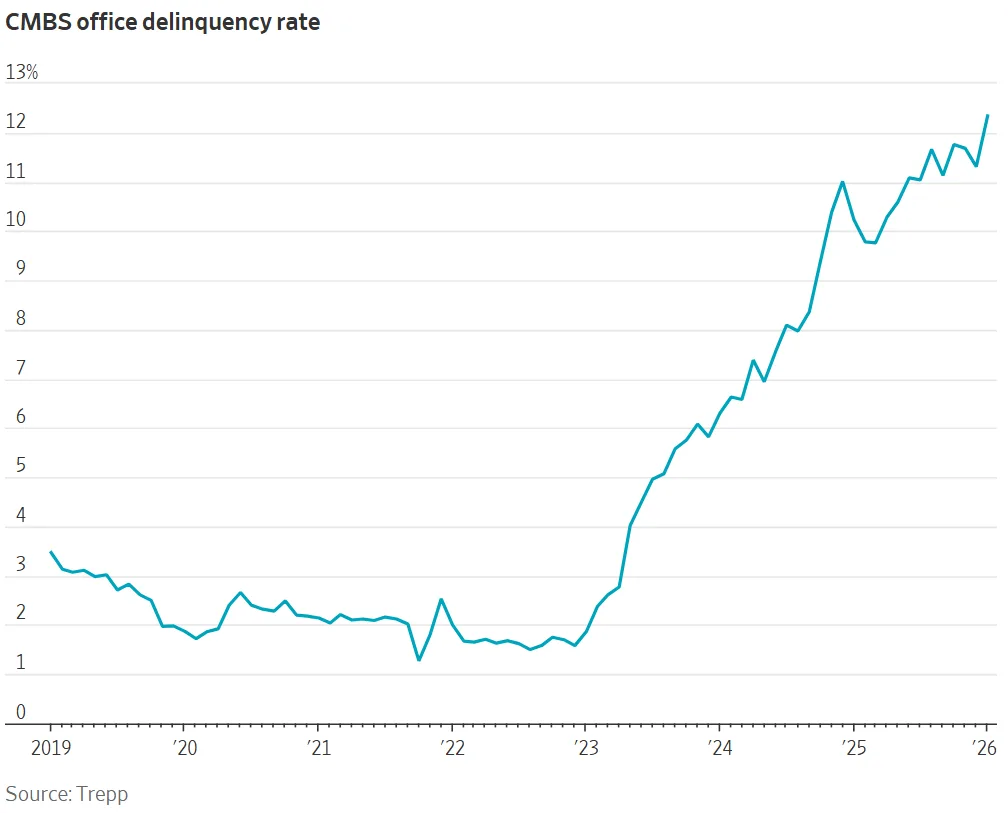

- Office loans delinquency rate rose to 12.34% in January, a new record for the sector.

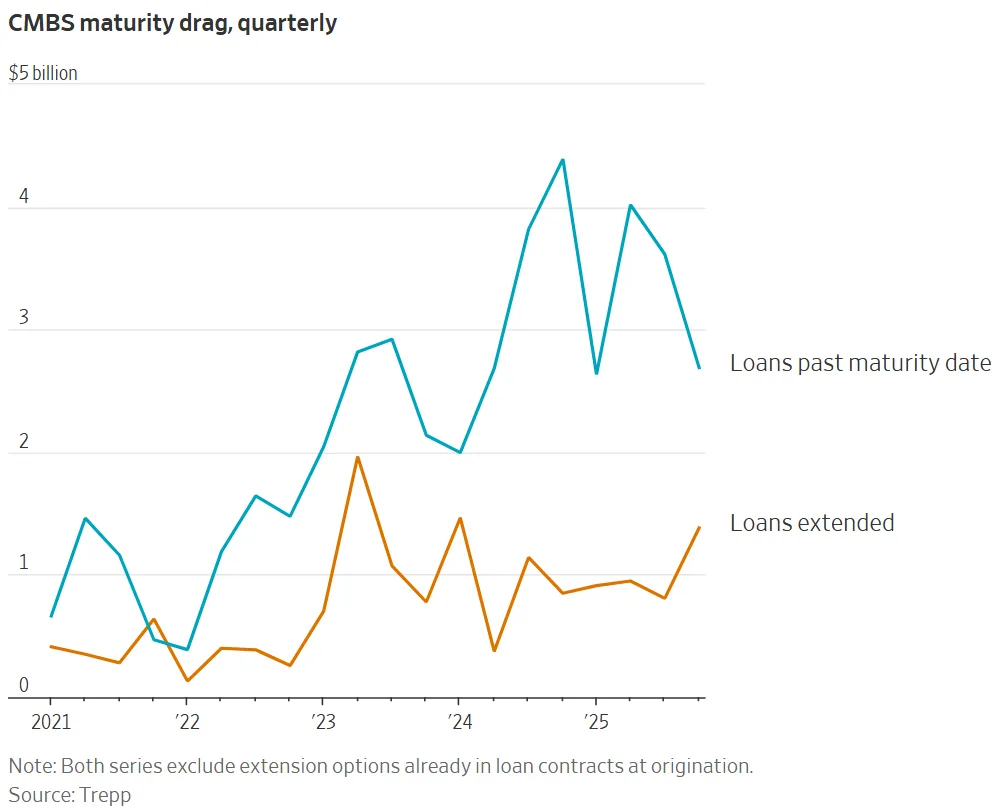

- More than half of $100B in CMBS office loans maturing this year unlikely to pay off at maturity.

- Structural shifts, not just economic cycles, are weakening office demand long-term.

- Distress expanding to regional banks with high commercial real estate exposure.

Record Office Loans Delinquency

The WSJ reports growing stress in the office sector. The delinquency rate for office loans in CMBS reached 12.34% last month. That figure marks the highest level recorded since 2000.

Previously, lenders extended maturing office loans and bet on lower rates or stronger cash flow. Now, refinancing options have narrowed. As a result, lenders are calling in more debts instead of granting extensions.

Debt Maturities Strain Owners

Refinancing for many office owners has become nearly impossible due to higher interest rates. More than 50% of the $100B in CMBS office loans coming due this year are projected to miss maturity payments, according to Morningstar DBRS. In previous years, over 75% of such loans were paid off at maturity. The volume of distressed commercial real estate debt now rivals post-2008 crisis levels.

Structural Shifts Pressure Office Market

Lenders increasingly view reduced office demand as a permanent structural change rather than a cyclical downturn, with hybrid work and remote options lowering long-term occupancy needs. Stalled loans and building vacancies contribute to the phenomenon of ‘zombie’ office buildings, which impact downtown economies in cities like Portland, San Diego, and Dallas. The growing gap in performance between struggling office assets and stronger property types such as industrial and data centers is becoming more pronounced. This divergence underscores how capital is gravitating toward sectors with durable demand and away from traditional office exposure.

Regional Bank Stress and Capital Markets

Stress from rising office loan delinquencies is spreading to regional lenders. Many of these banks expanded aggressively into commercial real estate in recent years. Now, that exposure is drawing greater scrutiny. Several large office projects are approaching foreclosure. As a result, investors and analysts are watching banks like Bank OZK closely. They want to understand how much risk sits on these balance sheets.

Meanwhile, the broader CMBS market shows renewed activity. Issuance reached $125.6B in 2025, up 21% from the prior year. This increase signals continued liquidity in healthier property types. Industrial assets and grocery-anchored retail centers continue to attract capital.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes