Top Picks for Favorite Apartment Markets in 2024

Plus: RXR and Ares Management join forces on new NYC office fund.

Jordan B.

January 23, 2024

Together with

Good morning. RealPage economists share their predictions for top apartment markets to outperform in 2024. Plus, one of New York’s biggest property developers is launching a $1bn fund to invest in the city’s distressed office buildings.

Today’s issue is brought to you by AirGarage. Receive a comprehensive revenue forecast for your parking facility to boost NOI.

Market Snapshot

|

|

||||

|

|

*Data as of 1/22/2024 market close.

INCOMING SUPPLY

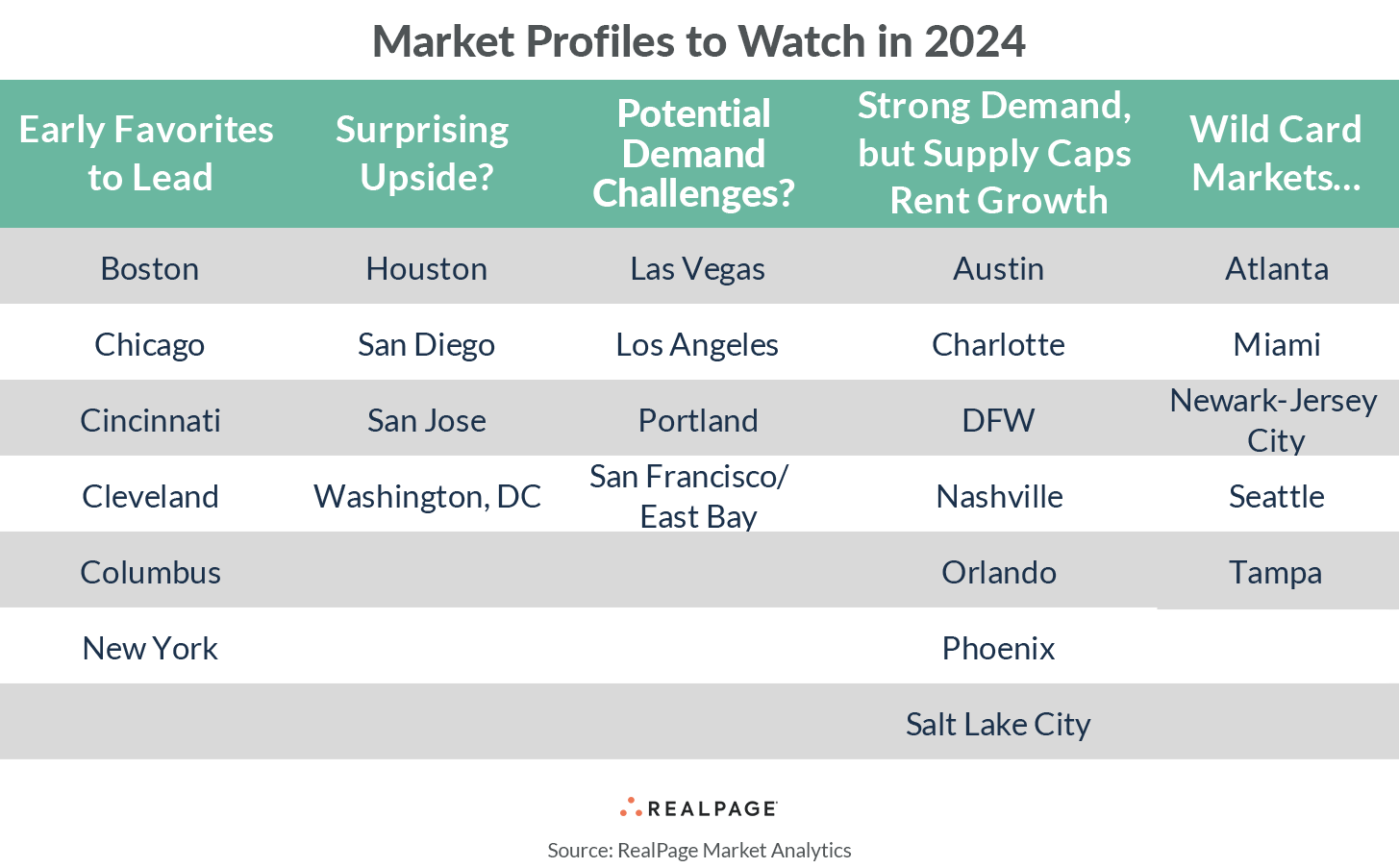

RealPage Economists’ Picks for Favorite Apartment Markets in 2024

2024 is shaping to be a pivotal year for the U.S. apartment market, with a record supply of approximately 670,000 new units, dwarfing 2023’s already impressive 440,000 units. Amidst this surge, which markets are top picks?

Leading the pack: Economists from RealPage have spotlighted stable Midwest markets like Chicago, Cincinnati, Cleveland, and Columbus, along with Northeast metros Boston and New York, as top performers for 2024. These markets boast high occupancy rates above 94% and have experienced rent growth surpassing national averages in 2023. Their construction activities have been moderate, indicating a balanced supply for the coming year.

In the hunt: Houston’s balanced supply-to-demand ratio could surpass other Texas markets in the near future. And despite a considerable supply planned for DC, the capitol is expected to outperform in 2024 due to concentrated growth in key submarkets. In fact, a third of DC’s submarkets will see no new supply in 2024.

Strong demand: Markets like Austin, Charlotte, Dallas/Fort Worth, Nashville, Orlando, Phoenix, and Salt Lake City are expected to see solid demand but might experience limited rent growth due to intense supply. These areas are set to witness inventory growth well above the national average, with some, like Austin and Phoenix, expecting increases of over 8%.

Wild cards: Atlanta, Miami, Newark, Seattle, and Tampa are the wild cards for 2024. Notably, Newark is absorbing new supply due to rising demand for more affordable apartments, especially from those relocating from Manhattan, making it a market to watch closely.

Challenges ahead: Meanwhile, major West Coast metros like LA, Las Vegas, Portland, San Francisco, and Oakland could face potential demand challenges this year. These metros all experienced rent cuts in 2023, and their occupancy rates ranged from 94–95%. While the new supply has been reasonable, it’s expected to limit rent growth potential, says RealPage.

➥ THE TAKEAWAY

A tale of many regions: The U.S. apartment market is bracing for a surge in apartment supply in 2024, which will significantly impact performance. While stable Midwest and Northeast markets are projected to lead in terms of occupancy and rent growth, challenges may arise in the West and other supply-heavy markets.

SPONSORED BY AIRGARAGE

AirGarage is offering parking facility revenue audits and due diligence for CREDaily readers.

Even in 2023, many parking lot and parking garage owners won’t know how much revenue their parking facility generates each month.

That’s because the parking industry is still stuck in its old ways, using cash, paper tickets, and spreadsheets.

Do you want real-time analytics and data-driven analysis of how much revenue your parking facility generates and how much it could be making with more optimization?

To help you understand the true value of your parking assets, AirGarage will:

-

Analyze your parking facility’s historical performance

-

Install our License Plate Reading cameras at your property to track usage

-

Give you a deep dive report on your past revenue and future opportunities to increase that revenue

AirGarage is the nation’s fastest-growing parking management company, combining our proprietary technology and operations to maximize revenue at hundreds of parking lots and parking garages across 37 states.

Interested in a parking revenue audit with AirGarage? Get in touch.

✍️ Editor’s Picks

-

IPO alert: Eyeing a $700M IPO, American Healthcare REIT (GRAH) is set to bring almost 300 properties from Indiana, Ohio, and beyond to the public market.

-

The big reveal: Don Tepman has revealed himself as StripMallGuy on Twitter, amassing 215K followers for his daily industry advice and deal alerts.

-

Real estate rollercoaster: A shift in interest rate expectations and rising 10-year Treasury yields led to a slump in real estate stocks in Wednesday’s market.

-

International intrigue: Major cities’ hotels, including NYC and LA, roll out new offerings to entice international visitors, with travel rebounding to 83% of pre-2019 levels.

-

Reverting to the norm: The bond market braces for a return to tradition, with traders predicting the 10-year Treasury yield to outpace the 2-year yield.

-

Rx for real estate: The surge in diabetes medications like Ozempic for weight loss poses potential shifts in commercial real estate, impacting retail and asset dynamics.

-

Closed: Realty Income Corp. (O) finalized a $9.3 billion all-stock deal to acquire Spirit Realty Capital (SRC), adding a massive 61.6 million square feet to its portfolio.

-

Comeback: Sam Nazarian gears up for a grand comeback, partnering with Wyndham Hotels & Resorts to launch ‘Project HQ Hotels & Residences’, targeting 50 new sites by 2030.

🏘️ MULTIFAMILY

-

The old college try: College towns remain resilient, with higher apartment occupancy rates and overall stability, but offer less upside during boom periods.

-

Multifamily moves: CBRE’s latest report highlights a significant uptick in key multifamily investment metrics. Unlevered IRR targets, initial (going-in) cap rates, and anticipated (exit) cap rates all saw an increase in Q4, signaling a robust shift in the sector.

-

Surfside condos: In a bold move, a Miami developer invested $64 million to acquire a prime oceanfront site in Surfside. The plan? To construct a lavish 10-story luxury condominium tower featuring an exclusive collection of 25 units.

-

Hand them over: WS Communities, one of Los Angeles’s largest landlords, is set to hand over properties valued at a staggering $1.1 billion to its lenders, marking a significant event in the city’s real estate landscape.

-

Affordable Harvard town: Cambridge, MA has relaxed zoning laws to allow for 15-story multifamily buildings, requiring every unit to be income-restricted affordable housing.

🏪 RETAIL

-

Expanding empire: Jeff Sutton has done it again. The retail titan and SL Green sold 715-717 Fifth Avenue retail space, spanning 115,000 SF, to Kering for $963M. Kering is a French luxury group owning brands like Gucci, Balenciaga, and Alexander McQueen.

-

Rejected: Macy’s pulls a Yahoo!-like move by rejecting a $5.8B takeover offer from Arkhouse Management and Brigade Capital, citing a lack of compelling value.

🏢 OFFICE

-

Bailing on China: BlackRock (BX) plans to sell some Shanghai office towers at a 30% discount due to low rents and a sluggish property market.

-

Leasing silver lining: Colliers reports positive pre-leasing data for 2H23, with 46.2% pre-leased and Manhattan at 83.3%, with 36.4MF of active construction expected to be completed in 2024.

FILLING THE GAPS

RXR and Ares Launch $1bn Fund to Invest in Distressed NYC Offices

US office leasing activity peaked in Q4 after a long pause, with several large deals announced. Source: Reuters

RXR (RXRA), one of New York’s largest office landlords, is joining forces with alternative investment manager Ares Management to launch a $1B fund aimed at investing in distressed office buildings in the city.

Why the conviction? The partners believe prolonged uncertainty around interest rates and remote work has thawed the city’s CRE market, presenting discounted opportunities. The fund will target office buildings that require fresh capital to remain competitive or restructured debts due to higher rates and slower rent growth.

Diamonds in the rough: RXR and Ares plan to focus on the upper quartile of class-A NYC offices, which offer potential value due to being shunned by lenders and investors. These properties, ranking below the newest and most modern towers but above older offices becoming obsolete, present a unique opportunity for opportunistic investors.

Rising expectations: $117B in commercial mortgages tied to U.S. offices will mature this year, contributing to tons of distressed sales. The tightening in CRE debt availability and the inclination of banks to shed exposure has left office owners with few options for refinancing loans or securing new capital for property improvements.

Capitalizing on conditions: Ares continues to fill gaps left by retreating lenders. Last year, it acquired PacWest Bancorp’s $3.5bn loan portfolio during its liquidity crisis. Now, they are joining forces alongside RXR, seeding the new fund with $500mn and aiming to raise another $500mn. “We bring capital and operational expertise and an understanding of what’s happening in the leasing market to know where tenants are going,” said Rechler.

➥ THE TAKEAWAY

Why it matters: This move by RXR and Ares could be a game-changer for New York’s CRE market, signaling a shift in investment strategies post-pandemic. As remote work reduces demand for office space and rising rates add to challenges faced by property owners, distressed dealmaking is expected to go up. The launch of RXR and Ares Management’s $1B fund highlights the potential for value creation in the upper quartile of the middle class-A office market, mostly overlooked by lenders and investors.

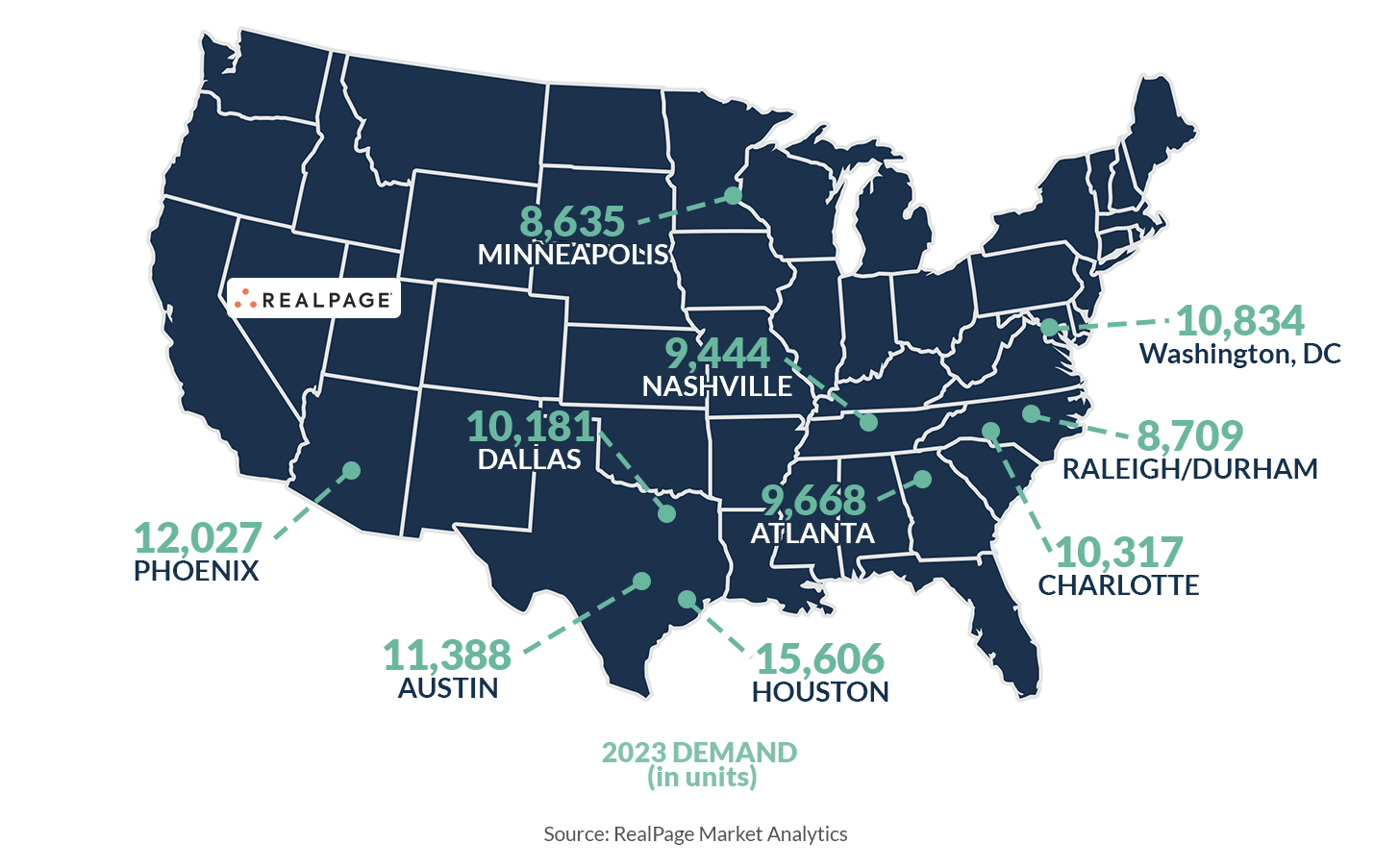

CHART OF THE DAY

In 2023, top U.S. apartment markets saw Houston leading (15,606 units absorbed annually), followed by Austin (11,388) and Charlotte (10,317). DFW came in 4th (10,181). Interestingly, no major coastal gateway cities made the top 10, except for DC. Florida cities were absent from the top 10 entirely.

What did you think of today’s newsletter? |