as debt funds sharply increased origination activity and average loan sizes grew 14% year over year.

- Lower spreads, rising loan-to-value ratios, and stronger agency multifamily lending point to improving liquidity conditions across CRE capital markets.

Commercial real estate lending activity continued its rebound in Q1 2026, reaching its highest level since 2021 as lenders loosened underwriting standards and deal flow accelerated. According to CBRE’s latest Lending Momentum Index, stronger acquisition activity, recapitalizations, and increased liquidity helped push lending sentiment sharply higher across the market.

The CBRE Lending Momentum Index—which tracks the pace of US commercial loan closings originated by CBRE over a rolling 36-month period—rose to 1.5 in Q1 2026. That compares with 1.2 in Q4 2025 and just 0.3 a year earlier, signaling a materially healthier lending environment after several years of elevated rates and tighter credit conditions.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Rebound Years in the Making

Commercial real estate lending has spent the past two years working through higher interest rates, declining property values, and refinancing stress tied to maturing debt. Many lenders, particularly banks, pulled back exposure during 2023 and 2024 as regulators increased scrutiny around CRE portfolios.

Conditions began improving in late 2025 as transaction activity picked up and borrowers adjusted pricing expectations. CBRE said rising acquisition volumes and fresh equity entering the market have helped improve price discovery and rebalance lender balance sheets. The firm also noted that recapitalizations and joint venture financings remain active, especially for larger institutional assets.

The Lending Details

Average commercial loan sizes increased 14% year over year in Q1 2026, according to CBRE. At the same time, commercial mortgage spreads tightened modestly, declining 2 basis points annually to 181 bps for fixed-rate loans with 55% to 65% loan-to-value ratios. Multifamily spreads fell even further, dropping 13 bps year over year to 136 bps.

Borrowing costs also eased meaningfully. Average mortgage interest rates declined 110 bps quarter over quarter to 5.7%, while loan constants fell to 6.7% from the previous quarter’s level, per CBRE data. Debt yields remained relatively stable at 9.5%, compared with 9.8% in Q4 2025.

Lenders also showed slightly greater risk tolerance during the quarter. Average commercial loan-to-value ratios climbed to 61.5%, up from roughly 59% a year ago, while multifamily LTVs increased to 67.2% from 65%.

Alternative lenders dominated non-agency lending activity in Q1. Debt funds and mortgage REITs accounted for 53% of CBRE’s non-agency loan closings, a sharp increase from 19% a year earlier. CBRE said debt fund lending volume alone surged 280% year over year.

Banks remained the second-largest lending source with 22% of non-agency volume, though that share fell from 34% a year ago. Life companies represented 17% of activity, while CMBS lenders accounted for the remaining 8%.

Alternative Lenders Take Center Stage

Private credit expanded rapidly across commercial real estate finance during Q1 2026. Meanwhile, banks continued managing regulatory pressure and tighter capital requirements. As a result, debt funds gained market share across bridge loans, recapitalizations, and acquisition financing for transitional assets.

The shift appeared most clearly in office and value-add multifamily deals. Borrowers increasingly sought flexible financing structures that banks often avoided. CBRE said alternative lenders now lead non-agency originations. One year ago, banks controlled that market segment.

Government-backed multifamily lending also strengthened during the quarter. Fannie Mae and Freddie Mac originations increased 35% year over year to $29.9B in Q1 2026. CBRE’s Agency Pricing Index showed average fixed agency mortgage rates falling 42 bps annually to 5.4%.

Why It Matters

The improvement in commercial real estate lending conditions suggests capital markets are stabilizing after a prolonged reset period. While lenders remain selective, tighter spreads, higher LTVs, and increased transaction activity indicate growing confidence around property valuations and refinancing prospects.

The resurgence of debt funds also highlights how CRE financing continues shifting toward private credit providers. That trend could reshape competitive dynamics across lending markets, particularly if banks maintain conservative underwriting standards through 2026. The shift also comes as office distress and looming maturities continue pressuring parts of the CMBS market.

For borrowers facing near-term maturities, the broader availability of capital may ease refinancing pressure that has weighed on the market since rates surged in 2022. Improved liquidity could also support more acquisitions as buyers and sellers narrow pricing gaps.

What’s Next

Market participants will be watching whether lending momentum holds through the remainder of 2026 as interest rate expectations evolve and transaction activity builds. A sustained recovery likely depends on continued stability in Treasury yields, stronger leasing fundamentals, and further improvement in property valuations.

Debt funds are expected to remain highly active, particularly in transitional and higher-yielding asset classes. Meanwhile, agency multifamily lending could continue gaining market share if borrowing costs remain favorable and housing demand stays resilient.

CBRE’s latest data points to a lending market that is no longer in defensive mode—but one that still remains disciplined as lenders balance growth opportunities against lingering risks in office and other challenged sectors.