- The US multifamily market has absorbed record levels of new supply, with over 500K units expected to be delivered in 2025, but a sharp decline in starts points to a likely rebound in rent growth by 2027.

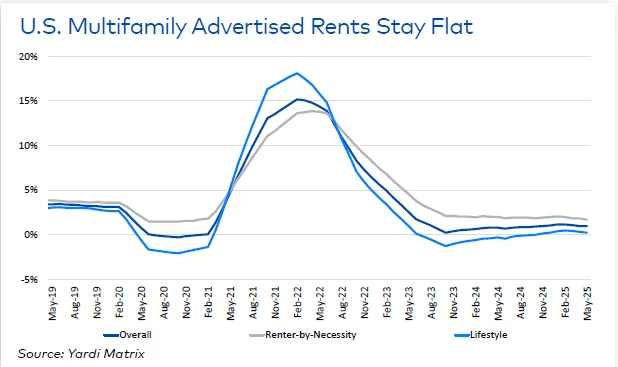

- National rent growth remains modest at 1.5%, with the strongest gains in constrained markets like New York, Kansas City, and New Jersey, while oversupplied Sun Belt metros continue to post rent declines.

- Investor appetite remains, with $25.9B in multifamily transactions through May 2025, and liquidity is strong, though a disconnect between buyer and seller expectations continues to constrain deal volume.

Deliveries Slow As The Supply Wave Peaks

After a record-breaking 2024, the US multifamily market is facing the next stage in its cycle, reports yardi matrix. The report forecasts 536K completions in 2025—a decline from 663K the year prior. This wave, while historic, is now ebbing as new construction starts fall, driven by high financing costs, labor shortages, and inflation in land and material prices.

Charlotte (8.4%), Phoenix (7.5%), and Austin (7.4%) lead in 2025 supply growth as a share of existing inventory. New York, the largest gateway market, will add over 17,500 units, or 2.8% of its inventory.

Rent Trends

National average rent is expected to rise 1.5% in 2025, reaching $1,761. Sun Belt metros continue to struggle with negative rent growth due to oversupply. Austin (-3.5%), Denver (-1.9%), and Phoenix (-1.7%) are among the weakest performers. In contrast, constrained supply markets like New York (3.5%), Kansas City (3.0%), and New Jersey (3.0%) are leading on the upside.

Still, absorption has been robust: in 2024, 555K units were absorbed, and 2025 is off to a healthy start. Cities like Indianapolis and Austin continue to lead in demand, suggesting that once the supply glut wanes, rents could bounce back.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Capital Markets

Multifamily remains the most attractive commercial asset class, but transaction volumes are still subdued. Through May, sales reached $25.9B—up slightly year-over-year—but still below pre-2022 levels due to a persistent pricing gap. Buyers want discounts to account for higher interest rates; sellers remain reluctant.

However, debt capital is plentiful. cmbs issuance is on track for its strongest year since 2007, and agency lending is surging. Delinquency rates are rising—CMBS reached 6.4%—but ample rescue capital is preventing widespread distress.

Recovery On The Horizon

The national rent growth forecast is 1.1% in 2026 before rebounding to 2.7% in 2027. By 2028, rent growth is projected to stabilize in the 3.0–3.5% range. High-supply markets like Austin, Miami, and Raleigh-Durham are expected to return to positive rent growth territory by the end of 2027, as new development slows and excess inventory is absorbed.

While policy uncertainty, tariffs, and affordability challenges remain risks, the multifamily sector is positioned for a gradual but firm recovery, with constrained markets already paving the way.