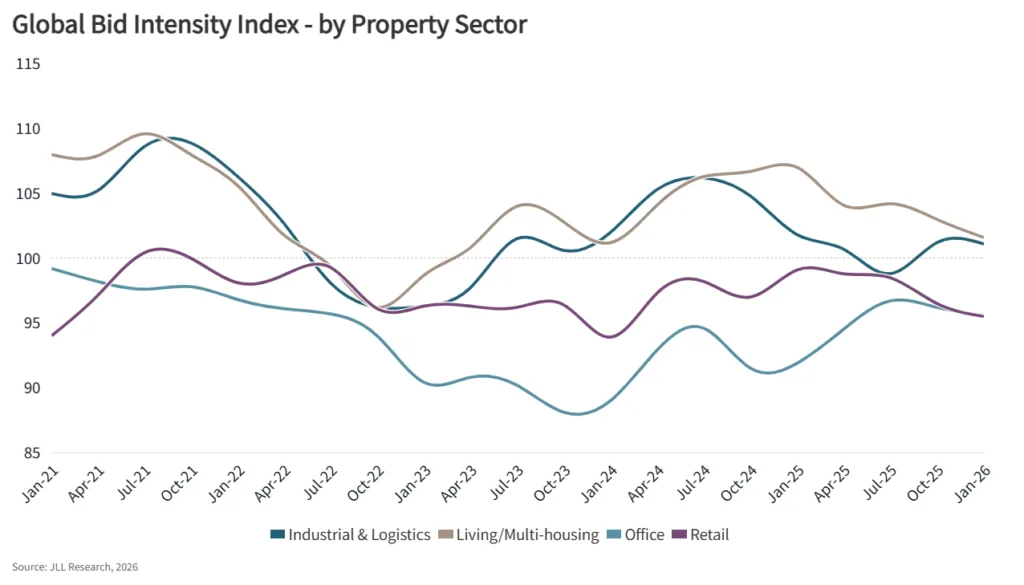

- Investor bidding intensity is converging across the four main property sectors.

- Bidding competitiveness has remained steady even as transaction volumes grow.

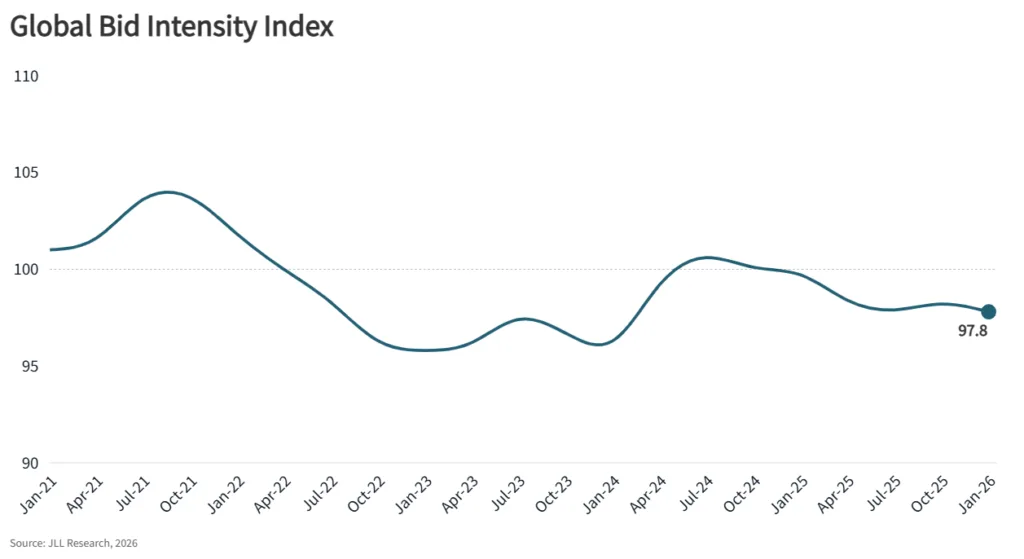

- The bid-ask spread is at its narrowest in over three years, signaling normalization.

- Sector trends reveal balanced competition and renewed liquidity.

Investor Momentum Holds Steady

Bidding intensity in global commercial real estate has remained robust despite a surge in available investment opportunities. According to JLL’s Global Bid Intensity Index, investor bidding competitiveness across Multi-family, Industrial & Logistics, Retail, and Office sectors has now narrowed to its smallest spread in more than three years. This signals a return to normalized market dynamics, even as the volume of deals on the market continues to expand.

Balanced Activity Across Sectors

The convergence of investor bidding intensity across all four main sectors marks a shift from the varied competition seen since late 2022. Multi-family still leads with the strongest bidding environment, supported by record amounts of investor dry powder, though softer rent growth in the US is impacting underwriting. This cooling in rent growth reflects a broader trend in the apartment market, where supply has recently outpaced demand in several metros, easing upward pressure on rents. Industrial & Logistics has seen a rebound in activity, while Retail’s broadening liquidity has resulted in a slight softening of competitiveness. Office, meanwhile, shows improving dynamics, with more buyers and lenders active compared to recent lows.

Market Drivers and Outlook

Strong sector fundamentals, stable interest rate policy, and gradually decreasing macroeconomic volatility are giving investors confidence to stay active. The narrowing bid-ask spread reflects greater pricing alignment among buyers and sellers, pointing to broadening investor appetites. While global uncertainties—such as ongoing geopolitical tensions—remain, the generally healthy economic backdrop is expected to drive an active and liquid capital markets environment in 2026. Investor bidding trends suggest a return to balanced, competitive dealmaking as more buyers embrace a diversified, risk-on approach.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes