- Midwest multifamily is seen as a safe haven, but Trepp’s new report finds its true credit risk closely matches the Sunbelt at the serious delinquency stage.

- While the Sunbelt shows higher rates of early-stage credit stress, the Midwest’s lower pricing and limited institutional capital could compress as investor flows rise.

- Structural demographic and economic headwinds may temper long-term Midwest performance, suggesting current advantages are likely cyclical.

Safe Haven Narrative Drives Midwest Attention

Sunbelt apartment markets are cooling—for now. Oversupply, concessions, and rent stagnation have pushed multifamily investors toward the Midwest, where headlines tout stability amid national volatility. According to Trepp’s 2026 “The Midwest Multifamily Investment Mirage” paper, the region is being rebranded as a defensive capital destination as Sunbelt distress grows. The new narrative: the heartland’s smaller cities are insulated from the rent and vacancy swings chilling investor confidence down South. But as always, nuance matters.

Per Trepp, this safety thesis hinges on the Midwest’s lower early warning signals in CMBS data and more conservative pricing, alongside limited recent construction. It’s an appealing package—on the surface. But a closer look at loan performance metrics reveals the region’s resilience may be as much a product of the Sunbelt’s excess as of true structural advantage.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Historical Stability or Cyclical Opportunity?

The “safe haven” narrative reflects real historical trends. Midwest apartments often outperformed coastal and Sunbelt markets during downturns. Stable rents and slower growth reduced volatility during market swings. However, Trepp says those same traits may limit long-term upside. Aging housing stock and slower job growth remain headwinds. Early warning indicators differ between the regions. Yet realized loan outcomes look remarkably similar.

The Midwest’s smaller institutional footprint has historically supported lower pricing. That attracted investors seeking higher yields and lower entry costs. However, rising capital inflows could compress those advantages. Weak population growth and slower hiring may further limit future performance. Short-term fundamentals remain healthy, but structural challenges persist.

The Details

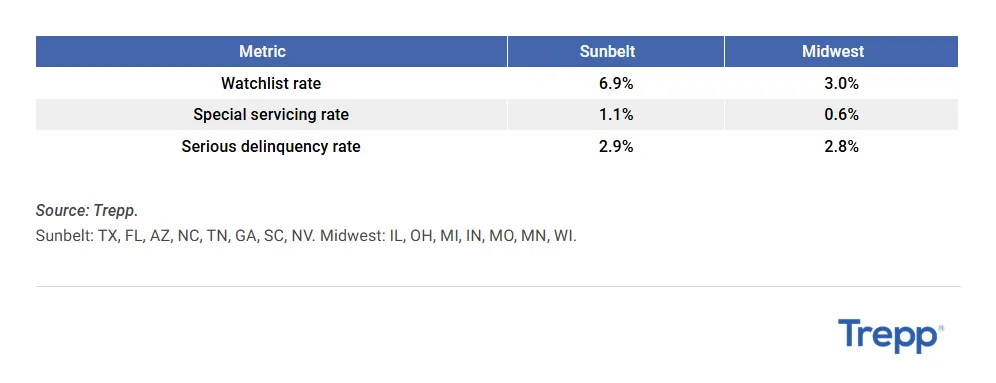

Trepp’s analysis parses CMBS performance data to measure where true risk differences show up. Sunbelt multifamily loans currently exhibit notably higher CMBS watchlist (6.9% of the loan pool) and special servicing rates (1.1%) versus Midwest counterparts (3.0% and 0.6%, respectively). But at the level of serious delinquency—where loans are actually in distress—the separation is effectively nil: 2.9% in the Sunbelt versus 2.8% for the Midwest.

This means early warnings may reflect reporting differences, risk management, or an overhang from aggressive recent Sunbelt lending, rather than an entrenched Midwest edge. Additionally, Sunbelt markets hold 2.5x as many CMBS multifamily loans maturing from 2026–2029 compared to the Midwest, hinting at a wave of pending refinancing risk and potential repricing opportunities in the coming years.

Wave of Maturities Could Reshape the Narrative

Comparisons uncover how temporary market cycles shape investor preference. Today’s Sunbelt headwinds—record supply completions and flatlining rents—contrast sharply with the Midwest, where fewer new units and tighter occupancy have kept short-term financials attractive. But as noted in the Trepp paper, CMBS maturities are stacking up disproportionately in high-growth southern metros. Between 2026 and 2029, more than twice as many Sunbelt loans face maturity relative to the Midwest.

This timing could tilt repricing opportunities toward markets that look distressed today but benefit from long-term demographic advantages, including in-migration and economic expansion. Investors zeroed in on headline stability may underestimate longer-term risks lurking in the Midwest’s slow-growth narrative, while over-discounting the Sunbelt’s cyclical pain.

Why It Matters

Regional safety narratives rarely hold up over full market cycles. Trepp found that serious distress rates are nearly identical across both regions. That distinction matters more than early warning indicators for underwriting decisions. The Midwest benefits from lower entry costs and stable occupancy trends. However, slower job growth and weaker demographics could limit upside. Meanwhile, the Sunbelt may offer value as refinancing pressures mount. More than twice as many Sunbelt loans mature through 2029 than Midwest loans. Today’s distressed markets could become tomorrow’s outperformers as pricing resets.

What’s Next

The coming wave of Sunbelt CMBS maturities between 2026 and 2029 will test regional risk narratives and could trigger renewed capital flows into currently out-of-favor metro areas. Investors in Midwest multifamily should watch for signs of pricing compression as institutional capital continues to enter what was once a yield backwater. Meanwhile, Sunbelt markets—rife with distress for now—may soon offer better relative value as refinancing pressure creates motivated sellers and repricing resets fundamentals. Across both regions, risk-adjusted performance will depend more on local demand resilience and execution than on broad-brush ‘safe haven’ labels. Trepp’s analysis reinforces the need for CRE investors to look past headlines and assess each market’s structural strengths—and vulnerabilities—over the full cycle.