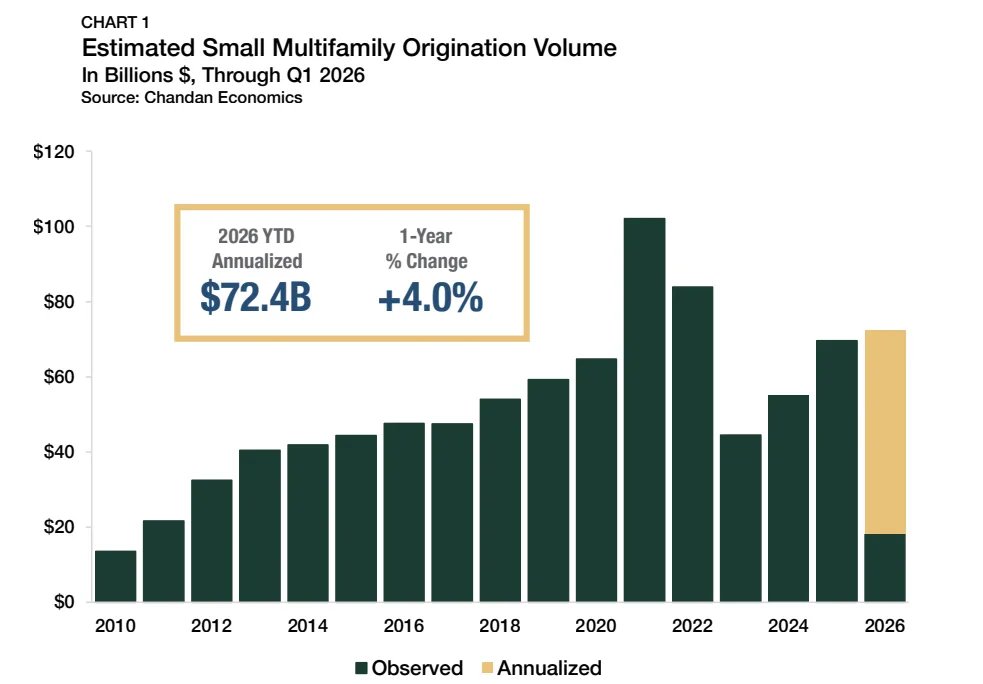

- Small multifamily originations reached an annualized $72.4B in Q1 2026, up 4% year over year, as refinancing activity continued to drive lending volume.

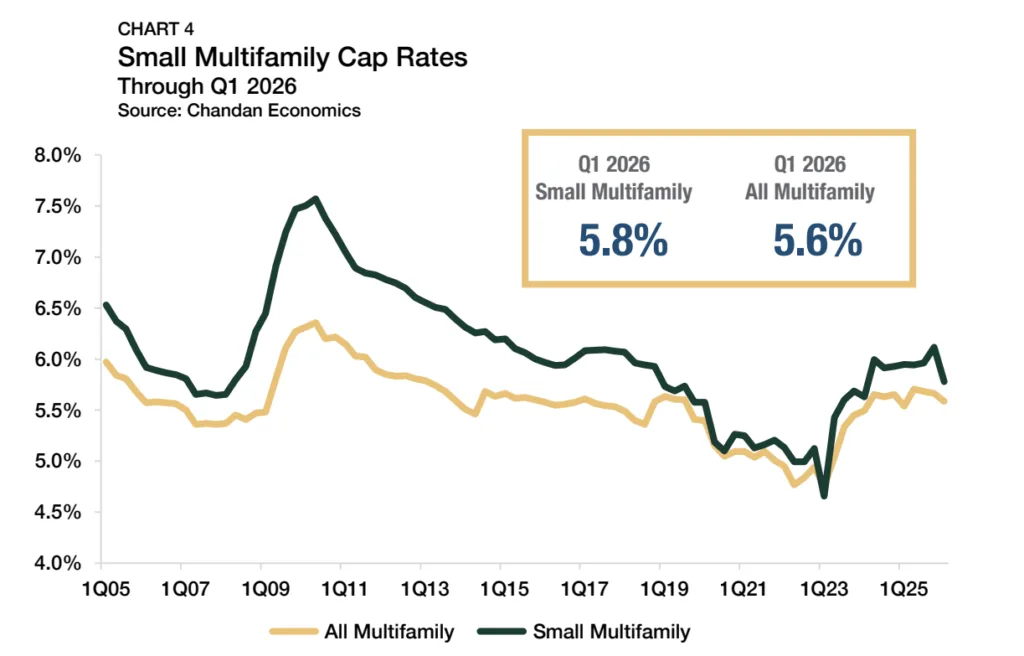

- Cap rates compressed to 5.8% while valuations rose 3.6% quarter over quarter, signaling improving pricing conditions despite higher operating expenses and softer occupancy.

- Gradually easing underwriting standards and stabilizing credit markets could support broader lending activity later in 2026, even as refinancing pressures persist.

Small multifamily investors entered 2026 with more stable financing conditions and improving valuations after a volatile end to last year. According to Arbor Realty Trust and Chandan Economics’ Q2 2026 Small Multifamily Investment Trends Report, lending activity continued to rise modestly in the first quarter while cap rates reversed course and compressed sharply.

The sector remains heavily refinancing-driven, but signs of easing credit conditions and rebounding asset values suggest the market may be moving into a more balanced phase after several quarters dominated by maturity stress and elevated borrowing costs.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Refinancing-Led Market

Refinancing accounted for 71.6% of all small multifamily originations in Q1 2026, up 302 basis points year over year, underscoring how debt maturities continue to shape activity across the sector, according to the report.

Total small multifamily originations for loans between $1M and $9M reached an annualized pace of $72.4B in the first quarter, a 4% increase over 2025’s finalized total of $69.6B. While lending volumes remain below the record-setting years of 2021 and 2022, the report noted that activity has now expanded for two consecutive years.

The Details

Property valuations improved meaningfully during the quarter. The Arbor Small Multifamily Price Index rose 3.6% quarter over quarter and 0.9% year over year as lower cap rates boosted implied values.

Small multifamily cap rates fell to 5.8% in Q1 2026 from 6.1% in the prior quarter, reaching their lowest level since early 2024. Acquisition cap rates declined to 6.0%, while refinance cap rates fell to 5.7%.

At the same time, underwriting conditions loosened modestly. Average loan-to-value ratios climbed to 64.6%, extending a recovery from 2023 lows, while debt yields declined to 8.7%, indicating lenders are becoming incrementally more comfortable with leverage.

Operating Pressures Persist

Despite improving capital market conditions, property fundamentals remained mixed. Occupancy rates for financed small multifamily properties slipped to 95.4%, down 1.4 percentage points from a year earlier.

Expense ratios also climbed sharply to 47.3%, the highest level in the current data series. The report pointed to rising insurance costs as a major driver, citing Harvard Joint Center for Housing Studies data showing multifamily insurance costs doubled between 2019 and 2024.

That combination of higher expenses and softer occupancy weighed on net operating income growth, even as rents continued to rise modestly.

Why It Matters

The latest data suggests the small multifamily sector is stabilizing after a volatile stretch. Falling cap rates and improving valuations show growing lender and investor confidence. The shift also reflects broader stabilization across multifamily markets as construction activity slows nationwide.

Small multifamily properties continue outperforming the broader rental market on occupancy. Financed properties posted 95.4% occupancy in Q1 2026. Meanwhile, the national rental average reached 92.8%, according to US Census Bureau data cited in the report.

The shift could expand transaction activity beyond refinancing and debt restructurings. Better borrowing conditions may also support more acquisitions through the rest of 2026.

What’s Next

Arbor Realty Trust and Chandan Economics expect refinancing to drive lending volume through 2026. Borrowers still face large volumes of maturing loans. However, rising valuations and looser credit standards could support more acquisitions and recapitalizations in coming quarters.

The sector’s outlook depends less on demand growth and more on stabilizing expenses and easing refinancing pressure. For now, small multifamily appears headed toward steady, slower growth instead of a sharp recovery.