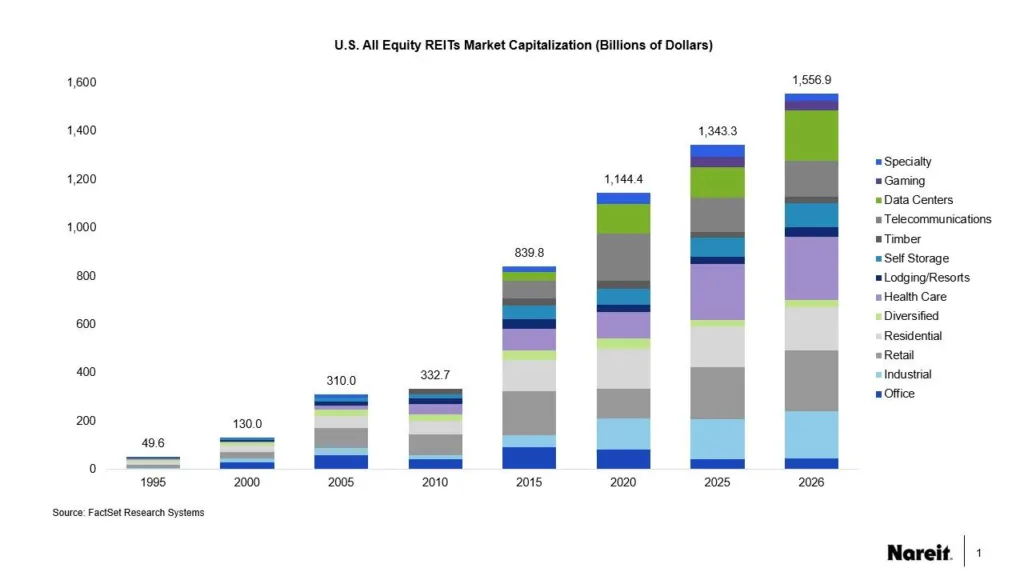

- The FTSE Nareit All Equity REITs Index reached $1.5 trillion in market capitalization in 2026, more than 25 times its 1995 value.

- New property sectors—including data centers, health care, and telecommunications—now make up over 50% of the index’s market cap.

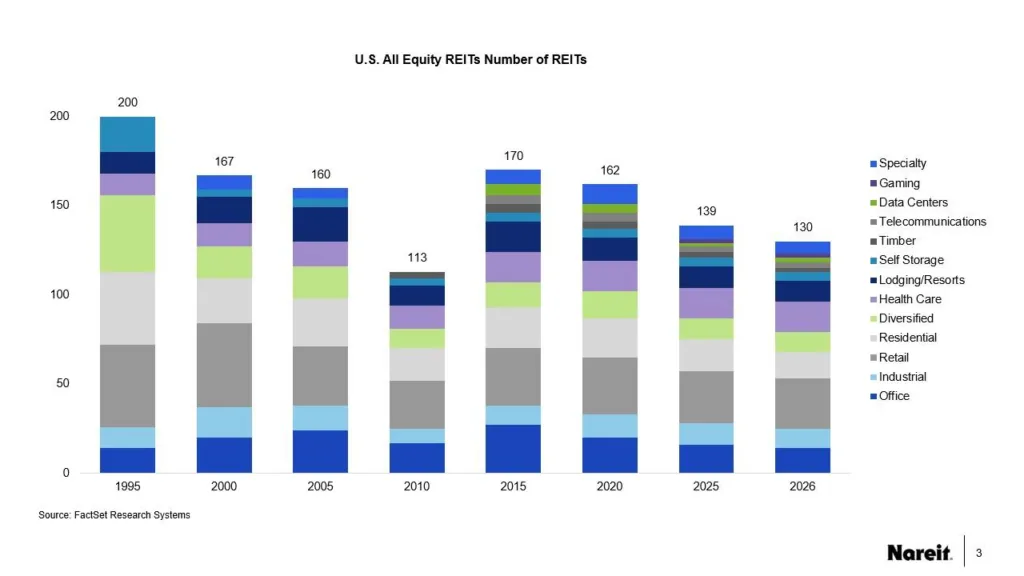

- Market growth has outpaced the number of REITs, signaling industry health is more linked to sector evolution than headcount.

REITs Transform Along With the Economy

According to FTSE Nareit, US REITs have undergone a significant shift over the past three decades, evolving to reflect broader trends across property types. What started as an index dominated by offices, retail, and residential assets has transitioned to a landscape where new and emerging sectors now hold the largest share. After briefly stumbling during the global financial crisis, market capitalization in the FTSE Nareit All Equity REITs Index has climbed steadily, reaching $1.5 trillion by mid-2026. Year to date, the index is up roughly 13%, highlighting investor appetite for real estate amidst ongoing market flux.

This composition shift isn’t just numerical. In 1995, traditional sectors claimed about 75% of the index’s market value. Fast forward to 2026, and properties like data centers, telecom, health care, and gaming collectively represent just over half the index. As appetite grows for specialized real estate, these newer asset types are reshaping the investable landscape.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

Market cap for the FTSE Nareit All Equity REITs Index has exploded from $49.6B in 1995 to $1.5 trillion in 2026. New sectors have propelled much of this growth. Health care REITs have grown from representing only 3% of the index and $4.7B in 2000 to over 17% and $261B in 2026. Data centers—introduced to the index in 2015—now total $127B in market cap, nearly 9% of the index, driven by demand from AI, cloud storage, and global connectivity. Telecom REITs likewise scaled rapidly, peaking at 17% of the index and nearly $200B in 2020, even as the number of publicly listed telecom REITs consolidated from five to three.

In the retail sector, total market cap jumped from $14B in 1995 to $252B in 2026. Yet its share within the index fell from a high of 28% in 1995 to a low of 10% by 2020, as other sectors outpaced its growth. The number of REITs themselves has fluctuated, peaking at 200 in 1995, declining to 113 by 2010, and holding just below a 21-year average of 142 today—demonstrating that market health rests more with sector growth than with sheer REIT count.

New Sectors Reshape the Landscape

The last decade has seen an undeniable tilt toward specialized real estate. While traditional asset classes like office, retail, and residential maintain their market cap ranking, their proportional dominance has waned. Data centers, health care, gaming, and telecommunications now capture the attention—and dollars—of investors seeking diversification beyond core property types.

Case in point: The data center sector’s market cap leapt from $36B across six firms in 2015 to $127B by 2026, fueled in part by a major IPO and a REIT shifting focus to digital infrastructure. Health care’s dramatic ascent leans heavily on demographic tailwinds, with demand for senior housing and medical facilities driving new capital. Meanwhile, the telecom sector’s brief spell as the index’s largest property type underscores how rapidly new asset classes can emerge and, if market conditions shift, consolidate. This contrasts with sectors like retail and residential, where absolute growth is strong but dwarfed by exponential expansion elsewhere.

Why It Matters

The evolution of the FTSE Nareit All Equity REITs Index marks more than just a rise in numbers. According to FTSE Nareit, the US listed REIT sector’s 25-fold increase in market cap since 1995 speaks to significant capital inflows and a broadening investor base. The ascendancy of specialized property types reveals a market that has successfully adapted to technological, demographic, and social change—particularly in sectors like data centers, which captured 9% of the index less than 15 years after their introduction.

Health care’s rise to a 17% market share reflects a strategic reallocation of capital as America’s population ages. Investor interest in defensive, needs-based assets has helped insulate the REIT sector from broader market swings, a trend likely to persist as demand for medical space, senior living, and digital infrastructure intensifies. That resilience has also supported expectations for a stronger performance backdrop as valuation discounts continue to narrow. The fact that market cap growth far outpaces the number of active REITs demonstrates scale, consolidation, and higher asset concentration, which can benefit liquidity and index visibility but may compress differentiation.

What’s Next

All signals point to continued diversification and growth. Per FTSE Nareit, emerging property types—especially those focused on data, health, and infrastructure—are positioned for further market share gains in the coming years, driven by secular demand for AI, cloud services, aging populations, and digital connectivity. Meanwhile, retail, industrial, and residential REITs are expected to remain significant, even as their proportional weight softens. With the number of REIT listings stable but industry market cap climbing, investors should anticipate an increasingly specialized—and competitive—landscape as the sector adapts to economic, demographic, and technological shifts.