- US self storage asking rents rose 0.8% in May to $16.34 PSF, but rates remain down year-over-year across most major markets.

- The national development pipeline is steady at 45.6M SF (2.2% of stock), with Phoenix and Sarasota-Cape Coral leading new supply.

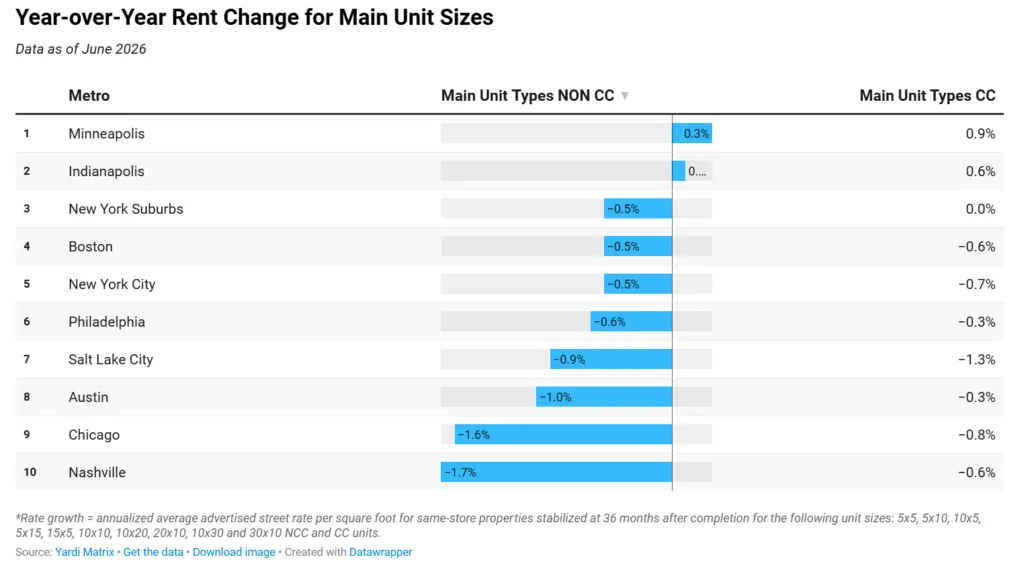

- Persistently negative annual rent growth signals that oversupply and tepid demand are still weighing on operators.

Urban Pipeline Remains Firm

According to Yardi Matrix, May saw the average annualized asking rent for US self storage tick up 0.8% month-over-month to $16.34 PSF. This marks a rare positive for the sector, but it’s a small rebound in the context of broader downward annual rent trends. For most of the Top 30 metros, advertised rates are still below year-ago levels. Ongoing pipeline activity remains robust: as of May, properties under construction or planned totaled 45.6M SF, which is 2.2% of national self storage stock—unchanged since April.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

Out of the 30 largest US metros tracked by Yardi Matrix, 26 registered month-over-month increases in self storage rental rates. Only Phoenix posted a decline, while Detroit, San Diego, and Seattle rents were flat. On an annual basis, however, the story flips—28 of those 30 markets saw negative year-over-year growth. Non-climate and climate-controlled unit rates both fell 1.8% year-over-year. This indicates that while monthly asking prices are stabilizing, the fundamentals remain soft compared to May 2025.

Supply Leaders Hold Their Edge

Despite robust development, supply growth paused in May, with the pipeline holding steady at 45.6M SF—down just 0.3% from a year earlier. Development remains heavily concentrated: Phoenix led with new supply equal to 6.7% of its existing inventory, up 30 basis points for the month. Sarasota-Cape Coral followed at 5.2%, although its figure slipped slightly from April. Other metros like New York suburbs, Austin, Nashville, Los Angeles, Boston, and Portland reported slight increases in their pipelines. Still, development across the Top 30 metros remains uneven, with many markets seeing flat or negative growth.

Why It Matters

The national self storage sector has cooled after its pandemic-driven boom. As of May 2026, asking rates are still under pressure from oversupply and moderating demand. While the 0.8% monthly rent uptick offers a glimmer of stabilization, most major markets show negative annual growth. That measured improvement also reflects broader signs of stabilization appearing across several commercial real estate pricing indicators.

According to Yardi Matrix data, the concurrent steadiness in construction—45.6M SF, or 2.2% of total inventory—means new competition will keep pricing in check for the foreseeable future. Phoenix and Sarasota-Cape Coral’s outsized pipelines illustrate the risk of further supply-driven softness, especially in Sun Belt growth markets. For owners and investors, margin pressure persists as rent growth cannot keep pace with operating costs in most metros. The trendline suggests the industry is moving from boom to balance, but not yet into a renewed growth phase.

What’s Next

With development activity plateauing in May and most rents still below year-ago levels, expect operators to focus on revenue management and marketing to fill vacancies and defend rates. If absorption picks up in pipeline-heavy metros like Phoenix, there could be incremental relief on pricing later in 2026. Until then, muted demand and a steady stream of new units mean sector stabilizing, not surging, looks most likely through year-end.