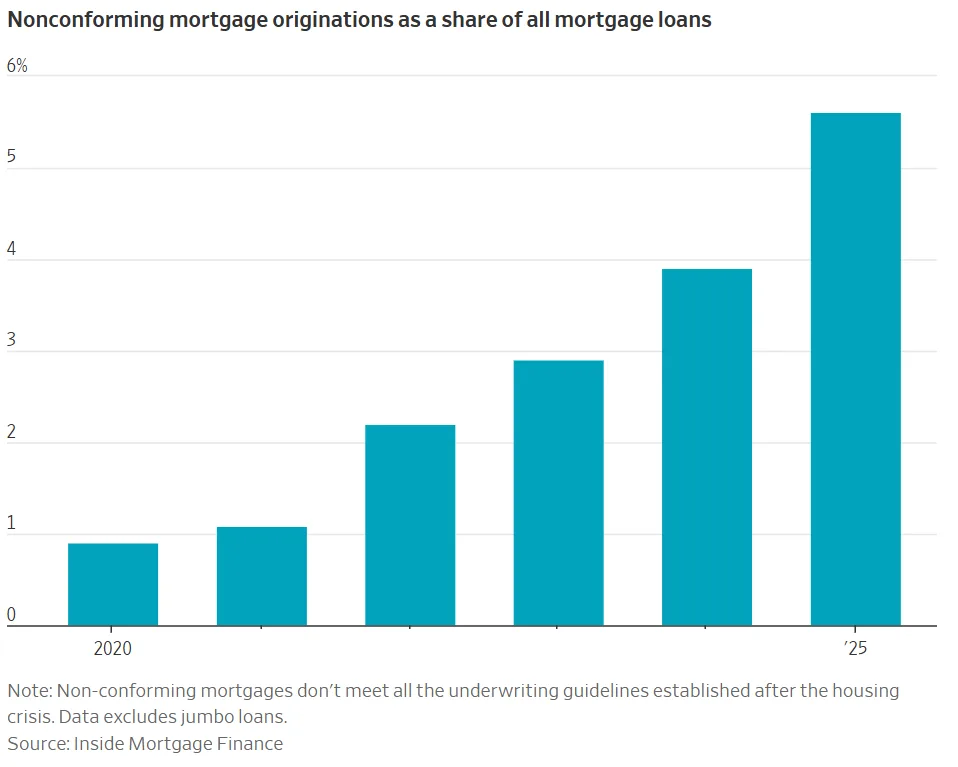

- Nonconforming mortgages accounted for nearly 6% of all home loan originations in 2025, double their share from three years ago, according to Inside Mortgage Finance.

- Lenders including Rocket Mortgage and LoanDepot are expanding alternative lending products aimed at investors, self-employed borrowers, and high-income buyers with nontraditional assets.

- Rising use of flexible underwriting could increase credit risk if housing conditions weaken, though lenders argue standards remain far tighter than pre-2008 levels.

Mortgage lenders are reviving nonconforming mortgages as traditional homebuying activity remains sluggish under elevated interest rates and affordability pressure, reports The WSJ. The products, which allow lenders to underwrite borrowers using alternative income documentation or asset-based qualifications, are gaining momentum among investors and self-employed buyers who often struggle to qualify for conventional loans.

According to Inside Mortgage Finance, nonconforming mortgages made up nearly 6% of all US mortgage originations in 2025, the highest level since the aftermath of the housing crisis and roughly double their market share from three years earlier.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Post-Crisis Product Returns

Nonconforming mortgages sit outside the underwriting standards required for loans backed by Fannie Mae, Freddie Mac, or government agencies. The category includes bank-statement loans, debt-service coverage ratio (DSCR) loans for rental investors, and asset-based lending products that evaluate wealth beyond W-2 income and tax returns.

The products largely disappeared after the 2008 housing crash triggered tighter lending standards and sweeping regulatory reforms. Before the crisis, nonconforming loans represented roughly 22% of the mortgage market in 2007, according to Inside Mortgage Finance.

Now, lenders are revisiting the segment as purchase mortgage volumes remain weak. Existing-home sales have hovered near multi-decade lows through 2025 and early 2026 as mortgage rates stayed elevated and inventory remained constrained.

The Details

Lenders say the borrower profile today differs substantially from the speculative lending seen before the financial crisis. Many applicants are high-income earners with variable income streams, small-business owners, or investors building rental portfolios.

LoanDepot reported a 68% increase in nonconforming loan production from 2024 to 2025. The company said many borrowers use the products to finance rental acquisitions, where underwriting can factor in projected rental income rather than traditional employment verification alone.

Investor demand is playing a growing role. According to Cotality data cited by The Wall Street Journal, investors accounted for roughly 30% of home purchases last year, the highest share on record. Small and midsize investors were a major contributor to the increase.

The loans also appeal to affluent borrowers whose taxable income may not fully reflect their earning power because of business deductions, commissions, or substantial real estate holdings.

Investor Lending Expands

Rental-property investors have become one of the biggest customer bases for nonconforming mortgages, particularly DSCR loans that evaluate whether rental income can cover debt payments. As institutional acquisitions slow, smaller investors have continued buying single-family rentals and vacation properties in many Sun Belt and coastal markets.

That trend aligns with broader changes in the housing market. Traditional owner-occupants continue facing affordability challenges, while investors and wealthier buyers retain greater access to capital and liquidity.

At the same time, analysts are watching loan performance closely. Fitch Ratings said delinquencies rose faster for nonconforming loans issued after 2023. The shift comes as broader commercial lending activity also rebounded in 2025, signaling renewed appetite for higher-yield debt products.

Because the loans lack government backing, lenders either retain them on balance sheet or sell them into private capital markets, exposing investors and lenders to greater credit risk if defaults rise.

Why It Matters

The resurgence of nonconforming mortgages reflects how lenders are adapting to a housing market with fewer conventional borrowers and heavier investor participation. It also highlights the growing divide between buyers with traditional salaried income and those with complex asset structures or investment portfolios.

While the sector remains far smaller than during the pre-crisis lending boom, expanding use of flexible underwriting standards could become a concern if unemployment rises or home prices soften. Moody’s Analytics Deputy Chief Economist Cristian deRitis told The Wall Street Journal that borrowers using these products are generally more vulnerable to payment stress during downturns.

For lenders, however, the products provide one of the few remaining growth channels in a market where refinancing activity remains muted and home sales volume is historically weak.

What’s Next

The trajectory of nonconforming lending will likely depend on two factors: housing-market activity and loan performance. If rates remain elevated and traditional purchase lending stays slow, lenders may continue pushing alternative mortgage products to maintain origination volume.

Regulators and ratings agencies will also be watching delinquency trends closely over the next 12 to 24 months, particularly among investor-heavy portfolios. Any meaningful deterioration in credit quality could tighten underwriting standards again, especially if private capital markets become less willing to absorb mortgage risk.