Syndication Distress: What’s Happening and How GPs and LPs Can Respond

Aleksey Chernobelskiy breaks down what’s happening in real estate syndication and how GPs and LPs should respond.

Jordan B.

May 05, 2024

Together with

Good morning. Welcome to the weekend edition of CRE Daily.

-

📰 Feature: What’s happening in the world of syndication distress

-

⏪ Catch up: The most-read stories from the week

-

👍️ Reviews: 4 new product reviews on CREDaily.com

-

📈 Chart: Major tech firms are downsizing their office spaces

Today’s issue is brought to you by Redwood Living.

Distress in Syndication

Syndication Distress: What’s Happening, and What Can Both GPs and LPs Do About It

This week, we teamed up with Aleksey Chernobelskiy, who advises Limited Partners (“LPs”) and has a unique perspective on syndicated real estate transactions.

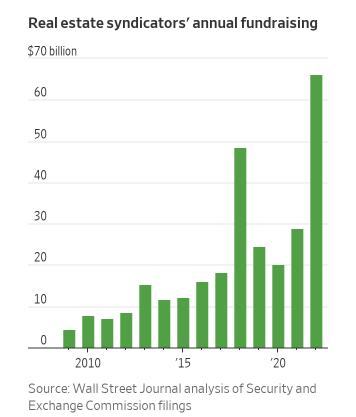

State of the market: Many real estate syndicators (“GPs”) are in a unique world of pain today due to rising rates, expanding cap rates, expiring rate cap contracts, and debt maturities. Unlike their institutional counterparts, these groups do not typically have a balance sheet to pull on and have much higher leverage than other real estate investors. As reported in the WSJ, these syndicators have attracted hundreds of billions of capital from retail investors, many investors putting in as little as $5-10k.

Between the lines: When a partnership runs out of money at a given property, the only option is to raise capital from the existing LP pool of partners (“capital call”) or seek external financing. At the time of such capital calls, many properties have a valuation that is approaching their principal balance on the senior loan (meaning the equity is wiped out). Seeking external capital isn’t cheap either and usually comes at ~15% cost.

What can GPs do about a property that’s in distress?

Plan in advance:

-

The amount of time you have to make a decision is critical and often deprioritized. I’ve seen this personally at a syndicator GP, and now I see the result of such procrastination from the perspective of an LP.

-

Real estate is an asset that is fairly illiquid and therefore anything you would like to do 3-6 months from now needs to be put in motion today and strategized 9-12 months prior to the execution date.

-

The great thing about real estate is that it is fairly simple (from a capital stack perspective) and the decisions are few – so doing things last minute typically comes off as unprepared at best.

Understand your options:

-

This is really important because many people think that the only option is issuing a capital call.

-

On the flip side, some are scared to issue a capital call but instead, go get external capital at a much higher cost to LPs without notifying the LP

Communicate well and early:

-

If you’re going to make a capital call (or alert the investors on any important decision), make sure you (1) outline their options, (2) are clear on why this decision is best for them, (3) explain clearly and analytically why you believe that to be the case

-

If the plan is a capital call, don’t forget to mention how (if at all) are you personally participating in the plan financially.

-

Take responsibility where it’s relevant to do so, and if you decide not to take responsibility (we can’t control everything, I get it) please don’t do the following.

What can LPs do about a property that’s in distress?

If you have a hunch that something is wrong but haven’t gotten an official notice:

-

Firstly, you should recognize the fact that you might be wrong in your assumptions. Perhaps the property is actually not in distress and you made some mistakes in your calculations. Having said that, it’s important to note that I have seen cases of GPs realizing that they are in a bind after an LP asks them a few pointed questions.

-

Even though your position as an LP is silent and you’re not in control of the investment, you should not feel helpless and unable to impact what happens.

-

Proceed with grace. If you lead with anger or tension, the counterparty is much less likely to listen to you.

If you got a capital call notice to respond to:

-

First, remember that this is an investment decision, just like the one you made at the outset! Remember that when you originally made your investment, you had data, models, and a thesis. Today, things should not be any different—you should have everything you need to decide whether investing more capital into this property is a good or bad financial (not emotional!) decision. Ask questions!

-

A corollary to the above is that the decision should NOT be based on fear of losing your original investment (I know it sucks, but it’s already made!) or the property going into foreclosure because you don’t contribute to the capital call (there are generally other sources of capital the GP can tap).

-

Finally, it’s important to remember that the alignment of interests may conflict in distressed situations.

-

Note that all of the above has to come after determining that your property is in distress, and I would not recommend waiting for your GP to tell you this.

➥ THE TAKEAWAY

Big picture: The syndication universe is facing unique challenges today and hundreds of millions of equity capital is at stake. For GPs, it’s critical to explore all of your options early and communicate clearly with your LPs. On the other hand, LPs should take the time to understand whether their investment positions are impaired and reach out to the GP if they’re expecting challenges that haven’t been addressed.

If you enjoyed this and want to get more updates on the GP/LP marketplace, please sign up for Aleksey’s weekly updates at www.lplessons.co.

TOGETHER WITH REDWOOD LIVING

Why Invest Directly in BTR Real Estate

While current market conditions might be causing some to pause their real estate investments, beginning the right long-term relationship with an operating platform with a longstanding track record in BTR can still be advantageous. See how you can benefit from investing directly in a build-to-rent investment opportunity with Redwood.

Please support our sponsors. It helps keep CRE Daily free.

⏪ Weekend Wrap-Up

Catch up on the most clickworthy stories of the week.

-

Cooling down: Austin’s apartment rents have taken a nosedive, leading the nation with a -7.4% year-over-year drop in April.

-

Mounting distress: The U.S. office market is experiencing turmoil as over $38B of office buildings are at risk of loan defaults, foreclosures, or distress, the highest level since 2012.

-

FOMC: Fed Chairman Jerome Powell held the line against inflation and kept interest rates steady at 5.25–5.5%, hinting at delayed cuts in 2H24—but only if inflation cools down.

-

Alternatives soar: Q1 of 2024 saw a 41% increase in sales volume for alternative real estate sectors, including medical offices and data centers, as reported by MSCI’s capital trends.

-

Cannabis reconsidered: The DOJ’s recommendation to reclassify cannabis as a lower-risk substance could significantly impact the real estate sector for marijuana businesses.

-

Debt dial: Distressed CRE levels in the U.S. surpassed $88.6B in 1Q24, up $2.7B from 4Q23, per a recent MSCI report.

-

Risk, reward: Brookfield (BN) repays riskier tranches in full on $675M in San Francisco apartment loans, resulting in a 45% loss on its initial investment.

-

Checkout closed: Walmart (WMT) is closing all 51 Walmart Health centers due to cost issues, suddenly impacting healthcare access for countless communities across the country.

-

Property pain: NYCB’s defaulted loans hit $800M in Q1, increasing the pressure on CRE lenders and regulators.

-

Buy it back: As delinquencies mount in multifamily mortgages, lenders are racing to buy back loans from their commercial real estate collateralized loan obligations to mitigate rising rates.

-

Return of the King: WeWork is all set to exit bankruptcy by as early as the end of May after court approval of key motions.

-

Deal: Related Cos. sells W Fort Lauderdale to Blackstone for $98M. The 346-key oceanfront hotel went for $282K per room.

-

Work trends: A survey by Federal News Network reveals that 30% of federal employees work entirely remotely, 6% work fully on-site, and 64% combine telework with office duties.

👍 Product Reviews

Compare reviews and prices on the top CRE software, products, and services.

RE Analytics

Reonomy |

RealtyMogul

CRED iQ |

Want us to review your product? Get in touch.

📈 CHART OF THE DAY

Major tech firms like Amazon and Meta are downsizing their office spaces and letting leases lapse. Data from CompStak shows Amazon, Google, and Microsoft leading in office footprint reduction nationwide from Q2 2023 to Q1 2024. The largest expired leases were in the Bay Area for Amazon and Google and Seattle for Microsoft. Over the next two years, tech lease expirations nationwide will surpass other industries by 60.5% in average size.

What did you think of today’s newsletter? |