- Office recovery is underway as leasing activity rises, space availability declines, and hybrid work patterns stabilize.rn

- Debt and equity capital are returning, with CMBS issuance and institutional buying both rebounding sharply in early 2025.

- Office pricing appears to have bottomed, offering attractive cap rates and yield spreads compared to other property types.

- Strategic opportunities exist across both core assets and distressed properties amid a generational reset in valuations.

The Long-Awaited Inflection

Two years ago, institutional investors had little appetite for office properties. With vacancy still historically high, skepticism lingers—but momentum is quietly building, reports Cushman and Wakefield. Leasing activity is up double digits, available space is falling, and capital—both equity and debt—is flowing back into the sector.

Behind this optimism: cap rate spreads, relative value versus other asset classes, and a realization that the worst of the work-from-home disruption may now be behind us.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Leasing Trends Point To Recovery

While remote work persists, its expansion has stalled. According to the BLS, fully remote employment rose just 0.6% year-over-year in April 2025, lagging overall job growth. Occupiers are increasingly committing to hybrid work models with clearer long-term space needs.

- Office attendance has leveled between 60–75% of pre-pandemic norms.

- Leasing activity surged over 10% year-over-year in 2H 2024 and continues to rise.

- Average lease size is up 13% since Q3 2023.

- Occupied office space declined by just 0.6% over the past year, a notable improvement from the 2.3% drop in the depths of the pandemic.

These trends suggest tenants are no longer in full retreat.

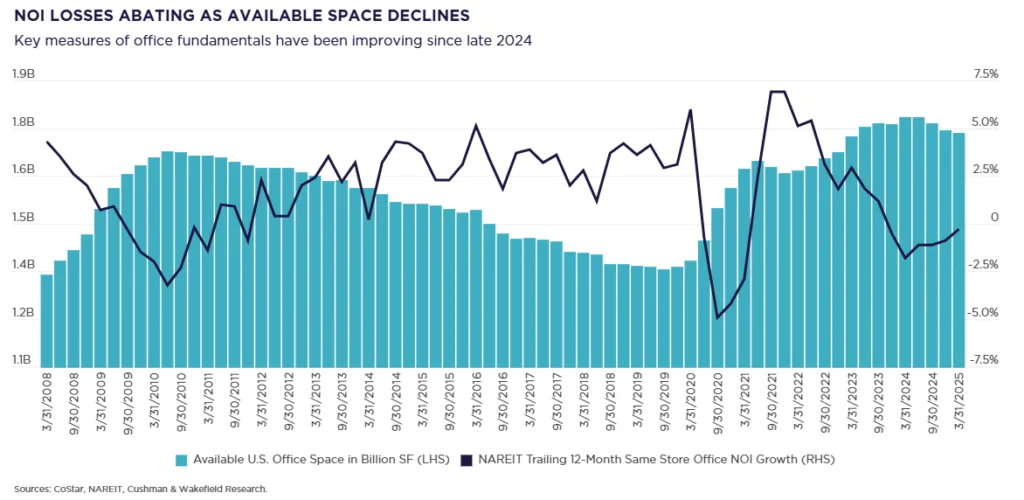

Supply Tightening And NOI Stabilizing

Availability of US office space has now declined for three consecutive quarters, driven largely by a drop in sublease listings. Coupled with the fact that new construction is near historic lows, this tightening dynamic is beginning to support fundamentals.

- Same-store NOI for office REITs dipped just 0.3% year-over-year in Q1 2025, its best result in over a year.

- As the market finds firmer footing, some investors are increasingly viewing this as a bottoming opportunity.

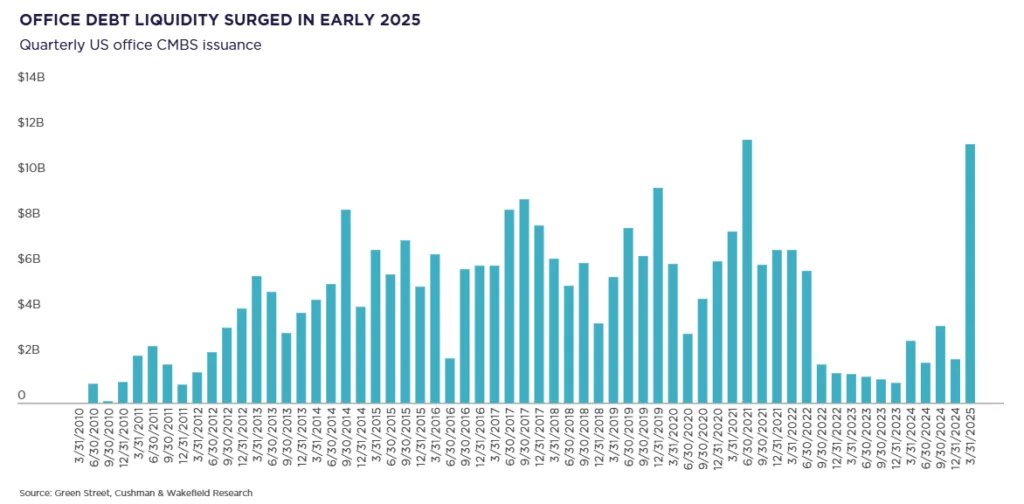

Debt Liquidity Is Back

The clearest sign of confidence? Lenders are re-entering the fray.

- cmbs issuance for office surged to $11.4B in Q1 2025—the strongest first quarter since 2007.

- Private lenders and debt funds are becoming more active, expanding beyond banks.

- Capital is now available for deals ranging from core to opportunistic, enabling a broader range of investment strategies.

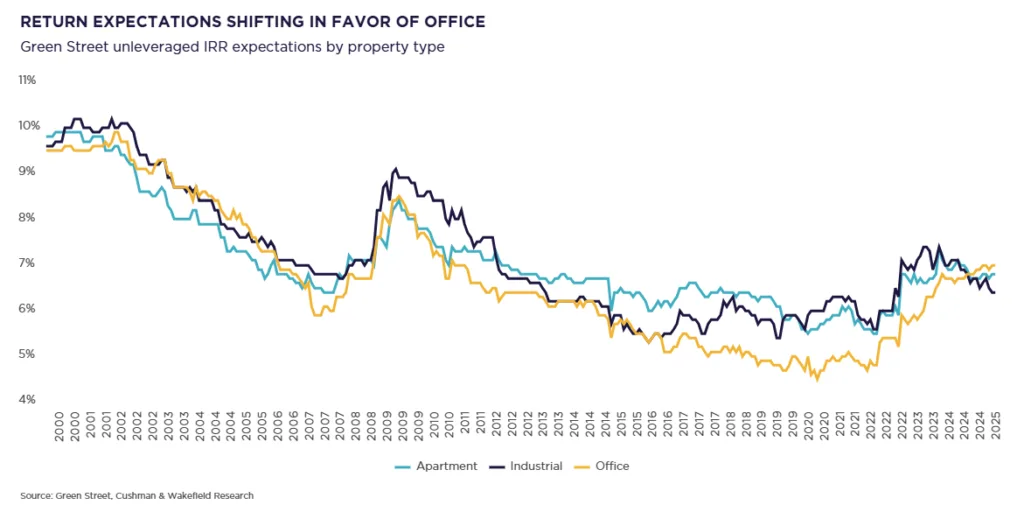

A New Cycle For Office Pricing

Office sales volume has rebounded from its 2023 lows. Institutional and REIT buyers increased office acquisitions by over 200% in 2024. Pricing indices from Real Capital Analytics and Green Street have shown either gains or stabilized declines since late 2024.

Meanwhile, cap rates in the office sector (7.4–8.8%) now far exceed those in industrial or multifamily. This yield spread is re-attracting core and yield-driven investors, particularly as Fed policy stabilizes and inflation moderates.

Strategic Recommendations

- Lean in to the reset: Pricing is attractive, and fundamentals are stabilizing. For well-located, modern office properties, current dislocation may be short-lived.

- Don’t write off core: Usage at Class A+ properties is rebounding faster—Kastle Systems shows 93% of pre-pandemic peak midweek activity. These buildings are outperforming and leasing up.

- Watch for a trophy space squeeze: With new construction stalled and demolitions rising, future shortages of high-end space are likely. This bodes well for today’s A-minus properties.

- Be patient with distress: The wave of troubled deals has only just begun. The next few years will bring continued recapitalizations, conversions, and workouts—especially for outdated, underutilized properties.

Why It Matters

While uncertainty remains, especially around economic growth and interest rates, early signs point to a slow but meaningful revaluation of the US office sector. With pricing still 20–30% below peak and yields at multi-year highs, the market offers compelling opportunities for diversified, yield-seeking investors.

If historical norms reassert, and office regains its pre-pandemic share of overall transaction volume, today’s buyers may be getting in ahead of the curve.