- Credit spreads are now the key driver of CRE deal activity, more than Fed policy rates.

- Wider spreads and risk premiums are limiting loan proceeds and tightening deal structures.

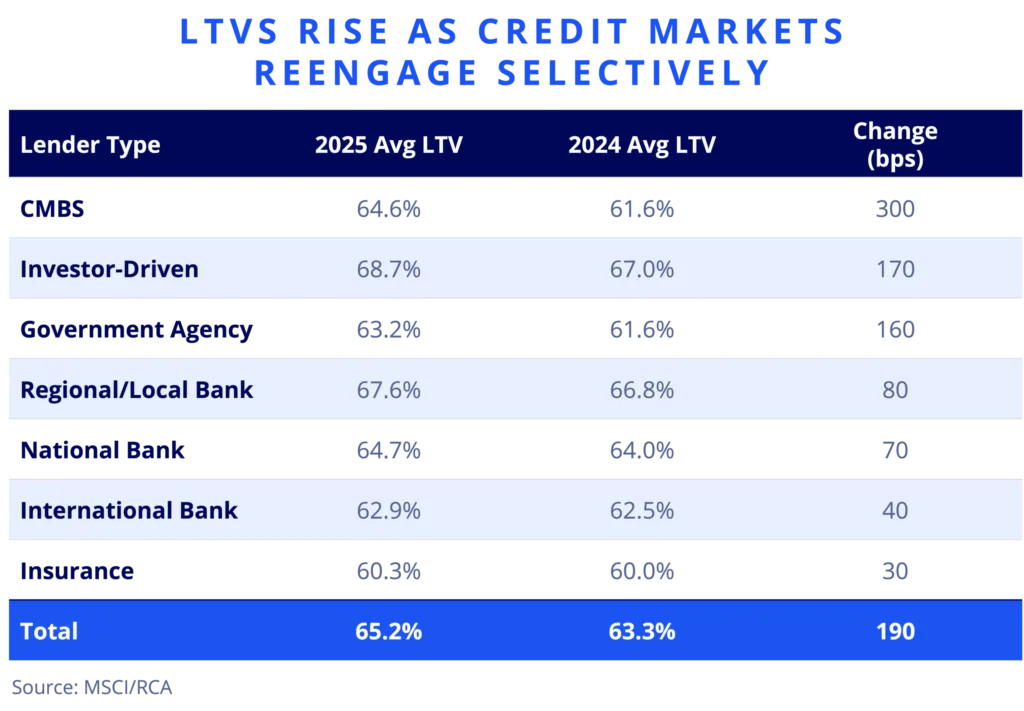

- Leverage has modestly improved but conditions vary across lender types.

- Market recovery depends on lender confidence in risk pricing, not just rate cuts.

Credit Spreads Drive the Market

Colliers’ Knowledge Leader reports that despite steady Treasury yields, credit spreads in commercial real estate (CRE) have widened and become more volatile. This shift has raised all-in borrowing costs, even while base rates remained stable in recent months. Data from Trepp shows that these spreads, rather than monetary policy, are increasingly impacting leverage and overall transaction activity for CRE.

Lender Risk and Leverage Trends

Lenders are responding to continued uncertainty by embedding higher risk premiums into loans. Loan-to-value (LTV) ratios have seen a slight increase, particularly among investor-driven lenders, signaling selective reopening of credit markets. Recent tightening in securitized lending markets has also pointed to improving risk sentiment, with spreads compressing in certain segments as lenders cautiously reengage. However, banks and insurers remain conservative, only marginally loosening underwriting standards.

Limits on Proceeds and Pricing Impact

The modest rise in LTVs has not compensated for wider credit spreads, leaving overall borrowing costs and debt service requirements high. As a result, buyers often need to contribute more equity or accept lower bids to close deals. Transactions are stalling—not due to value disagreements, but because current lending terms no longer match older pricing benchmarks.

Outlook for CRE Activity

Looking forward, CRE deal volume will depend less on future Fed rate moves and more on when lenders feel risk is appropriately priced. Until spreads settle, credit pricing remains the limiting factor for market recovery and new transaction activity. Credit spreads will continue to be a crucial metric for CRE participants throughout 2024.