Lending Market Shows Signs of Stabilization

The CRE lending market showed promising signs of stabilization in the final quarter of 2023,

Jordan B. & Han-Gwon Lung

February 21, 2024

Together with

Good morning. The CRE lending market showed promising signs of stabilization in the final quarter of 2023. However, while banks are leading the lending uptick, bad CRE loans are starting to exceed reserves.

Today’s issue is brought to you by RE Analytics — grow your analyst team without having to cover costly overhead.

Market Snapshot

|

|

||||

|

|

*Data as of 2/20/2024 market close.

LOAN CLOSINGS

Lending Market Shows Signs of Stabilization

The commercial real estate lending market showed promising signs of stabilization in the final quarter of 2023, as exhibited by the latest CBRE research.

Slight uptick: The CBRE Lending Momentum Index, a key measure of U.S. commercial loan closings, experienced a 1.0% increase in Q4 2023 compared to Q3 2023. This growth is notable as it marks the first quarterly increase since early 2022, despite a 38.1% year-over-year decline. The index value stood at 189 by the close of Q4.

-

Banks remained the largest contributors to CBRE's non-agency loan closings for the seventh consecutive quarter, making up 39.5% of the total in Q3 2023, a slight increase from the previous quarter. About a third of the Q4 loan volume comprised floating-rate loans, with a focus on refinancings and property acquisitions.

-

Alternative lenders, like debt funds and mortgage REITs, saw increased loan volume participation, rising to 30% in Q4 from 27.4% in Q3 2023. Multifamily assets continued to be the preferred property type for these lenders.

-

Life insurance companies contributed to 27.4% of origination volume in Q4, predominantly in fixed-rate loans for industrial and retail assets, marking a decrease from the previous quarter.

-

CMBS conduits represented less than 3% of the non-agency loan volume, though there was an improvement in Q4 2023. The year’s total CMBS volume declined by 44% compared to 2022.

Underwriting criteria: The average underwritten cap rate increased by 16 basis points to 5.68%, and the loan-to-value ratio rose to 61.4%. Higher interest rates led to loan constants averaging 6.72% in Q4, up from the previous year.

➥ THE TAKEAWAY

What they are saying: James Millon, U.S. President of Debt & Structured Finance at CBRE, highlighted that despite ongoing market challenges, more favorable lending conditions are emerging, especially in specific asset classes. Contributing factors include declining credit spreads, a narrowed trading range for benchmarks, and higher cap rates reset.

SPONSORED BY RE Analytics

Outsource Your Analyst Team & Back Office

The best real estate investment firms need a comprehensive analysis of their properties.

However, hiring a team of analysts can be expensive, covering costly annual overheads like salaries, bonuses, and benefits.

That's where RE Analytics comes in.

Our proprietary platform and team of seasoned real estate professionals can help your company make more informed investment decisions and attract capital to grow your portfolio.

And here's the best part: we work month-to-month, with no long-term contract.

Get in touch today for a free consultation, and let us help take over your back-office responsibilities.

Please support our sponsors. It helps keep CRE Daily free.

✍️ Editor’s Picks

-

Empty office crisis: Remote work during COVID-19 led to a rise in empty commercial buildings, with banks facing $160B in losses.

-

7-Day Multifamily: Learn the systems used to go from 0 to 600+ units in just six years, plus the KPIs to track to successfully operate multifamily properties to increase NOI, cash flow, and asset value. (sponsored)

-

Stalled construction: Commercial construction faces a slow start in 2024 due to labor shortages, rising costs, and ongoing supply chain challenges.

🏘️ MULTIFAMILY

-

Market gap convergence: CBRE predicts 2% growth for U.S. apartment rentals in 2024, narrowing the gap between top and bottom markets.

-

Generational housing boom: LA incentivizes larger apartments for multi-generational families, exempting extra bedrooms and bathrooms from square footage calculations.

-

From contamination to construction: Grand Jersey Group plans to build a 515-unit project in Jersey City, including a 26-story building with 172KSF of office space.

🏭 Industrial

-

Industrial evolution ahead: A report by Newmark and NAIOP predicts a 6–13% increase in manufacturing space nationwide, focusing on advanced manufacturing over warehousing.

-

Construction conundrum: With 49MSF of planned industrial construction, Dallas-Fort Worth still leads the nation despite Phoenix's 42.5MSF.

-

Fundraising frenzy: Elion Partners raised $400M for its U.S. industrial real estate fund, targeting $750M with a $1B hard cap. Multiple commitments have already been reported.

🏬 RETAIL

-

Population boom: Retail is poised to lead the nation in terms of CRE occupancy with +4.8M household growth by 2028, according to Marcus & Millichap

-

Changing of the guard: Plant-based patty retailer Beyond Inc. (BYND) shakes things up with recent leadership changes, and many other retail companies are following suit.

🏢 OFFICE

-

Tech vacancies: In 3Q23, tech markets saw a 30 bps rise in vacancies across traditional, emerging, and national areas.

-

Frozen tower: Vornado (VNO) halted its 18MSF Penn Station office tower project due to frozen capital markets last January.

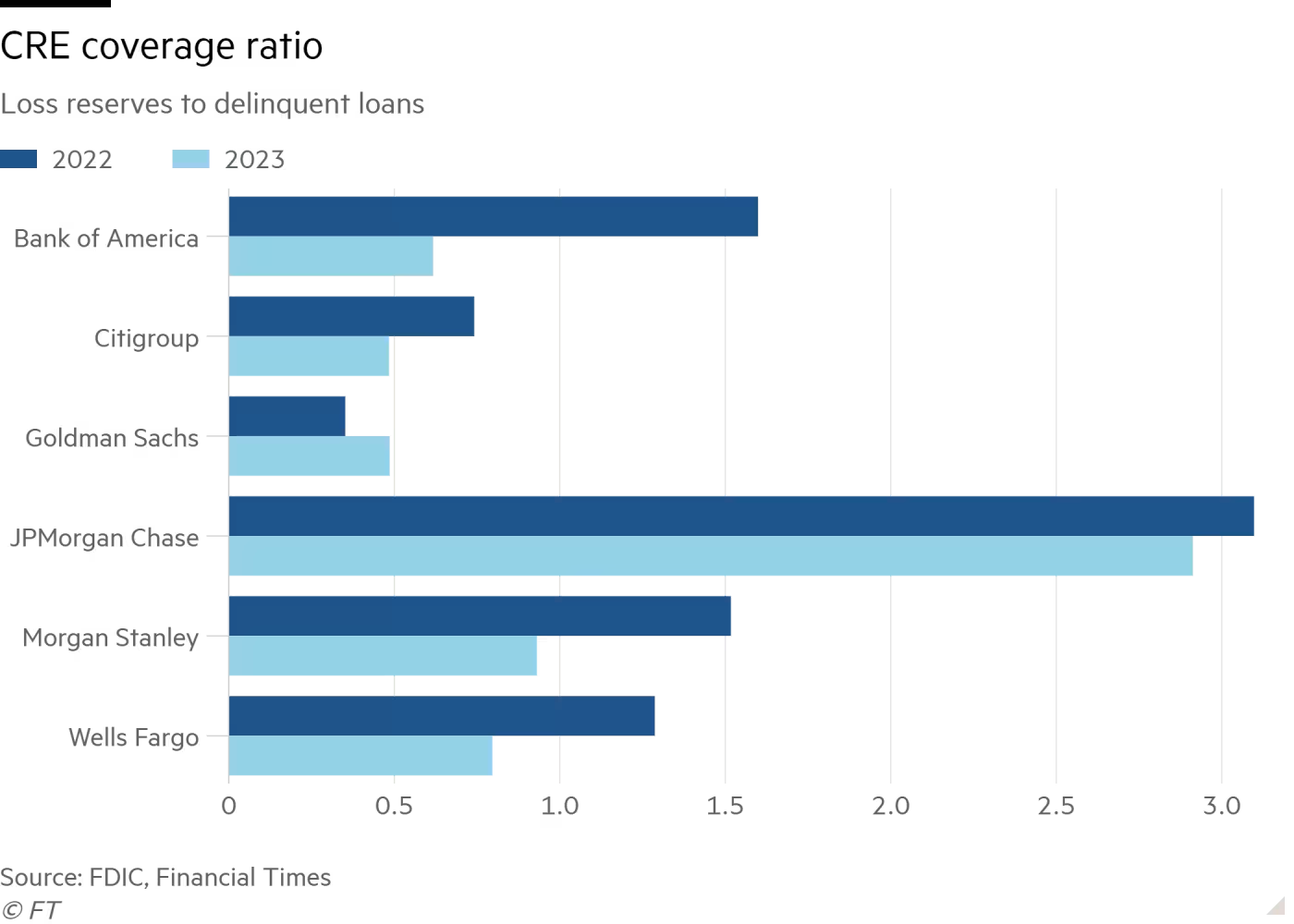

LOAN LETDOWN

Bad Property Debt Now Exceeds Reserves at Largest US Banks

Shares of regional lender NYCB plunged after it reported potential losses in its commercial property loan book © Bing Guan/Bloomberg

The largest U.S. banks are facing the music as bad CRE loans officially surpassed reserve levels, raising alarms about the impact of delinquent debt on the banking sector.

Reserve erosion: Average reserves at top U.S. banks plummeted from $1.60 to just 90 cents for every dollar of CRE debt where borrowers are at least 30 days late. This sharp decline comes as delinquent CRE debt tripled to $9.3B over the past year. The overall value of delinquent loans across the U.S. banking sector tied to CRE has more than doubled to $24.3B, intensifying concerns.

Rising defaults: Delinquencies on loans related to offices, malls, and apartments surged, with banks now holding $1.40 in reserves for every dollar of delinquent CRE loans, down from $2.20 a year ago. This is the lowest cover banks have had in absorbing potential CRE loan losses in over seven years.

Revising strategies: Banks traditionally set reserves based on historical loss rates for different categories, with CRE typically having lower default rates. But after COVID, relying solely on historical data might not make sense this time around. Some experts suggest banks should adopt a more forward-looking approach, basing reserves on current delinquency levels to better prepare for potential future losses.

➥ THE TAKEAWAY

Troubling data: Despite assurances from bank executives about preparedness, recent data reflects a worrying rise in delinquencies on loans tied to CRE. With estimates suggesting potential losses could reach $60B over the next five years, banks may need to reevaluate their reserve strategies to ensure sufficient buffers against unforeseen challenges.

📈 CHART OF THE DAY

In 2023, apartment sales saw a 61% decline in overall volume. Despite the challenging financial landscape, six luxury apartment complexes changed hands for over $200M each last year.

SHARE CRE DAILY & EARN REWARDS

Click the button below to get your personalized referral link. When your colleagues sign up and stay subscribed for 3 days, you'll get credit for a referral.

What did you think of today's newsletter? |