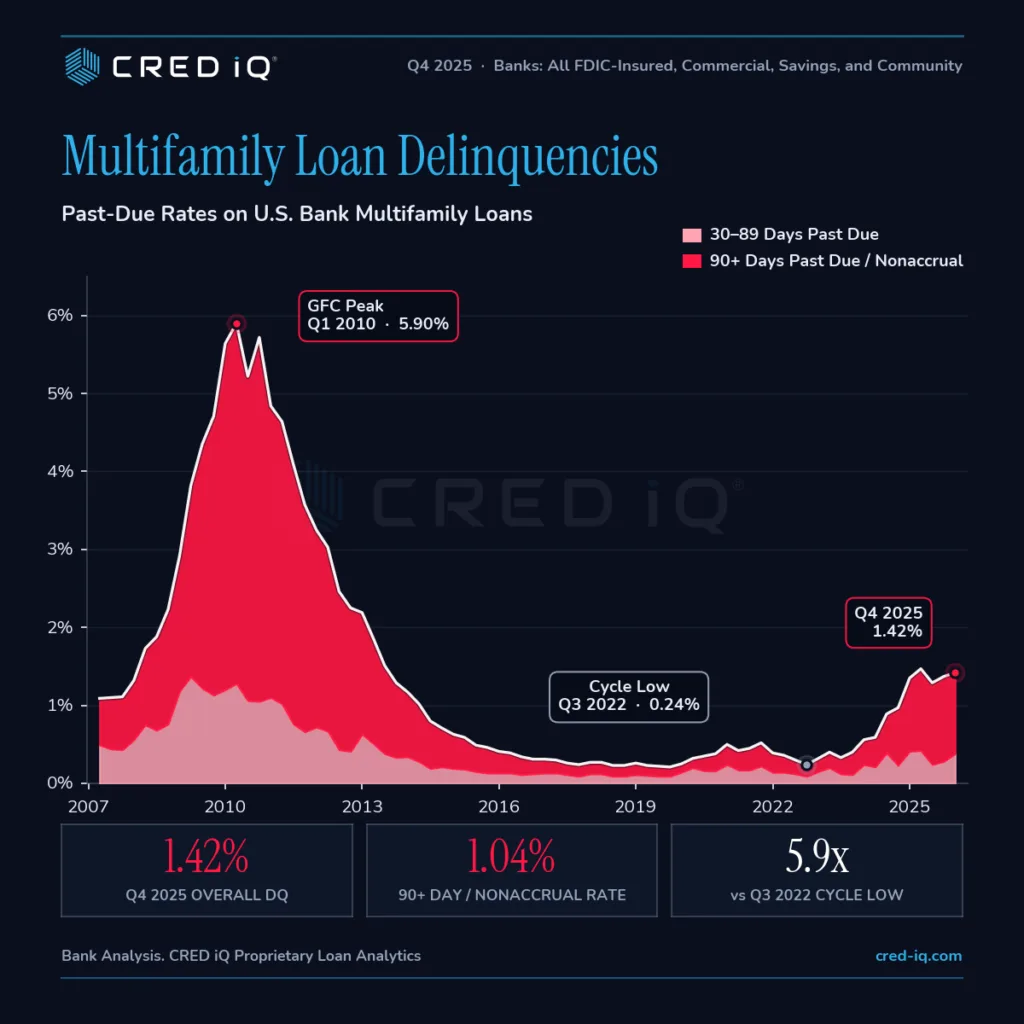

- US bank multifamily delinquency rates rose to 1.42% in Q4 2025, the highest level since Q2 2013, according to CRED iQ.

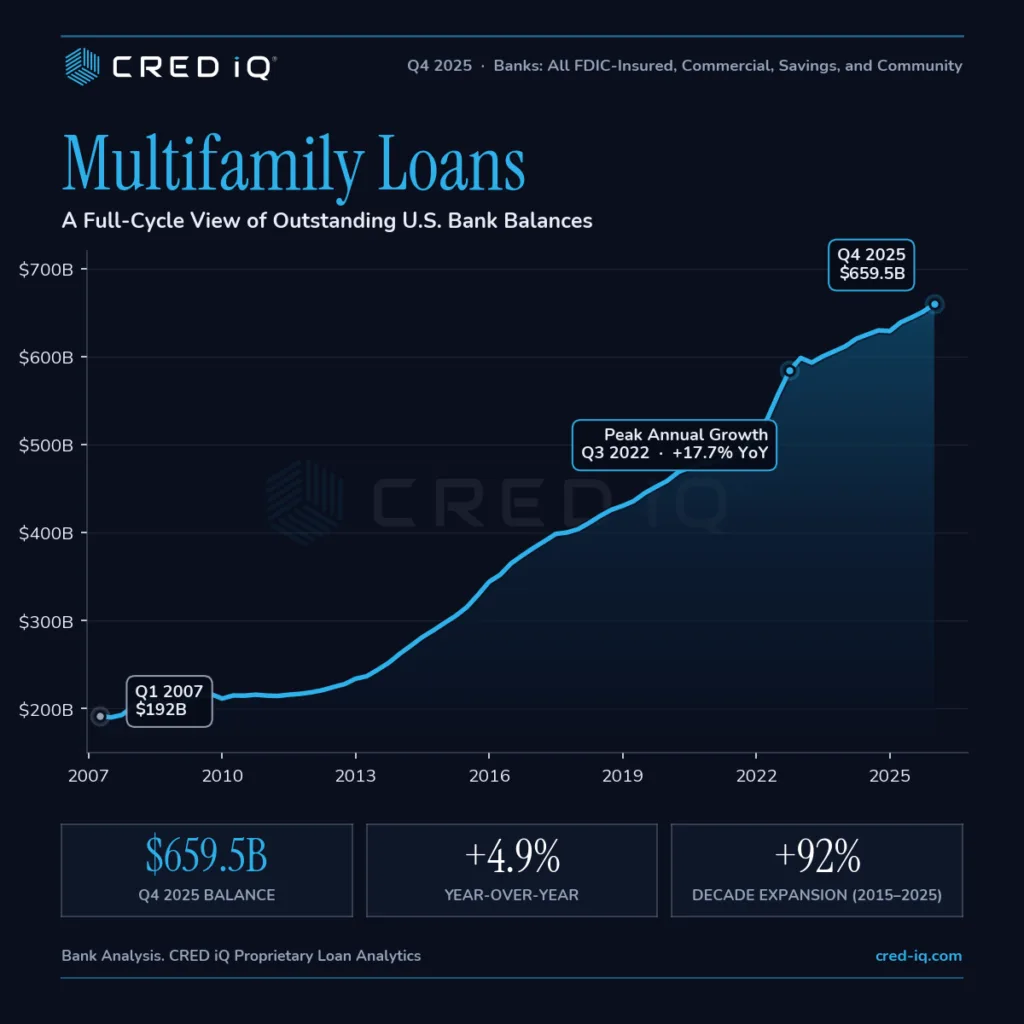

- Banks continued growing multifamily exposure despite mounting stress, with outstanding apartment loan balances reaching a record $659.5B.

- Rising refinancing costs and slowing rent growth in oversupplied Sun Belt markets are increasing distress risk heading into 2026.

US banks are carrying more apartment debt than ever, but the credit quality behind those loans is deteriorating fast. According to CRED iQ’s Q4 2025 analysis, multifamily delinquency rates climbed to 1.42%, the highest reading in more than a decade, while outstanding multifamily balances hit a record $659.5B.

The data highlights a growing disconnect in CRE lending: banks are still expanding apartment exposure even as refinancing pressure and weaker property fundamentals push more borrowers into distress. Multifamily delinquencies have now increased nearly sixfold from the cycle low of 0.24% recorded in Q3 2022.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Decade Of Multifamily Loan Growth

Bank multifamily lending has nearly doubled over the past 10 years. Outstanding balances increased 92% from $344.1B in Q4 2015 to $659.5B by the end of 2025, per CRED iQ. The portfolio also grew by $8.6B quarter-over-quarter in Q4, even as other CRE categories—particularly construction and development lending—contracted for a sixth consecutive quarter.

Growth, however, has slowed materially from the sector’s post-pandemic peak. Year-over-year multifamily loan growth reached 17.7% in Q3 2022 before moderating as higher interest rates and tighter credit conditions cooled transaction activity.

The Details

CRED iQ attributed the rise in bank multifamily delinquencies to several converging pressures. Borrowers refinancing loans today face significantly higher debt service costs than they did during the low-rate era, while rent growth has weakened across many pandemic boom markets that absorbed large volumes of new apartment supply.

The stress is especially visible in Sun Belt metros where multifamily deliveries surged between 2021 and 2024. At the same time, banks have tightened underwriting standards, limiting refinancing options for owners facing looming maturities.

Importantly, the deterioration is concentrated in more severe delinquency categories. The 90+ day past-due and nonaccrual rate climbed to 1.04% in Q4 2025, up sharply from 0.15% in Q3 2022. Meanwhile, the 30-to-89-day delinquency bucket stood at a comparatively modest 0.38%, suggesting many troubled loans have already migrated into deeper distress.

Still Below GFC-Era Distress

While multifamily stress is building, current delinquency levels remain well below the peaks seen during the Global Financial Crisis. Bank multifamily delinquencies topped out at 5.90% in Q1 2010, according to CRED iQ, with the 90+ day delinquency rate alone reaching 4.62%.

Current readings represent roughly 24% of those GFC-era highs. Losses also remain relatively contained for now. Annualized multifamily loan loss rates measured 0.13% in Q4 2025, compared with 1.24% at the height of post-crisis losses in Q4 2010.

Why It Matters

The data underscores the increasingly uneven outlook for multifamily owners and lenders entering 2026. Apartment fundamentals remain healthier than office in most markets, but refinancing risk is emerging as a major pressure point as loans originated during the ultra-low-rate cycle mature into a much higher-rate environment.

For banks, the challenge is balancing continued portfolio growth with weakening credit quality. The rise in apartment stress also comes as broader bank CRE delinquencies climb to their highest levels in more than a decade, reflecting mounting pressure across multiple property sectors. For investors, rising distress could create acquisition and recapitalization opportunities, particularly in oversupplied Sun Belt markets where rent growth has stalled and property values have reset.

What’s Next

The next phase of multifamily stress will likely hinge on three factors: interest rates, rent growth, and lender flexibility. If rates stay elevated and apartment supply continues outpacing demand in key markets, more loans could migrate into serious delinquency through 2026.

Market participants will also be watching how aggressively banks pursue modifications and extensions versus forced dispositions. Distressed multifamily volume remains manageable today, but the steady rise in 90+ day delinquencies suggests more workout activity is likely ahead.