- Construction costs in the US are tracking above forecasts, with year-over-year increases exceeding 5% and potential to hit 8% by late 2026.

- Tariff pass-through, labor shortages, and geopolitical disruptions are compounding to drive material and labor costs higher, with limited prospects for relief this cycle.

- A narrow procurement window exists for owners who act quickly before cost and contractor availability worsen in high-demand regions and sectors.

Structural Cost Escalation Defines 2026 Outlook

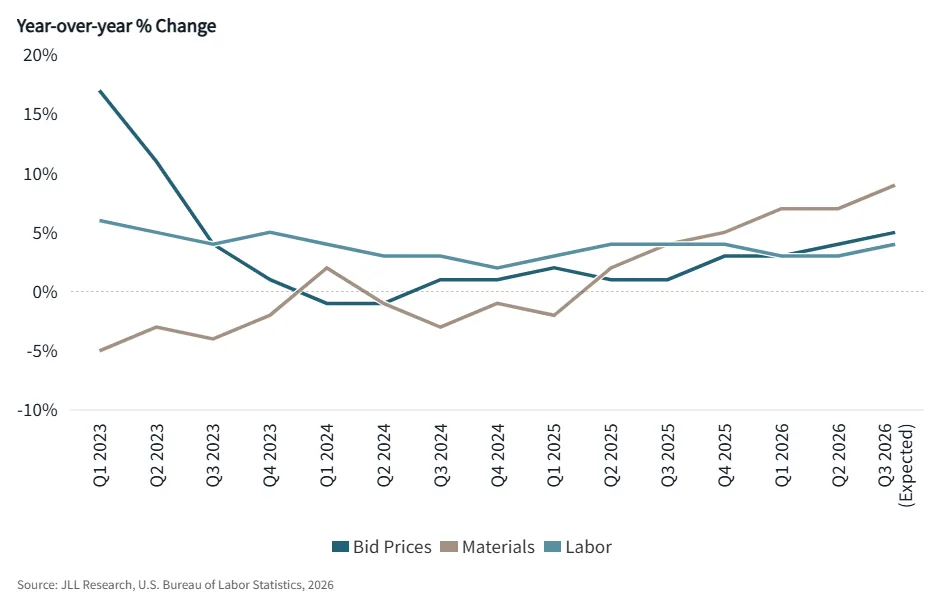

According to JLL’s 2026 US Construction Perspective mid-year update, cost escalation across construction projects is now above the forecasted range set late last year. The baseline for final project costs—including both material and contractor margins—is running roughly 5% year-over-year, and the sector is bracing for further acceleration in the back half of 2026. Relief mechanisms anticipated in prior outlooks—like lower interest rates or tariff concessions—have disappeared, locking in a high price “floor” with no clear ceiling in sight. For US owners and developers, this marks a departure from the range-bound risk of previous years, as construction costs are now exposed to persistent external and structural pressures without practical policy offsets.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

Final-cost indices, factoring in margins, are tracking above 5% year-over-year and could reach JLL’s previously forecasted upper bound of 8% by late 2026. Tariffs are a key contributor: Section 232 tariffs on steel, aluminum, and copper remain at a 50% rate with no expiration, while changes to Section 301 could push duties even higher in coming months. Geopolitical volatility is amplifying cost layers, especially for materials with high energy intensity—copper prices have surged 36% and aluminum 45% year-over-year. At the same time, labor constraints have hardened, with 61% of US metro markets currently supply-constrained and that share expected to hit 72% by 2027. Employment growth in the building trades is lagging historic norms at just 0.6% so far in 2026, per JLL.

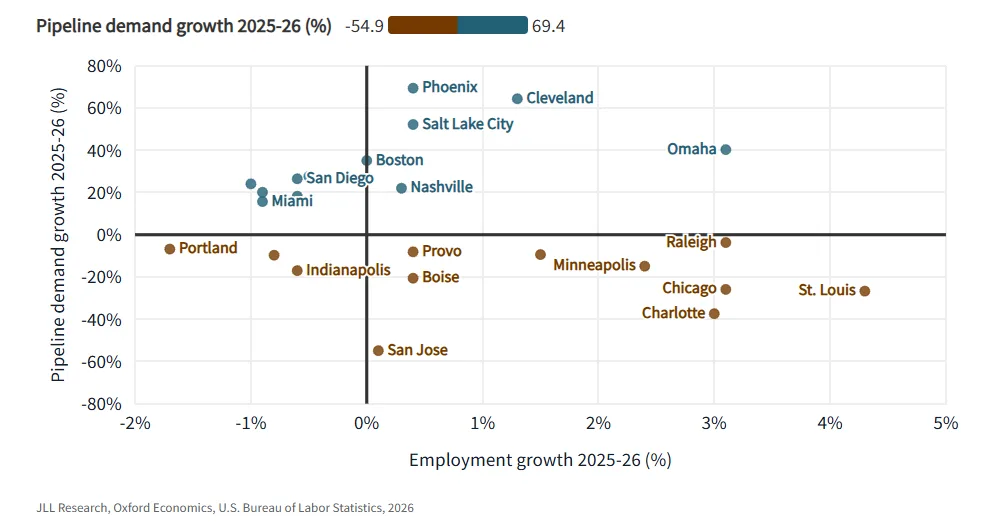

Bifurcation of Demand and a Shrinking Procurement Window

Construction labor shortages have become structural rather than cyclical, with local rules limiting worker mobility. Data centers and power projects compete with traditional CRE developments for specialized labor. Electricians, HVAC technicians, and specialty contractors remain especially scarce. JLL says contractors are building larger margins into bids as cost relief expectations fade. Owners now face a shrinking window to secure pricing and contractor availability. Smaller contractors outside major project pipelines may offer the best near-term opportunities.

Why It Matters

US construction budgets face structural pressures from tariffs, labor shortages, and geopolitical disruptions. No single domestic policy is likely to offset those costs. Material inputs rose 6.4% year over year in May, versus 3.5% for final demand prices. According to JLL, contractors are unwilling to absorb further margin compression. Instead, higher material costs are flowing through to bid prices. Hopes for lower interest rates have also faded. The Fed raised its median year-end rate projection to 3.8% in June, from 3.4% in March. USMCA renegotiations exclude steel, aluminum, and copper tariffs. Meanwhile, more than 60% of metro markets face construction labor shortages. JLL expects that figure to rise to 72% by 2027. For many owners, acting now means securing costs and contractor access before conditions worsen.

What’s Next

The construction cost landscape is set to remain volatile and elevated into 2027, with global and domestic influences compounding underlying structural shortages. Owners targeting projects that do not compete with data center or power infrastructure demand, and that can engage regional or midsize contractors, have a fleeting window to strike under relatively less competitive conditions. Once existing pipelines absorb the available labor and cost escalators become further embedded, pricing and margins are likely to ratchet higher, particularly as pending Section 301 determinations could exacerbate tariff-driven material costs. Proactivity in procurement—especially ahead of contractor workloads pushing into 2027/2028—is now a strategic imperative for controlling costs on new US development.