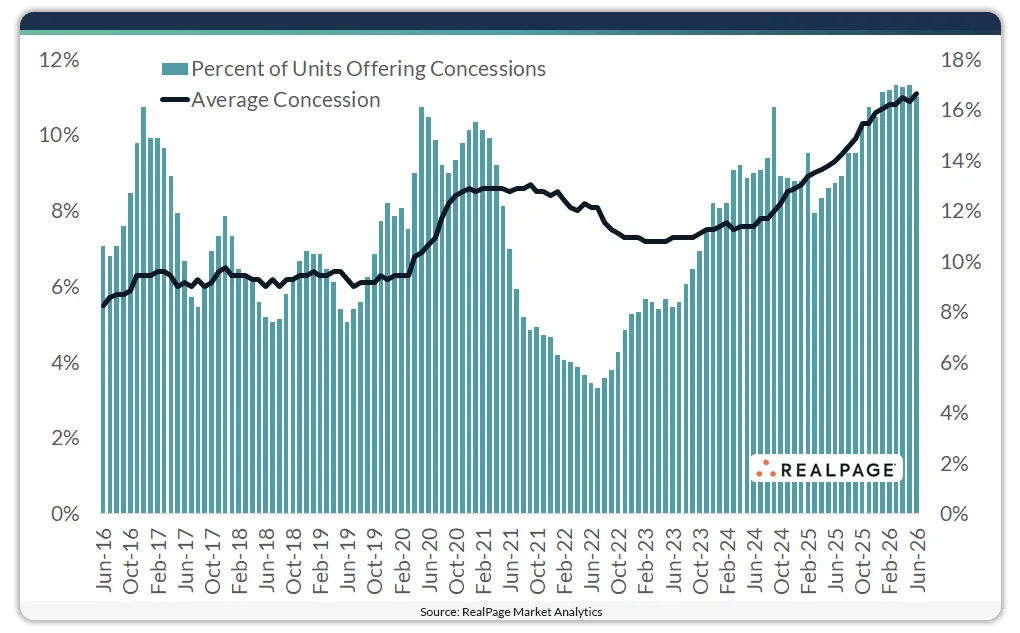

- Over 16% of US stabilized apartments offered concessions in June 2026, near post-2014 highs.

- The average concession discount jumped to 11.1%, the deepest in more than 25 years, per RealPage Market Analytics.

- Elevated concessions signal lingering supply-demand imbalances and competitive pressure across all product classes.

Pandemic-Era Discounts Stick Around

The US apartment market’s pandemic-era trend of elevated lease concessions is showing little sign of abating as peak leasing season ramps up, according to RealPage Market Analytics. Concerns about oversupply and competitive lease-up activity are keeping operators reliant on discounts. June 2026 saw concession utilization remain high, continuing a stretch not seen since the industry was digging out from the last economic downturn in the early 2010s. Concession rates have generally trended upward since bottoming a decade ago, marking a clear signal of how persistent supply-side pressure has changed market tactics for property managers.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

Nationally, 16.5% of stabilized units provided a concession in June 2026, representing a modest decline from May but a significant 3.4 percentage-point increase from the prior year. The average discount reached 11.1% of annual lease value—nearly six weeks free on a 12-month lease—and is now at its highest level since the late 1990s. Across the spectrum, Class C units saw the highest concession usage rate at 20.7%, with Class A and Class B following at 13.7% and 15.1%, respectively. However, Class A leads in the average discount depth at 11.4%, slightly ahead of Class C’s 11.3% and Class B’s 10.7%.

Concessions Widen as Supply Grows

The competitive landscape appears to be driving concession growth more than demand-side weakness. Data from RealPage show elevated concessions aligning with ongoing new supply absorption challenges, especially in Sun Belt metros and growth markets that have added significant multifamily inventory since 2020. Since the post-Great Financial Crisis era, concession rates had dropped to a decade low of 5.5% by mid-2016 but have since climbed steadily, reflecting the impact of a national construction surge. While supply pressure is most acute in Class A, lower-end product is not immune—Class C’s high concession usage hints at affordability challenges and increased renter mobility as discounts proliferate.

Why It Matters

Persistently high concession rates signal ongoing operational and pricing challenges for owners, especially in oversupplied markets. According to RealPage Market Analytics, the current 11.1% average discount essentially means properties are surrendering more than a month’s rent per lease—a level not approached since the immediate aftermath of the Great Financial Crisis. For comparison, the June 2026 value is over double the cycle low of 5.5% seen in 2016. With Class A leading on discount size and Class C shouldering the highest share of concessions, margin pressure is becoming widespread and not contained to any one segment. The broad deployment of concessions underscores operators’ struggles to maintain occupancy amid an influx of new deliveries, and may suggest further rent growth deceleration or softness ahead.

For investors and asset managers, the composition of concessions by class offers a clearer window into tenant demand sensitivities and the strategic limits of price reductions. Class B’s relatively lower concession rate may indicate more pricing power or less direct impact from new stock, though all segments are well above historic averages. Considering property tax hikes and inflation-driven operating cost increases, deeper and more frequent concessions risk eroding net operating income even in markets with strong population growth.

What’s Next

With multifamily deliveries forecasted to remain strong through the end of 2026, industry analysts expect elevated concessions and deep discounts to persist at least through the next few quarters. Operators may continue relying on months-free incentives but could face resistance from lenders and investors to further margin compression. Eyes will be on whether absorption accelerates in high-supply markets and when, if at all, the upward trend in concession depth stabilizes. If demand doesn’t keep pace with supply, the industry could see further normalization of hefty renter incentives as a standard lease-up tactic into 2027.