- Industrial market leasing activity grew 17.8% year-over-year in Q1 2026.

- Mega-box warehouses led absorption, with 17M SF absorbed in Q1.

- Big-box leasing jumped 80.7%, with strong demand from 3PLs and e-commerce.

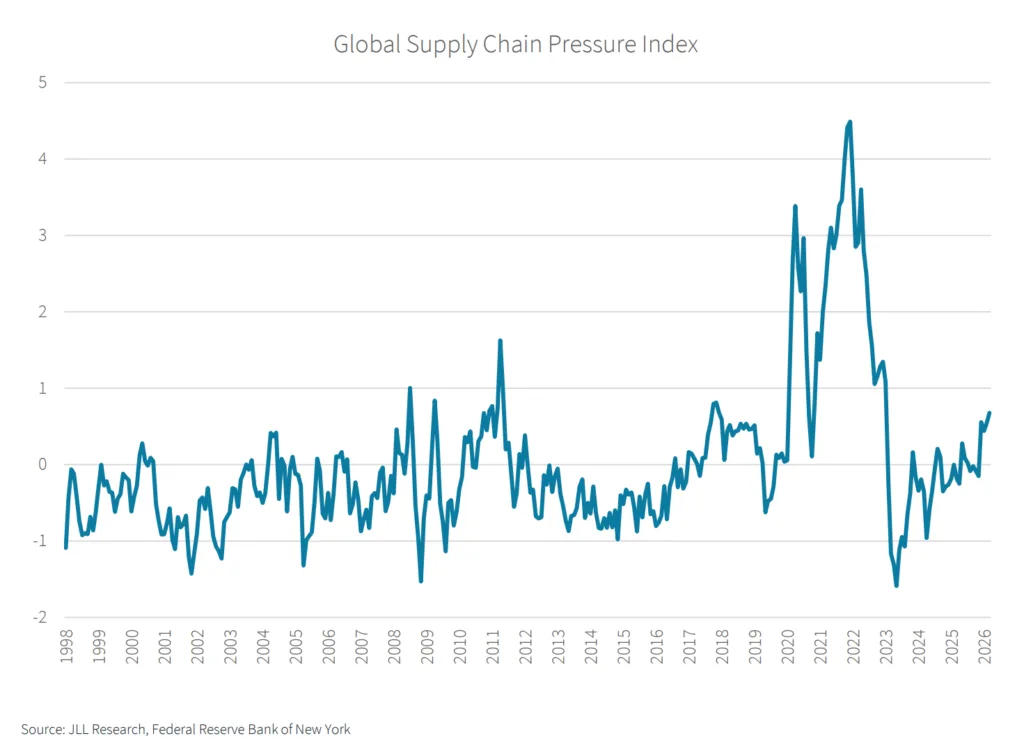

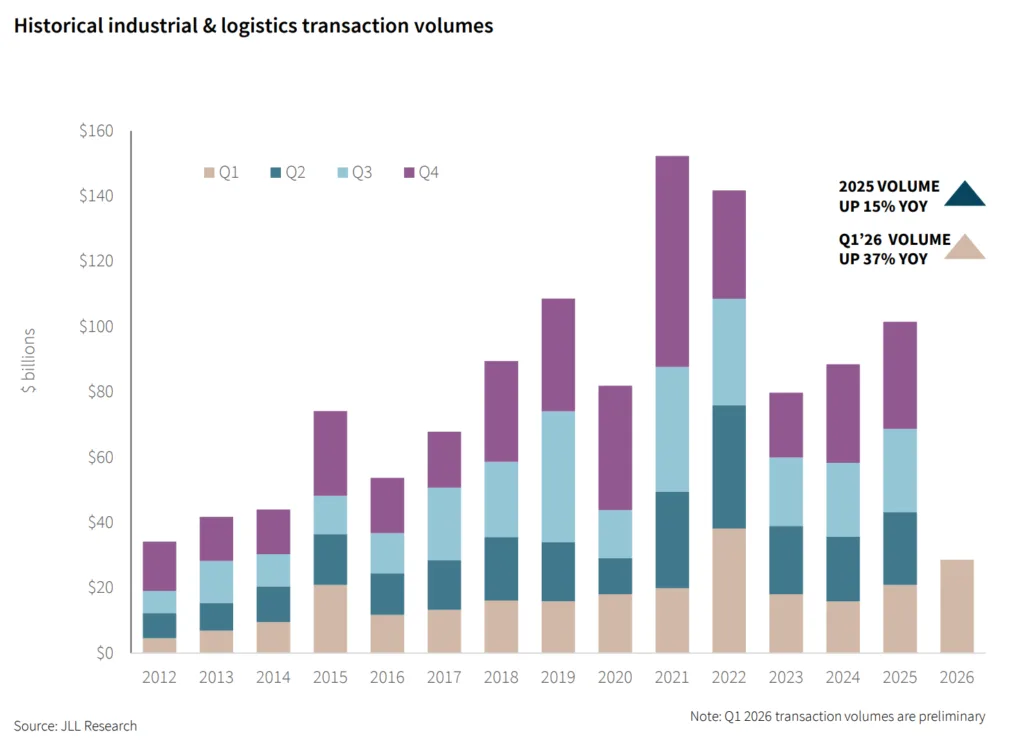

- Capital markets activity rose 36.6% YOY, signaling renewed investor confidence.

Leasing and Demand Strengthen

JLL’s US industrial market report showed continued resilience in Q1 2026 as leasing activity hit 145.2M SF—up 17.8% from the prior year. Robust demand was fueled by continued tenant migration into high-spec facilities, with 71.6% of leases being new commitments. Large occupiers, such as third-party logistics providers (3PLs), accounted for a significant portion of new leasing, reflecting growing need for flexible supply chain solutions and regional distribution hubs.

Mega-Box Absorption Drives the Market

Net absorption totaled 50.9M SF, the strongest first quarter since 2023, led by mega-box warehouses greater than 1M SF. These facilities accounted for 17M SF of absorption, mostly concentrated in logistics hubs like Chicago, Phoenix, Dallas-Fort Worth, Houston, and New Jersey. The flight to quality and operational consolidation continue to bolster industrial market dynamics.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Supply Expands, Vacancy Stabilizes

Development in the industrial market climbed 2.2% year-over-year, with 259.5M SF under construction and 55.7M SF delivered—the lowest quarterly delivery since Q2 2017. Vacancy held steady at 7.5%, though tightening is expected as supply slows and demand remains strong, particularly for modern Class A space. Pre-leasing rates on speculative projects rose to 16.5%.

Rents and Investment Trends

Asking rates in the industrial market increased 0.8% year-over-year to a nationwide average of $10.34 PSF, with Class A mega-box rents surging 14.5%. Landlords in some markets are offering more concessions amid high availability. Investment volumes reached $28.6B in Q1 (up 36.6% YOY), with capital depth remaining solid and strong investor demand for core assets. Debt market activity also increased, with originations up 21% year-to-date.

What’s Next

Strategic shifts in supply chains, including nearshoring and expanded regional distribution, will continue to support Industrial Market growth. At the same time, uncertainty around global trade policy and tariffs is starting to influence how tenants think about lease duration and network flexibility, even as underlying demand remains intact. While geopolitical and trade policy uncertainty may drive some tenants to seek shorter lease terms, the broader outlook for leasing and investor interest remains optimistic driven by e-commerce expansion and the push for supply chain resilience.