- Retail market dynamics in Q4 2025 featured positive net absorption of 11.9M SF, reversing earlier declines.

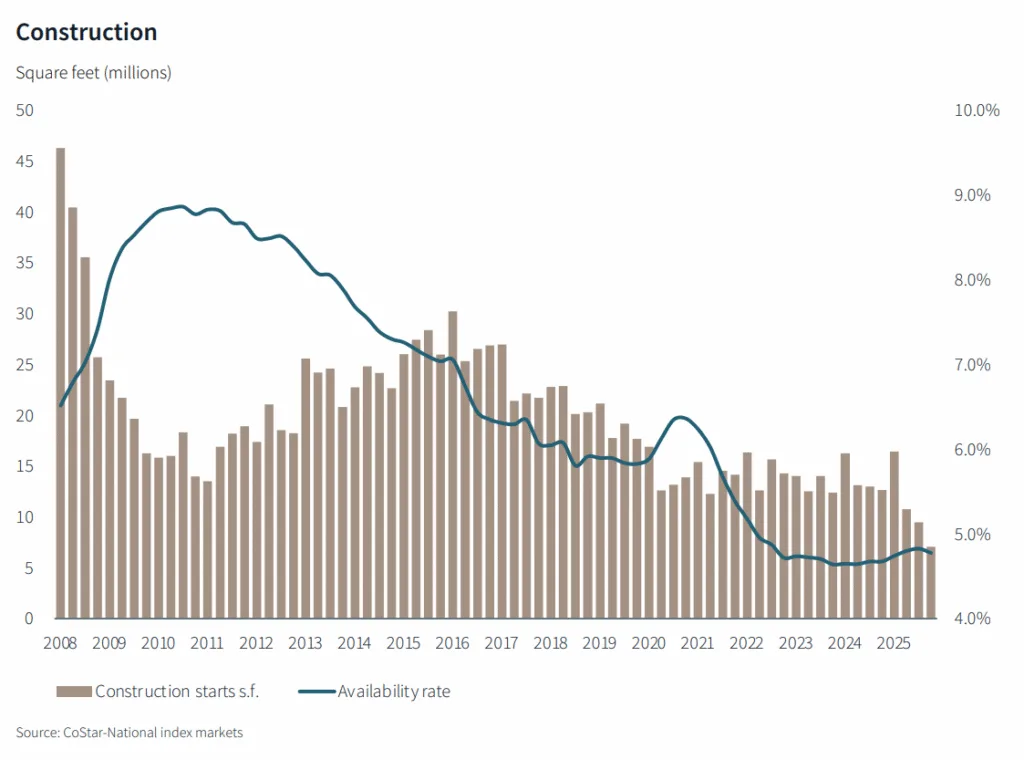

- Retail construction starts fell 44% YoY, with supply and quality space remaining tight.

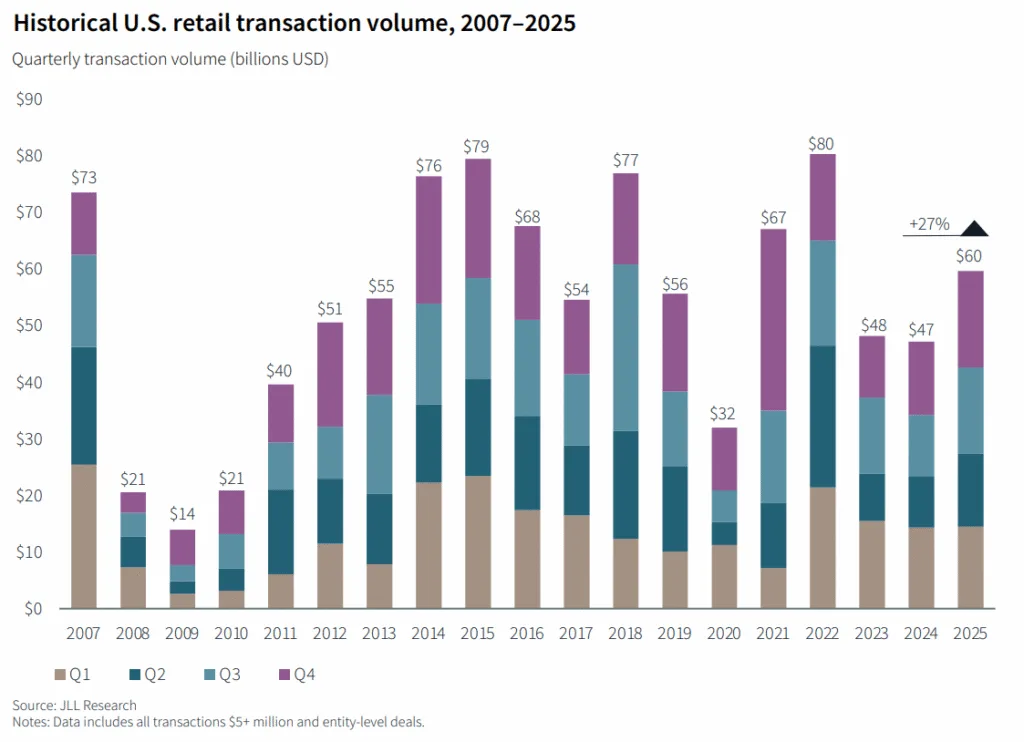

- Institutional investment in retail assets hit $60B, up 27% from 2024.

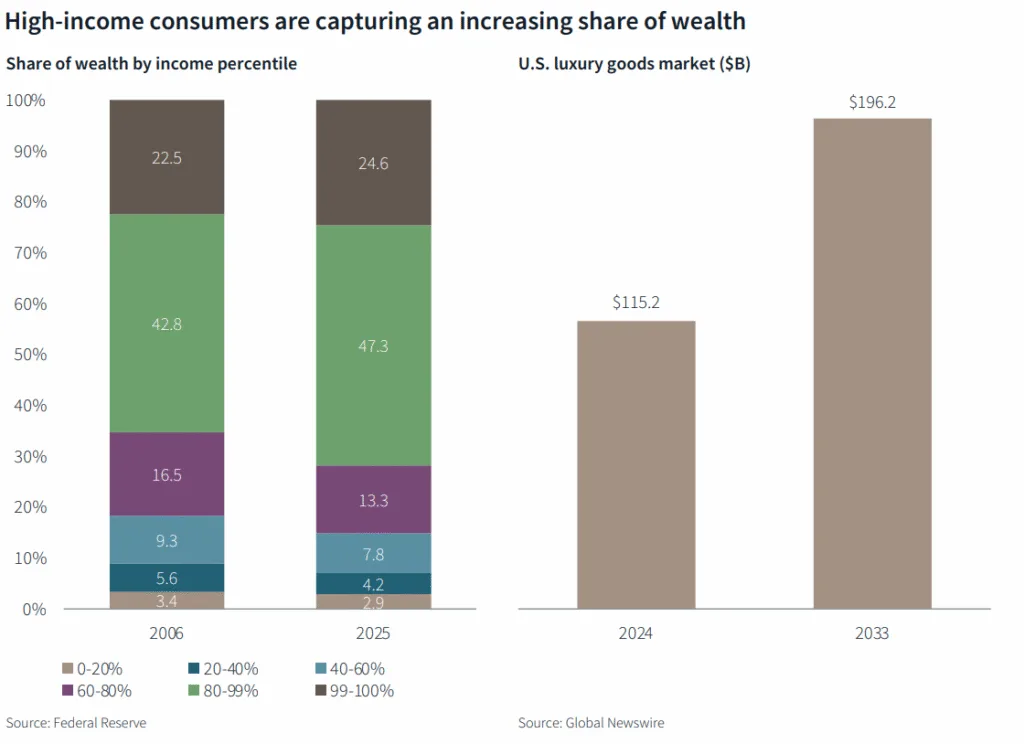

- Luxury and discount segments outperformed mid-market retailers amid shifting consumer wealth patterns.

Retail Market Sees Demand Recovery

JLL reports that the US retail sector rebounded in Q4 2025, with net absorption reaching 11.9M SF and countering weakness seen in the year’s first half. General retail and neighborhood strip centers posted the strongest gains, while mall assets continued to lag, reporting negative annual absorption and elevated vacancies.

Overall, Q4 retail market dynamics reflected continued stabilization after a year of closures and consolidations. Power centers and strip centers experienced only modest improvements, but positive late-year leasing signaled market normalization.

Supply Remains Constrained

Development headwinds continued, with only 7.1M SF breaking ground in Q4—a 44% decrease YoY. Net new deliveries totaled 9.1M SF, while demolitions remained modest at 1.4M SF. The active pipeline shrank to 52.1M SF under construction nationally.

Persistent supply shortages resulted in fewer options for expanding retailers, lengthening average lease-up times to 7.6 months. Tight supply supported rent growth in most major markets, particularly Charlotte and Nashville, while some large coastal metros saw flat or falling rents.

Leasing Activity and Tenant Trends

Despite flagging overall leasing volume, retailers quickly absorbed high-quality space as it became available. Nearly 70% of leases were for spaces of 2,500 SF or less, and almost 90% were below 5,000 SF. The leading tenants in Q4 included fitness operators and discount/value retailers such as Crunch Fitness and TJX brands.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Institutional Investors Target Retail

Retail market dynamics attracted institutional capital, with investment volumes rising to $60B in 2025—outpacing the sector’s historic average. Institutional buyers accounted for nearly 20% of all retail acquisitions, their highest share in a decade. Large deals ($100M+) made up 18% of 2025’s volume, signaling renewed interest from long-term capital sources.

Public market signals have mirrored this renewed confidence. Retail-focused REITs posted stronger Q4 leasing momentum and improved price performance, reinforcing broader optimism around the sector’s recovery.

However, limited supply remains a constraint, holding transaction counts below recent highs despite robust investment demand. Investors are seeking portfolio diversification and yield premiums relative to other CRE asset classes.

Consumer Segmentation Drives Strategy

Retail market dynamics continued to reflect diverging consumer spending patterns. Wealth concentration among high-income households supported growth in the luxury sector, while value-oriented and essentials retailers catered to budget-conscious shoppers pressured by inflation.

Looking ahead, experts anticipate ‘barbell’ demand with premium and discount formats outperforming as middle-market retail faces heightened challenges. Retail formats centered on experiences and essential services are also projected to see stronger performance.

What’s Next

With occupancy steady near 4% vacancy and rents still climbing in core markets, 2026 is expected to bring further selective leasing and more backfilling of existing centers rather than major new development. Investors and tenants will continue to compete for a constrained pool of quality assets as retail market dynamics remain shaped by supply-demand imbalances and evolving consumer preferences.