- The Federal Reserve’s April 2026 Senior Loan Officer Opinion Survey showed large banks easing standards across commercial real estate loan categories, even as smaller banks tightened selectively.

- Institutional borrowers drove stronger demand for core commercial and multifamily loans, while construction and land development lending remained softer.

- Improving credit conditions, rising transaction volumes, and stronger REIT valuations suggest the CRE recovery is broadening despite macroeconomic uncertainty.

Principal Asset Management reports that commercial real estate lending conditions are stabilizing — and in some corners, improving faster than expected. The Federal Reserve’s April 2026 Senior Loan Officer Opinion Survey (SLOOS) showed that large US banks eased lending standards across construction, core commercial, and multifamily loans during Q1, marking an important shift after years of tighter underwriting.

The headline survey result showed lending standards largely unchanged overall, but the underlying data revealed a growing divide between large institutions and smaller lenders. According to the Fed survey, large banks also reported significantly stronger demand for commercial and multifamily loans, signaling renewed activity from institutional-quality borrowers despite ongoing geopolitical and trade-related volatility.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Split Market for CRE Lending

The biggest takeaway from the Fed’s survey was the divergence between lender groups. Large banks loosened standards across all three major CRE loan categories, while smaller domestic banks tightened standards for construction and multifamily loans and held commercial lending steady. Foreign banks also reported modest tightening.

Loan demand followed a similar pattern. Large lenders saw stronger appetite for core commercial and multifamily debt, while smaller banks reported weaker demand for construction and multifamily financing. Foreign banks stood out as an exception, reporting modestly stronger demand across all categories.

That divergence matters because large banks often reopen the lending cycle first. Their willingness to compete for deals typically signals improving confidence in asset valuations, liquidity, and refinancing conditions.

The Details Behind the Easing

The Fed also included annual questions about CRE lending policies and competition. The responses showed a more competitive lending market than the headline data suggested.

Banks pointed to stronger competition from traditional lenders and private credit firms. That pressure shaped loan terms over the past 12 months. Many lenders increased maximum loan sizes and narrowed spreads over funding costs. Others extended interest-only periods for borrowers. Some banks also eased debt-service coverage requirements for construction and multifamily loans.

Meanwhile, lenders cited several drivers behind stronger demand. Those included rising acquisition activity, refinancing needs tied to maturing debt, and lower interest rates. Banks also reported improving confidence in rental demand fundamentals.

According to Real Capital Analytics, regional and local banks made up 19% of CRE lending volume in 2025. That figure rose from 17% in 2024 and exceeded the 2015–2019 average. The increase suggests smaller lenders are re-entering the market as competition intensifies.

CRE Recovery Indicators Keep Improving

The Fed survey aligns with several broader indicators showing a healthier CRE market entering mid-2026. According to the report, major private CRE indices have risen broadly, REIT valuations have surpassed prior-cycle peaks, and transaction activity continues accelerating. That momentum follows improving lending activity seen throughout late 2025, as banks gradually reopened capital channels for stabilized CRE assets.

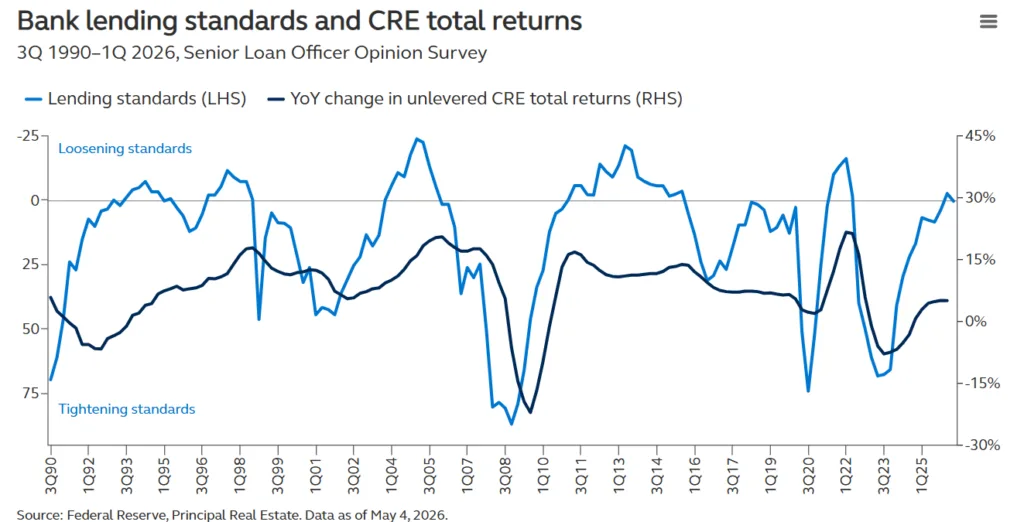

Historically, easing bank lending standards have correlated closely with stronger property returns. The Fed’s long-term SLOOS data, tracking lending conditions back to 1990, shows that periods of credit loosening generally coincide with improving unlevered CRE total returns.

Multifamily and stabilized commercial assets appear to be benefiting first, particularly among institutional borrowers with stronger balance sheets and lower refinancing risk. Construction and land development financing, however, remains more uneven as lenders continue to monitor supply pipelines and project economics carefully.

Why Institutional Borrowers Are Benefiting First

The timing of the survey is notable because it captured lender sentiment between March 23 and April 3, a period marked by elevated geopolitical uncertainty and shifting trade policy concerns. Against that backdrop, the absence of widespread tightening was itself viewed as constructive.

For institutional borrowers, the reopening of large-bank lending channels could improve refinancing flexibility and transaction liquidity heading into the second half of 2026. That’s especially important as billions in legacy CRE debt continue approaching maturity.

The survey also highlights the growing role of lender competition in stabilizing pricing and availability. Nonbank lenders and debt funds have steadily gained market share over the past several years, forcing traditional banks to compete more aggressively for high-quality deals.

What’s Next

The next few quarters will show whether this selective easing broadens into a wider CRE credit recovery. Much depends on interest-rate stability, property fundamentals, and whether economic uncertainty begins affecting occupier demand.

Still, the latest Fed survey suggests the lending environment is moving in a more constructive direction. If large banks continue loosening standards and borrower demand remains firm, refinancing conditions and transaction volumes could improve meaningfully through the rest of 2026.

For CRE investors, the message is increasingly clear: capital is available again — just unevenly distributed toward higher-quality assets and institutional borrowers first.