- The US CMBS delinquency rate declined by 20 basis points to 7.35% in June 2026, according to Trepp.

- Lodging saw the biggest improvement, while retail, multifamily, and office delinquencies increased.

- Non-performing matured balloon loans continue to dominate new delinquencies, affecting overall market recovery.

Lodging Cures Lead Short-Term Decline

The commercial mortgage-backed securities (CMBS) market saw some relief in June, with Trepp reporting that the overall US delinquency rate declined by 20 basis points to 7.35%. This marks one of the more significant month-over-month drop-offs in the past year, driven primarily by the cure of a large lodging portfolio in Florida that had weighed heavily on prior readings. According to Trepp’s June 2026 report, the seriously delinquent rate—covering loans 60+ days delinquent, in foreclosure, real estate owned (REO), or non-performing balloon—also moved lower, landing at 7.16%, a 14-basis-point improvement.

This is only the second time in the past year that the headline number has posted a clear month-over-month decline, despite consistent pressure from maturing debt. Six months ago, the rate stood at 7.30%. While the latest drop signals incremental improvement, Trepp’s analysis indicates the risk profile for CMBS remains far above pre-pandemic levels, especially as distressed maturities persist across retail, office, and multifamily sectors.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

June’s headline decline came mainly from lodging. The lodging delinquency rate fell 79 basis points to 5.22%. Several large loans paid off or cured, including a major Florida hotel portfolio.

Industrial also improved. Its delinquency rate fell 11 basis points to 1.20%, remaining a market bright spot. Meanwhile, multifamily delinquency rose 28 basis points to 7.23%. Troubled assets entered delinquency after last month’s temporary improvement.

Retail also weakened. Its delinquency rate rose 30 basis points to 6.91%. Several regional malls and outlet centers became delinquent, reflecting broader mall distress. Office delinquency also increased to 11.57%. Central business district properties continued driving most of the stress.

New delinquencies reached $2.64B in June. The five largest assets accounted for $998.9M. They included malls, office towers, and Manhattan multifamily properties. Non-performing matured balloon loans represented 65% of new delinquent balances. Another 22% were only 30 days delinquent.

Renewed Maturity Pressure Across Property Types

Loan maturities remain a major CMBS challenge. Including performing matured balloon loans would lift June’s delinquency rate to 9.53%. That sits 218 basis points above the headline figure.

The gap highlights growing refinancing pressure across CRE. Many borrowers still pay interest but cannot refinance or repay principal.

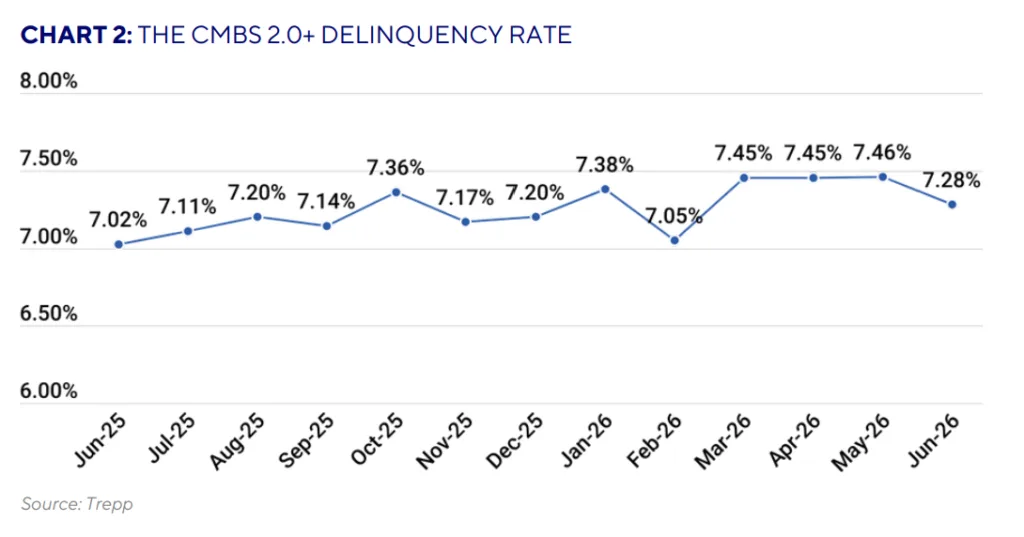

CMBS 2.0+ loans performed near the broader market average. Their delinquency rate fell to 7.28% in June. However, pressure remains uneven. Office posted an 11.47% CMBS 2.0+ delinquency rate. A handful of large deals drove most new defaults. By contrast, industrial remained resilient with limited new delinquent loans.

Why It Matters

The overall CMBS delinquency rate declined modestly in June. That offers some relief for lenders and investors. However, the trend remains uneven.

Trepp’s data shows large lodging portfolio cures drove the improvement. Without those resolutions, delinquency rates would have changed little. Recent declines in special servicing also reflected rising loan cures, reinforcing signs that select distressed assets are stabilizing.

Retail, multifamily, and office continue facing mounting pressure. Office delinquency reached 11.57%, the highest among major property types. That exceeds last year’s 11.08%. Hybrid work and weaker CBD leasing continue weighing on performance.

Retail and multifamily also saw new large delinquencies. Regional malls and multifamily properties led much of the increase. Consumer shifts, e-commerce growth, and affordability challenges continue pressuring both sectors.

Performing matured balloon loans remain a significant risk. They equal 2.18% of outstanding balances. These borrowers remain current but often lack refinancing options. Higher rates and tighter credit continue limiting solutions. If these loans default, overall delinquency could rise quickly.

Property type and loan structure now matter more than issuance vintage. The gap between CMBS 1.0 and 2.0+ has become less significant.

What’s Next

June’s cure-driven decline offers temporary relief, but structural pressures remain. July and August already include several large loan maturities. Many office and retail loans face limited refinancing options.

Borrowers approaching maturity will remain the market’s main focus. Trepp continues tracking growing matured balloon loan volumes. Office and retail deserve close attention as aging towers and big-box properties enter delinquency.

The second half of 2026 will depend on rate stability, refinancing activity, and sector-specific demand recovery.