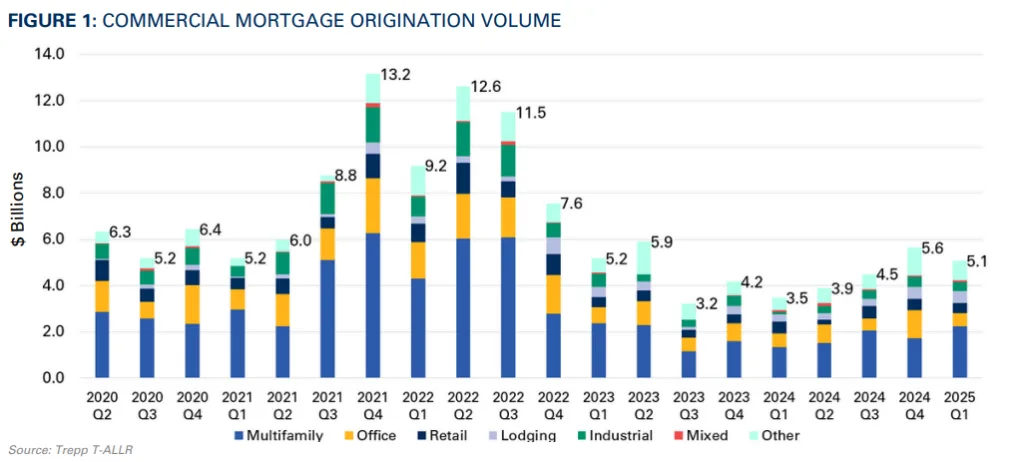

- CRE loan originations fell slightly to $5.1B in Q1 2025, ending 2024’s growth trend but still topping Q1 2024’s $3.5B.rn

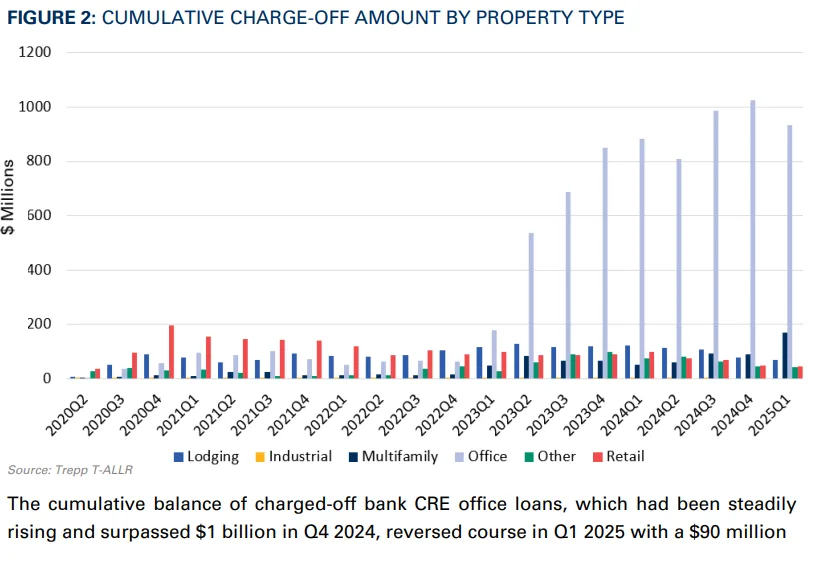

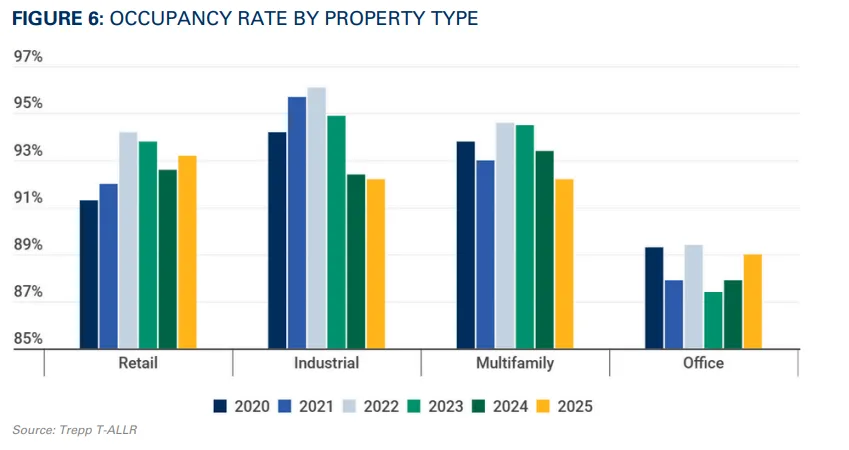

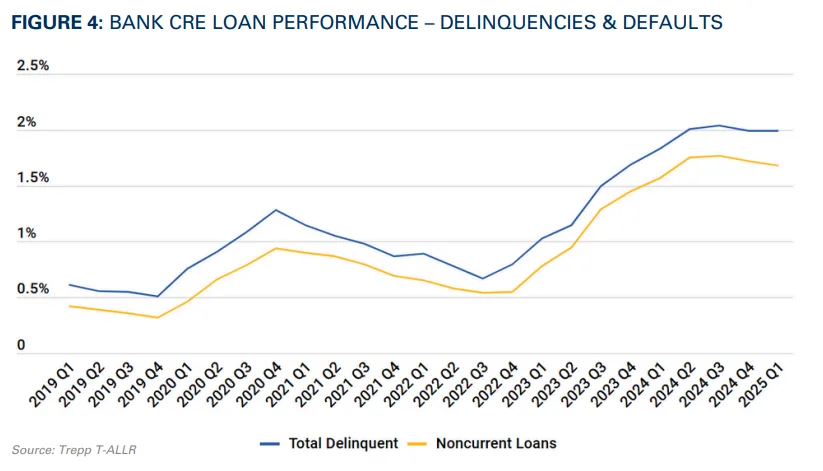

- Office performance improved, with declines in charge-offs and delinquencies and stronger occupancy.rn

- Multifamily distress increased, with higher charge-offs and delinquencies, plus a drop in occupancy.rn

- Criticized loan rates remain high, especially in office-heavy markets like San Francisco and Washington, though some cities saw relief.

CRE Lending Slows but Stays Strong Compared to 2023

As reported by Trepp, commercial real estate lending slipped slightly in Q1. Total originations came in at $5.1B, down from $5.6B in Q4 2024. Despite this dip, lending activity was still well above levels seen in early 2024 and late 2023—helped in part by early signs of office recovery, which may be restoring some lender confidence in the sector.

Multifamily was the top sector by dollar volume. It posted a 67% increase in originations year-over-year. Lower interest rates and delayed deals from 2023 helped support the surge.

Office Sector Begins to Show Positive Signs

The office market may be finding its footing. Charge-offs dropped by $90M, the first decline in two years. The total charge-off balance now stands at $933M.

Delinquencies also improved. The rate fell to 6.54%, down 20 basis points from Q4. Office occupancy rose to 89%, close to pre-pandemic averages. These gains suggest that the sector may have reached a low point and could be starting an office recovery.

Multifamily Shows Growing Signs of Stress

In contrast, multifamily is weakening. Delinquencies rose from 1.44% to 1.58%. Charge-offs nearly doubled, reaching $171M, up from $89M at year-end 2024.

Occupancy also declined. It’s down 2.2% since Q3 2024, driven by too much new supply and softening demand. This trend is especially strong in certain sunbelt markets.

Office Criticized Loans Still High in Key Markets

Criticized office loan rates remain elevated in large cities like San Francisco, New York, and Washington, D.C. These markets face ongoing pressure from high vacancies and tough refinancing conditions.

However, some metros showed progress. Atlanta and Chicago saw lower criticized loan rates in Q1. But Dallas and Washington worsened due to maturing debt and tighter lending terms.

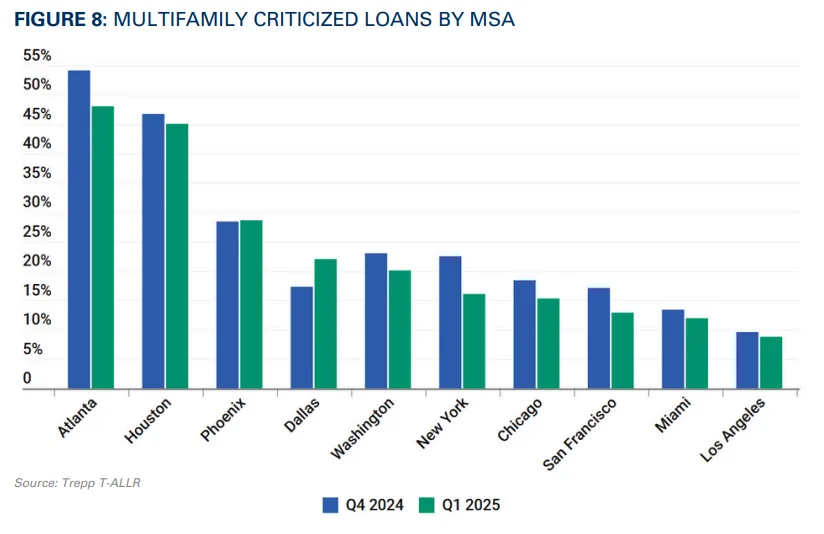

Multifamily Criticized Loan Rates Improve in Some Cities

The multifamily sector remains under stress, but most major markets saw modest improvements. In Atlanta, the criticized loan rate fell more than 6%, landing at 48%. Houston also saw a small drop, while other cities posted declines of 1%–7%.

Dallas was an outlier, with a 4.7% increase, although that follows a large improvement in the previous quarter.

CRE Market Outlook: A Sector in Transition

The start of 2025 showed a mixed picture. Office loans saw encouraging signs of recovery. Meanwhile, multifamily may face more trouble in overbuilt areas.

Retail and industrial remain relatively stable. But industrial delinquencies rose by 53 basis points, reflecting softer demand and more new supply.

Looking ahead, banks may tighten lending standards, especially for office and multifamily deals in riskier markets. Changes in interest rates and regional growth will keep shaping how banks approach CRE.

Why It Matters

CRE loan performance is closely tied to interest rates, demand, and local market trends. The office sector is stabilizing, while multifamily may split, with strong and weak markets pulling in different directions. Lenders will need to stay cautious and flexible as 2025 unfolds.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes