- Single-Family Rental cap rates have increased by nearly two percentage points since 2021.

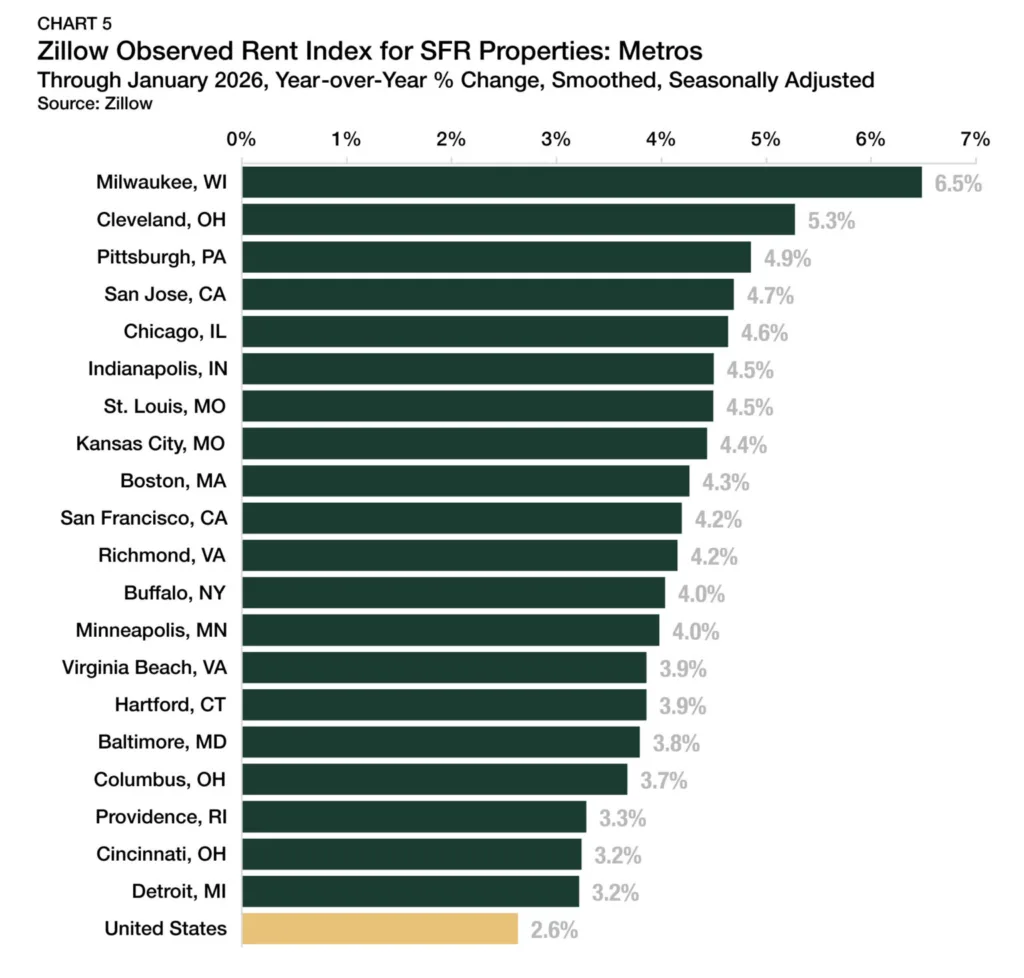

- National rent growth remains positive, with Midwest metros leading major markets.

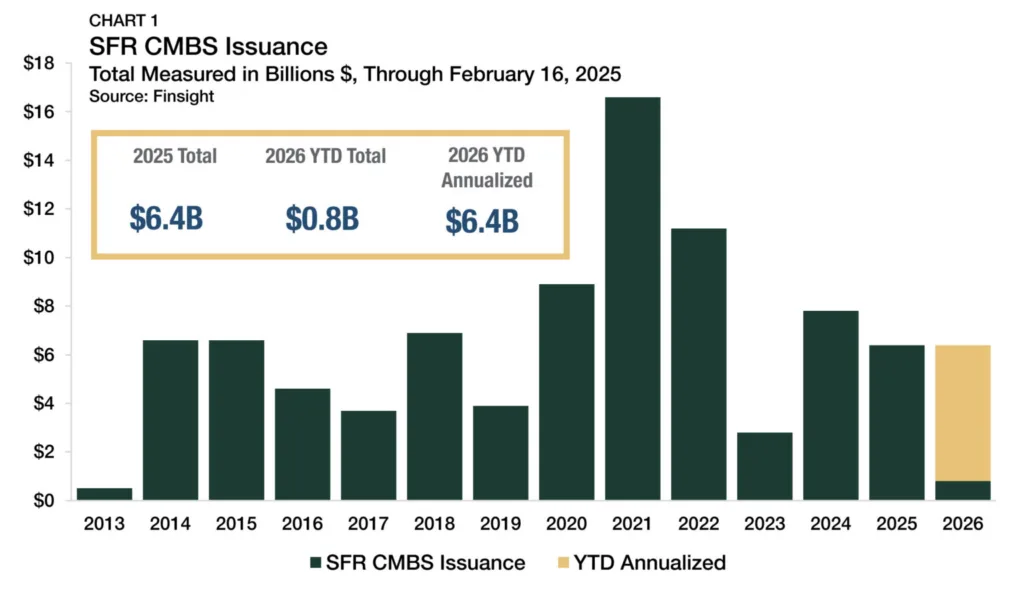

- SFR CMBS issuance and REIT acquisitions indicate normalized, disciplined capital markets.

- Build-to-rent construction is still above historical norms, supporting ongoing rental demand.

Resilient Market Performance

The single-family rental (SFR) sector sustained strong fundamentals in early 2026. Occupancies held near long-run averages as rent growth moderated from post-pandemic highs but remained steady. Home price appreciation slowed, yet property-level cash flow metrics were healthy. Arbor reports that elevated mortgage rates and low homeownership affordability continued to funnel demand into the SFR market, with SFR household counts reaching a seven-year high in 2025.

Capital Markets Adjust but Remain Active

SFR cap rates rose to 7.3% in Q4 2025, a 194 basis point climb since 2021, reflecting slower home price growth and normalizing rental gains. Despite this upward trend in cap rates, investor interest remained stable and investment volumes aligned with historical averages. This stability comes as more institutional buyers re-enter the market, drawn by improving yield profiles and disciplined pricing. Structured SFR capital markets settled into a more balanced pattern, with 2025 SFR CMBS issuance totaling $6.4B—slightly down from 2024 but in line with a normalized pace. Public SFR REITs registered their strongest net quarterly acquisitions since mid-2022, suggesting selective expansion as disposition activity receded.

Operational Metrics Remain Solid

Average occupancy for SFR properties was 94.0% in Q4 2025, nearly identical to pre-pandemic norms. National SFR rents increased 2.6% year-over-year in January 2026. In metro-level results, Midwest cities such as Milwaukee (+6.5%), Cleveland (+5.3%), and Pittsburgh (+4.9%) led growth, while Austin was the only major metro to post a decline.

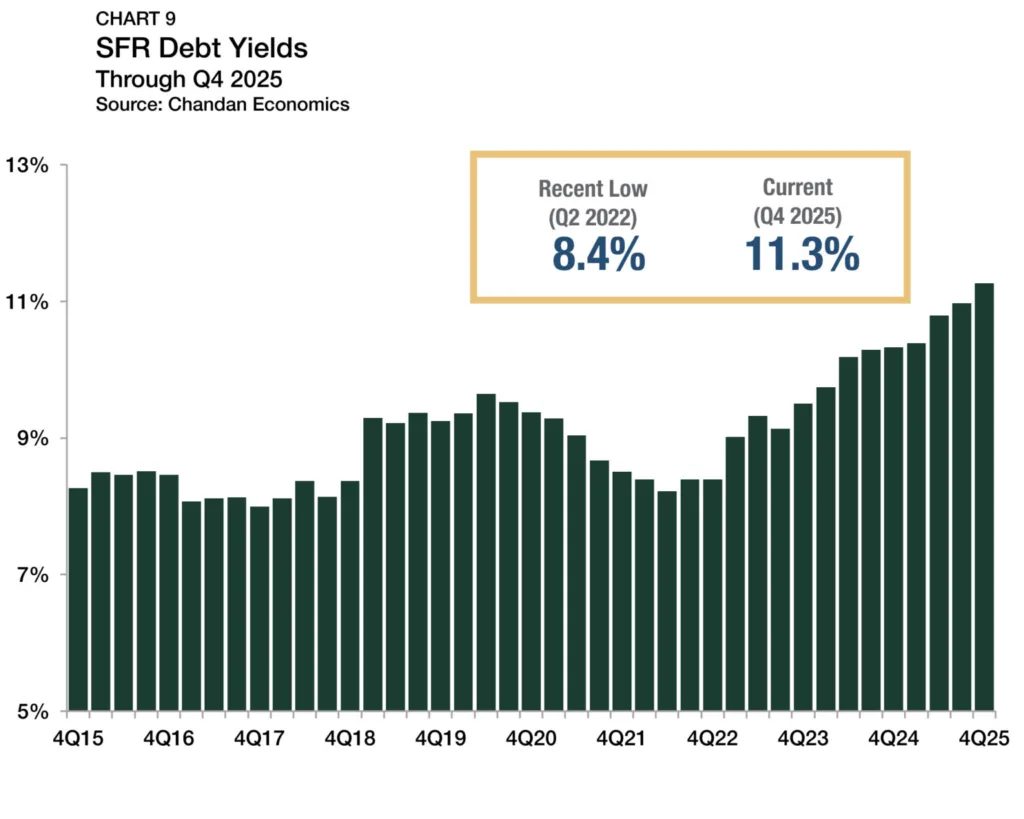

Credit, Risk, and Pricing Signals

Debt yields rose to 11.3% as lenders tightened standards and reduced leverage. Average loan proceeds declined from 2022 peaks but stayed accessible for established borrowers.

Meanwhile, residential mortgage delinquencies and SFR distress remained low. SFR delinquencies fell to 1.6% in October 2025, down from 2.1% a year earlier.

Build-to-Rent and Supply Trends

Build-to-rent (BTR) development continues at elevated levels. Around 69,000 BTR units were started in the 12 months ending September 2025, accounting for 7.2% of all single-family housing starts—well above pre-pandemic averages, even as growth cooled from recent peaks.

What’s Next

The outlook for single-family rental investment remains positive. Homeownership affordability challenges continue to limit buyer activity. At the same time, new construction stays below long-term historical norms. These conditions continue to support steady rental demand across many markets.

Key demand drivers remain firmly in place. Household formation continues to expand the renter base. Many households also prefer the flexibility of rental living. Together, these trends reinforce stability across the SFR sector through 2026 and beyond.

Interest rates may moderate, but they will likely remain elevated. Even so, market fundamentals continue to support the sector. As a result, single-family rentals remain a compelling investment option for many investors.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes