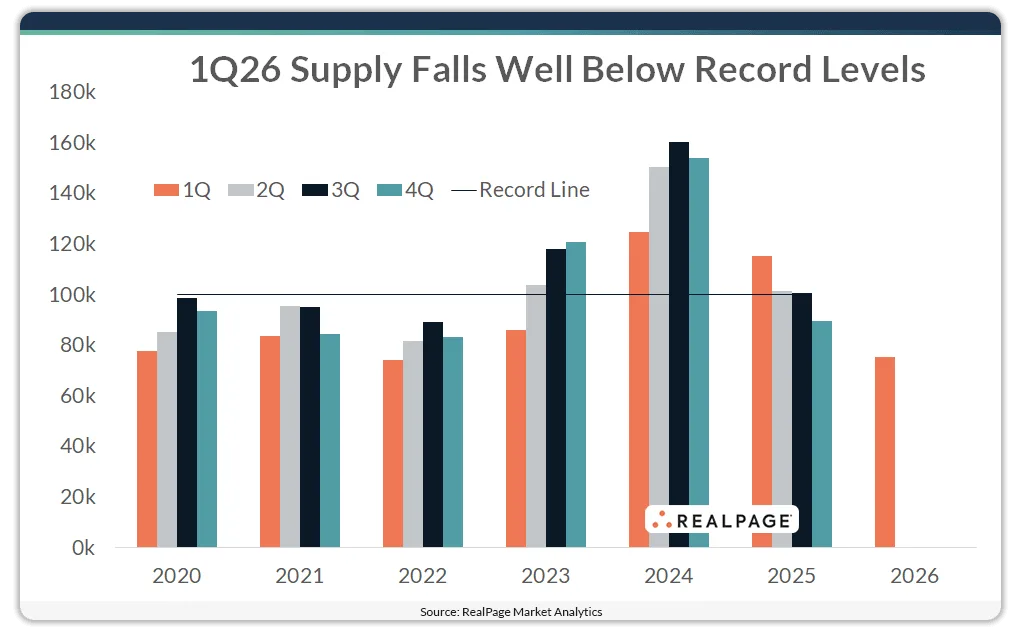

- Roughly 75,200 apartment units were delivered in Q1 2026, the lowest quarterly total since early 2022.

- The slowdown marks a clear break from the 2023–2024 construction boom that pushed deliveries above 100,000 units for multiple quarters.

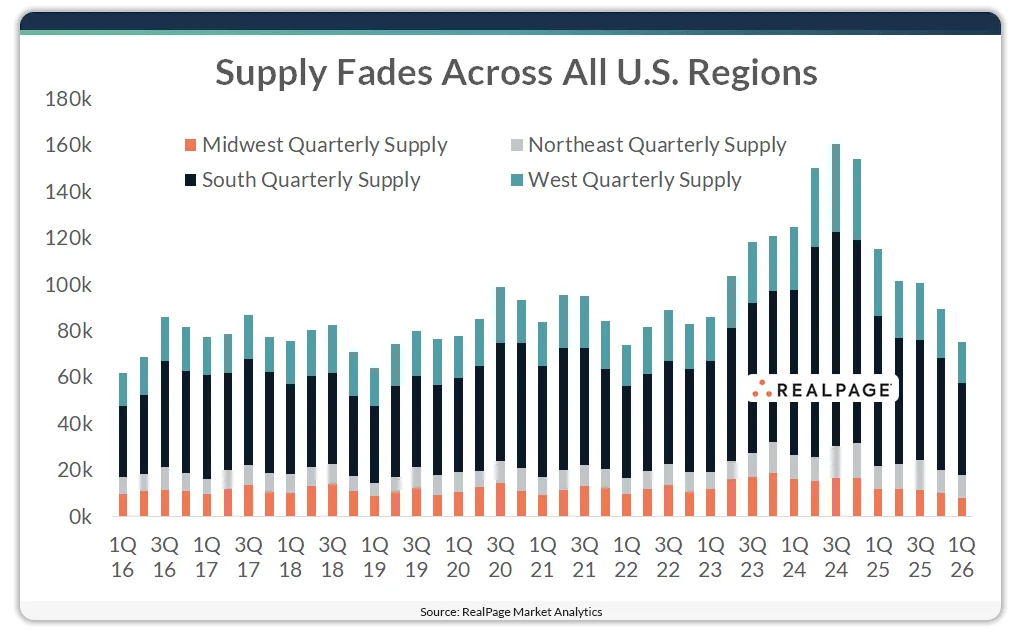

- While the South remains the most active region, it has also experienced the steepest decline in new supply.

According to RealPage, after several years of aggressive multifamily construction, the pace of new apartment deliveries is losing steam. The first quarter of 2026 brought a notable pullback, with completions dropping to their lowest level in four years.

From Boom to Cooldown

Developers completed just over 75,000 units in Q1 2026, a significant decline from the elevated levels seen during the recent supply surge. Between mid-2023 and late 2024, quarterly deliveries consistently exceeded 100,000 units—peaking in Q3 2024. That momentum began to taper off by the end of 2024, with volumes steadily declining through 2025 and into this year.

Regional Trends Shift

The South continued to lead the nation in new supply, delivering nearly 40,000 units in the first quarter—more than double the West’s output. Still, the region has seen the sharpest contraction, with volumes dropping each quarter since hitting a high in 2024.

The West followed with approximately 17,700 units delivered, also down from the previous quarter. Meanwhile, the Northeast and Midwest posted more modest totals, with fewer than 10,000 units each.

Top Markets Hold Strong

Despite the broader slowdown, key Sun Belt metros remain active. Phoenix and Dallas led the nation in Q1 completions, each surpassing 5,000 units delivered during the quarter, with Phoenix in particular continuing to see strong renter demand even as new supply begins to taper.

Why It Matters

The pullback in new supply suggests the multifamily sector is entering a rebalancing phase after years of rapid expansion. With fewer units coming online, pressure on occupancy and rent growth could begin to ease, offering some stability to property fundamentals.

What’s Next

As construction pipelines thin and developers reassess new starts, the market is expected to normalize further. The recent slowdown may help absorb excess inventory from the peak building years, setting the stage for a more measured growth cycle ahead.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes