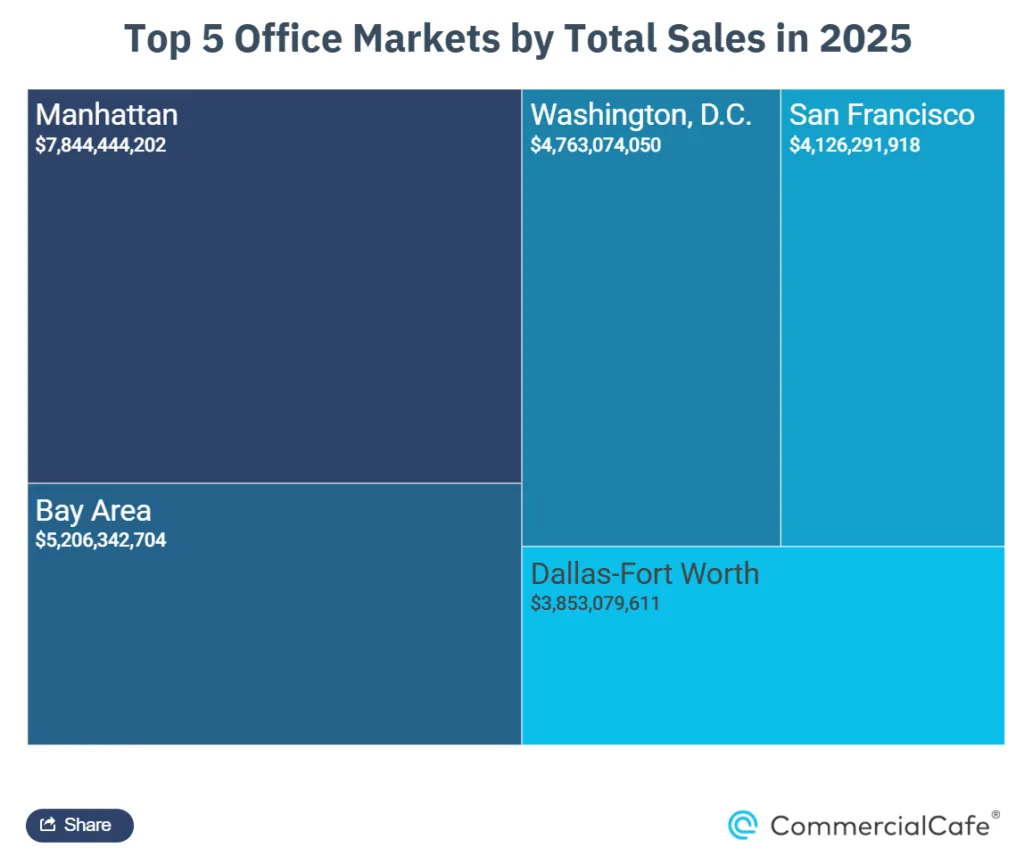

- Manhattan ranked as the top US office investment market in 2025 with roughly $7.8B in sales and the nation’s highest average pricing at $496 PSF.

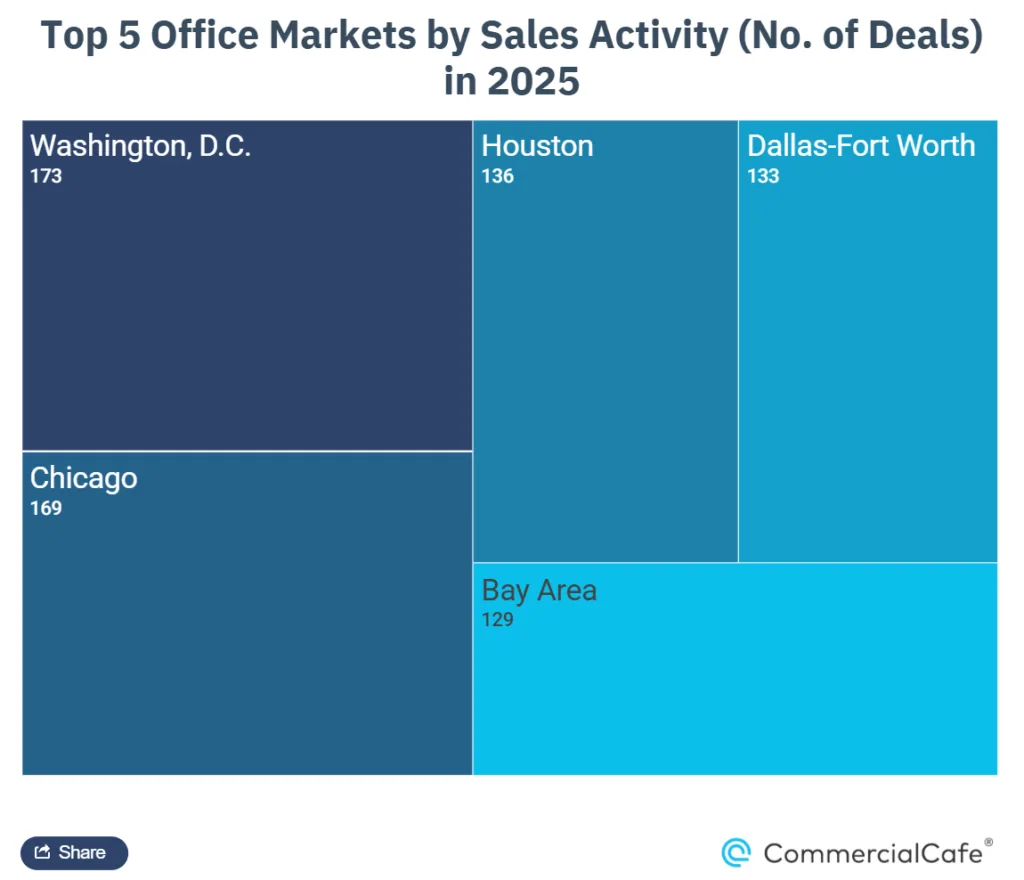

- Washington, D.C. recorded the most office transactions and the largest volume of space traded, while Chicago, Houston, and Dallas-Fort Worth also saw elevated deal activity.

- Investors continued favoring gateway and high-quality assets despite broader office market uncertainty, reinforcing the industry’s ongoing flight-to-quality trend.

US office investors doubled down on gateway markets and trophy assets in 2025, even as the sector continued working through elevated vacancies and refinancing pressure. According to Yardi Research data analyzed by CommercialCafe, office sales nationwide surpassed $53B last year, with average pricing reaching $192 PSF.

The biggest winners were familiar names. Manhattan led the country in both total sales volume and pricing, while Washington, D.C. emerged as the most active market by both transaction count and square footage traded. Chicago, Houston, Dallas-Fort Worth, San Francisco, and Miami also ranked among the country’s busiest or most expensive office investment destinations.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Manhattan Dominated Office Investment Activity

Manhattan office sales totaled roughly $7.8B in 2025, the highest volume in the country. One deal alone — the $1.1B sale of 590 Madison Ave. — accounted for nearly 14% of the borough’s annual sales volume and marked Manhattan’s largest office acquisition in more than three years.

The market also posted the nation’s highest average office pricing at $496.30 PSF. A SoHo office-and-retail property at 165 Mercer St. traded for roughly $1,290 PSF after Spear Street Capital acquired the asset for $40M.

San Francisco followed as the country’s second-priciest office market, averaging nearly $402 PSF. The Bay Area also logged the second-highest office sales total nationally at $5.2B, helped by PG&E’s $906M headquarters acquisition in Oakland.

Washington, D.C. Became the Busiest Office Market

Washington, D.C. stood out less for pricing and more for sheer activity. The market recorded 173 office transactions in 2025 — the most in the US — while nearly 27.4M SF traded hands, also topping the national rankings.

The largest deal by square footage involved the 597K SF office tower at 1000 Wilson Blvd. in Arlington, Va., which Goldman Sachs Asset Management sold as part of a portfolio transaction. The district also posted nearly $4.8B in office sales volume, led by Exelon’s $175M acquisition of Edison Place at 701 Ninth St. NW.

Chicago followed closely behind Washington, D.C. in both transaction activity and space traded. The market logged 169 office sales and roughly 27.3M SF changing hands, making it one of the country’s most liquid office markets despite ongoing distress headlines.

Texas Markets Stayed Highly Active

Houston and Dallas-Fort Worth continued attracting investor capital thanks to population growth, corporate relocations, and relatively lower occupancy costs compared to coastal gateway markets.

Houston recorded 136 office transactions and more than 25M SF traded in 2025, while Dallas-Fort Worth posted 133 deals and nearly 17.7M SF sold. DFW also ranked fifth nationally in total office sales volume at more than $3.8B.

The region’s marquee transaction involved The Link Uptown, a newly completed Class AA office tower in Dallas that sold for $218M while more than 90% leased.

Meanwhile, Miami continued cementing itself as one of the country’s highest-priced office markets. Office assets traded at an average of nearly $356 PSF in 2025, ranking fourth nationally behind Manhattan, San Francisco, and Brooklyn.

Gateway Pricing Still Commands a Premium

While office distress continues reshaping parts of the market, the data reinforces how bifurcated the sector has become. Investors remain willing to pay premium pricing for newer, well-leased, highly amenitized assets in top-tier locations, while commodity office properties continue facing valuation pressure.

Brooklyn ranked as the third-priciest office market nationally at roughly $384 PSF, boosted by redevelopment-driven acquisitions such as the $140.5M sale of 205 Montague St. in Brooklyn Heights. In Palo Alto, First Citizens Bank paid nearly $2,000 PSF for a mixed-use office property on University Avenue.

That pricing gap aligns with the broader flight-to-quality trend that has dominated office leasing and investment activity since the pandemic. Institutional buyers continue concentrating capital in gateway cities, trophy assets, and mixed-use redevelopment opportunities that can outperform in a slower office recovery environment. Leasing momentum has also started improving in select gateway markets as tenants continue consolidating into higher-quality space, helping stabilize demand for premium office assets.

Why It Matters

The 2025 rankings show office capital is still flowing — just far more selectively than during the sector’s pre-2022 peak. Investors are prioritizing liquidity, tenant quality, redevelopment potential, and long-term market fundamentals over broad-based office exposure.

Markets like Manhattan, Washington, D.C., and San Francisco continue benefiting from institutional capital depth and trophy-asset demand, while Sun Belt metros such as Dallas and Houston remain attractive for growth-oriented investors. Per Yardi Research’s 2026 analysis, the highest activity concentrated in markets with either global gateway status or strong demographic and corporate expansion trends.

What’s Next

Office investment activity could accelerate further in 2026 if borrowing costs continue easing and bid-ask spreads narrow. However, capital will likely remain concentrated in high-quality assets as lenders and buyers continue avoiding commodity office properties with weak leasing fundamentals.

Investors will also keep watching refinancing pressure across older office stock, particularly in secondary business districts. That dynamic could create more discounted acquisition and conversion opportunities, especially in markets where multifamily demand and mixed-use redevelopment remain strong.