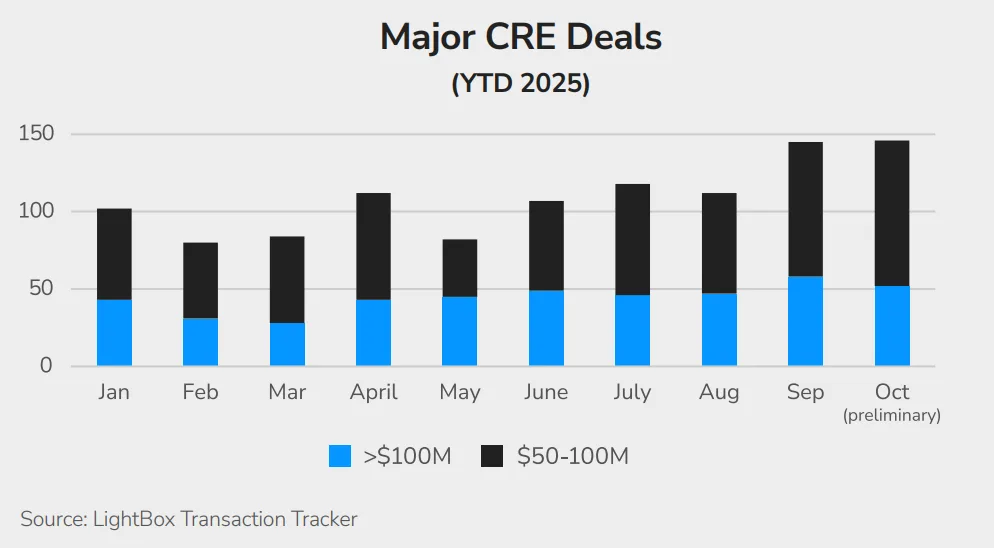

- CRE transaction volume reached $34.6B in October, up 28% from September, as activity expanded across multiple sectors.

- Mid-cap deal volume surged, while institutional capital targeted healthcare, data centers, and prime office assets.

- Top deal: A $7.2B outpatient medical office portfolio sale from Welltower to Remedy Medical Properties and Kayne Anderson.

- Office sector showed early signs of stabilization, posting its first annual vacancy decline in five years.

CRE Market Regains Momentum in Q4

According to LightBox, October marked a turning point for US commercial real estate. Transaction volume hit $34.6B, rising sharply from $27B in September. Importantly, activity was spread across asset classes, with multifamily, retail, and office accounting for 65% of total volume.

“Activity picked up across the board, pointing to a shift from reactive to strategic investment,” said Manus Clancy, Head of Data Strategy at LightBox.

Multifamily, Retail, and Office Lead the Pack

Multifamily remains a top investment target. While rent growth is still modest, the sector appears to have moved past peak vacancy. Moreover, low construction activity—paired with a national housing shortage—continues to support investor interest, especially in growing metro areas.

Retail also performed well. Vacancy remains near historic lows, and though rent growth is moderating, it is still healthy. Notably, supply is constrained due to record-low development. As a result, new tenants—including restaurants, fitness, and medical users—are absorbing space quickly.

Office, on the other hand, remains mixed. The market is likely several quarters away from peak vacancy. However, sales activity surged in October, signaling early signs of stabilization. Q3 saw the first annual vacancy rate decline in five years, dropping 20 basis points to 18.8%. Investors are increasingly focused on well-located, next-generation buildings and suburban assets. Meanwhile, central business districts continue to struggle due to excess space and tighter financing.

Land and Alternatives Attract Growing Attention

Land deals made up 11% of October volume, up from 8% in September. Demand is high for sites tied to housing and data centers. However, challenges like high construction costs, tighter credit, and tariff uncertainty are slowing new projects. Still, developers remain active in regions with strong job growth and population gains.

One standout deal was BlackChamber Group’s $160M purchase of a 38-acre site in Northern Virginia’s data center corridor. The sale marked a 6,800% increase from its 2004 price. Located in Prince William County’s Data Center Opportunity Zone, the land will be redeveloped into a hyperscale campus.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Winners and Losers in October Deal Activity

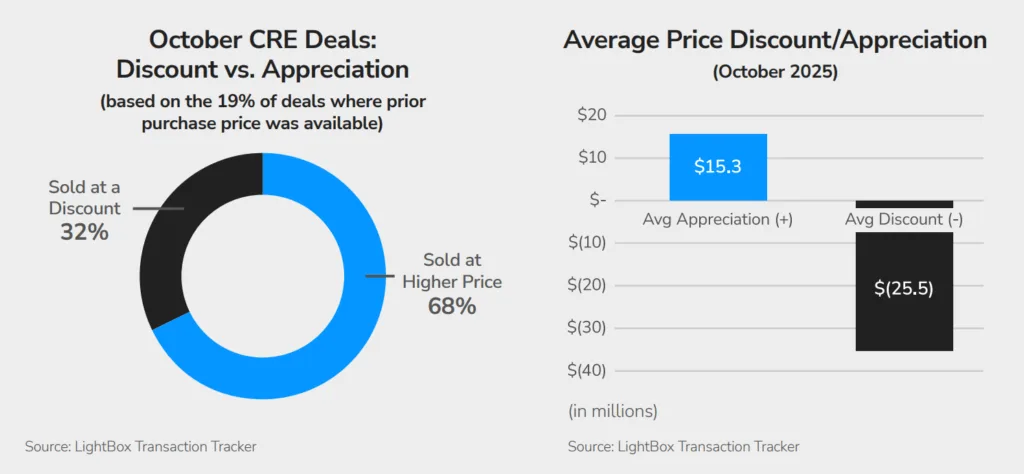

Among nearly 1,100 closings, LightBox found that 68% of tracked deals with price history sold for more than their previous purchase price. Meanwhile, 32% sold at a loss, with office properties accounting for most of the markdowns.

The largest decline came from Irvine Company’s sale of One America Plaza in San Diego for $120M—a 60% discount from its 2005 purchase price of $300M. Still, San Diego’s office market is faring better than Los Angeles, with a 29% Q3 vacancy rate.

Conversely, the largest value increase came from the BlackChamber land deal, underscoring the explosive growth of data center development.

Institutional Buyers Dominate October Transactions

Institutional capital played a major role in October’s largest deals.

- Remedy Medical Properties and Kayne Anderson completed the month’s top transaction—a $7.2B acquisition of 296 outpatient medical properties across 34 states. The portfolio was 94% leased.

- Centersquare, backed by Brookfield Infrastructure, bought 10 data centers across North America for approximately $1B, expanding its footprint to 80 facilities.

- In the office sector, SL Green Realty Corp. acquired Park Avenue Tower in Manhattan for $730M. The 95% leased asset highlights renewed confidence in top-tier office locations.

Outlook: Positive Indicators for Year-End Activity

The LightBox CRE Activity Index remained strong at 106.2 in October, staying above the 100-point “healthy activity” benchmark for the ninth month in a row. This follows September’s elevated reading of 116.8, which accurately forecast the October volume surge.

With interest rates easing, credit spreads tightening, and refinancing conditions improving, investors are returning to the market more strategically. Although macro uncertainties persist—including tariffs, labor, and policy volatility—the overall sentiment is turning cautiously optimistic.

“After two years of recalibration, the CRE market is entering a more orderly phase,” said Clancy. “Capital deployment is increasingly strategy-driven. Investors are preparing portfolios for a more constructive 2026.”