- High vacancy rates and slowing net absorption are weighing on markets with elevated supply, particularly in the Sun Belt, where economic uncertainty and softened migration trends are magnifying challenges.

- National job growth has slowed sharply, and younger renter cohorts are feeling the strain, raising near-term risks for renter demand and lease-up activity.

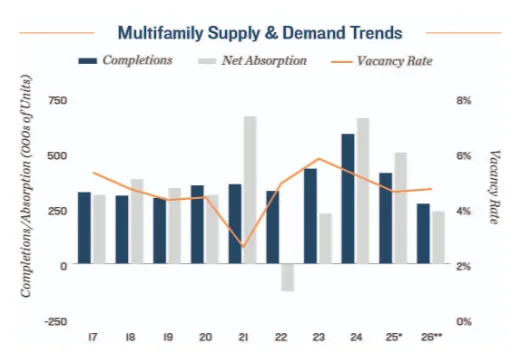

- A sharp drop in multifamily construction—down 53% from 2023’s peak—is setting the stage for tighter supply conditions in future years.

- Elevated homeownership costs and a persistent affordability gap continue to support rental demand, with lease renewal rates remaining above long-term averages.

A Market In Transition

The US multifamily sector is entering 2026 at a crossroads, reports Marcus & Millichap. After several years of unprecedented construction and strong renter demand, the tide is shifting. Vacancy rates are climbing in some regions, and job creation has lost momentum, particularly among key renter demographics.

The national vacancy rate stood at 4.6% at the end of Q3 2025—down from early 2024 highs, but still elevated in key markets. Net absorption, while strong in recent years, has begun to slow, revealing cracks in near-term fundamentals.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Economic Uncertainty Hits Core Renter Demographics

The multifamily sector’s short-term prospects are increasingly tied to macroeconomic volatility. Since new tariffs were introduced in April, hiring activity has declined. The US added nearly 500K jobs between January and April 2025, but only 193K between May and September.

The employment situation is particularly acute for renters aged 20 to 28—traditionally a core driver of multifamily demand. Their jobless rate rose to 7.4% in September, compared to 4.4% nationally.

Sun Belt markets, where much of the recent construction has occurred, are especially exposed. Domestic migration has cooled from pandemic-era highs, and vacancy rates in those metros are now roughly 200 basis points above the national average. In addition, average effective rents have declined across many heavily built-out areas.

Long-Term Tailwinds Offer Reassurance

While 2026 may bring challenges, the longer-term outlook for multifamily remains fundamentally strong. The construction pipeline is rapidly contracting, with the number of units under construction down 53% from its 2023 peak. Rising construction and labor costs are expected to keep new development subdued.

Meanwhile, the cost of owning a home remains a major barrier to exit for renters. As of late 2025, the monthly payment on a median-priced home is approximately $1,200 more than average apartment rent. This affordability gap continues to drive high lease renewal rates, currently near 55%—well above the historical average.

Additionally, some delayed household formation—due to job market uncertainty—is expected to bounce back once economic conditions stabilize, further supporting long-term multifamily demand.

What To Watch In 2026

The key to a stronger multifamily recovery will be renewed job growth and improved consumer confidence. If hiring picks up and household formation rebounds, high housing costs and limited new supply could catalyze a relatively swift improvement in sector performance. But until then, investors and developers should prepare for uneven performance across markets, with an emphasis on resilience in supply-constrained metros.