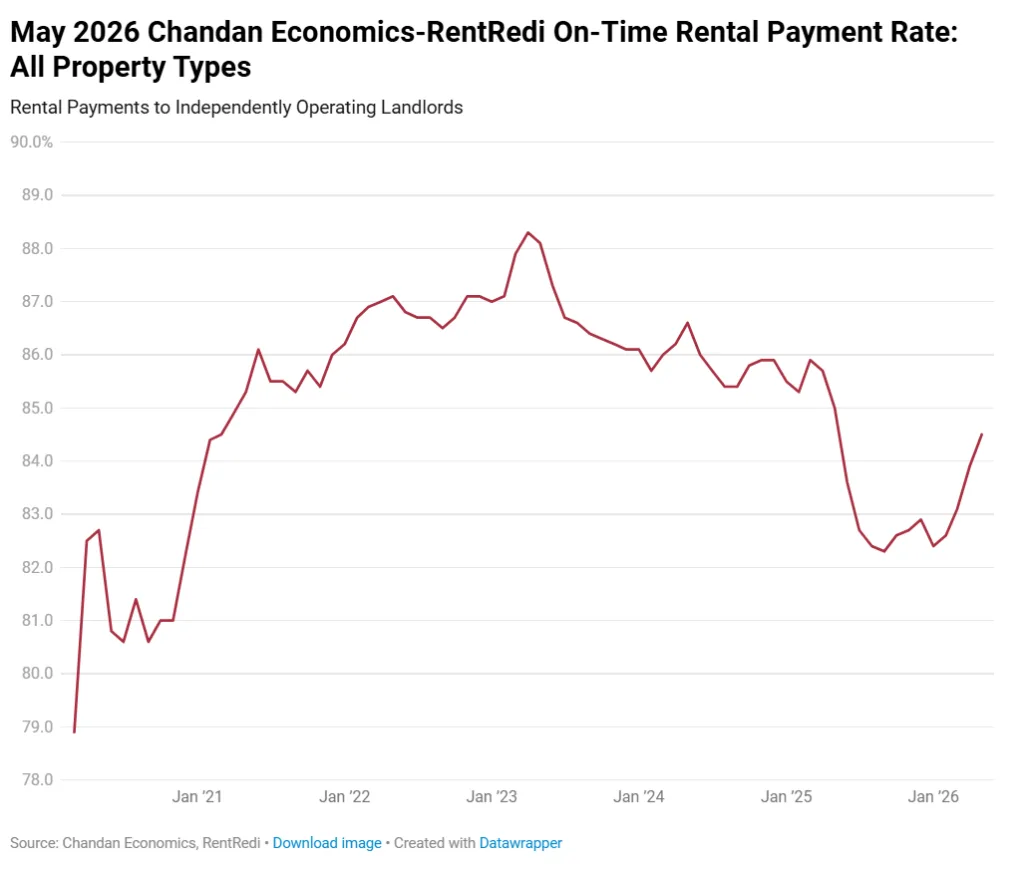

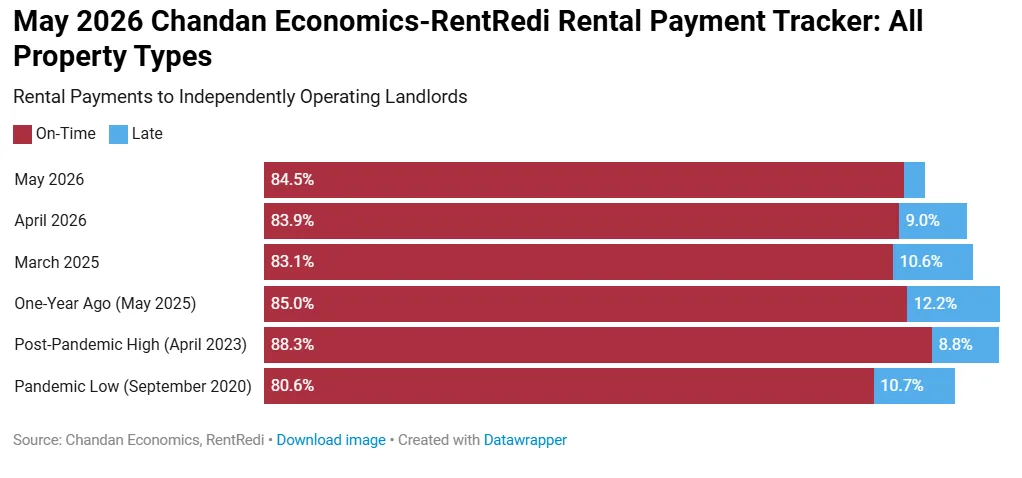

- On-time rent payments across independently operated rentals rose to 84.5% in May 2026, extending a recovery trend that began in late 2025.

- Forecast full-payment rates reached 97.1%, suggesting most missed payments are eventually being cured even as late payments remain elevated.

- Western and Mountain states continued to outperform nationally, while renter financial stress remains more visible across parts of the South and Midwest.

Independent landlords saw another month of improving rent collection performance in May, adding to signs that the sector is stabilizing after a difficult stretch in 2024 and 2025. According to Chandan Economics’ latest Independent Landlord Rental Performance Report, 84.5% of renters at non-institutional properties paid their rent on time in May 2026, up from a revised 83.9% in April.

The gains continue a broader rebound that has lifted on-time payment rates 223 basis points above the September 2025 low. Still, collections remain below prior-year levels, underscoring how uneven the recovery has been for smaller landlords navigating rising operating costs and lingering renter affordability pressure.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Slower Road Back

The latest report extends a pattern that has been building since late 2025. On-time payments have now improved in seven of the past eight months, suggesting the sector is moving beyond the sharp deterioration seen during the second half of last year.

Even so, the market has not fully recovered. Chandan Economics reported that May’s on-time payment rate remained 48 basis points below May 2025 levels, marking the 34th consecutive month of annual declines. The gap has narrowed considerably, however. Year-over-year declines exceeded 300 basis points during parts of late 2025 before moderating this spring.

Seasonality may also be helping support recent gains. Spring rent collections often benefit from tax refunds and temporary household liquidity boosts, though Chandan Economics said the current rebound appears broader than a typical seasonal bounce.

The Details

While on-time collections improved, late payments remain the biggest operational challenge for independent landlords. Forecast late-payment rates came in at 12.6% for May, only modestly below the 13.5% peak recorded in January and February 2026.

That distinction matters for small landlords, many of whom rely on rental income to cover mortgages, insurance, maintenance, and taxes without the balance-sheet flexibility available to institutional owners. A tenant paying weeks late can still create meaningful cash-flow strain even if the rent is eventually collected.

At the same time, overall payment resolution continues to improve. Chandan Economics forecast a 97.1% full-payment rate for May — the strongest projected reading since May 2025. Observed full-payment rates through the first two months of 2026 averaged 96.3%, slightly ahead of the 2025 annual average of 96.0%. That builds on the stabilization trend that first began emerging in late 2025 as collection declines started narrowing and payment activity gradually rebounded across smaller rental operators.

The report drew data from 63,038 rental units managed through RentRedi’s property management platform.

Smaller Rentals Still Outperform

Performance varied meaningfully by property type. Smaller properties continued to outperform larger multifamily assets in May, reinforcing a trend that has persisted throughout much of the recovery cycle.

Two-to-four-family properties posted the strongest on-time payment rate at 85.4%, followed by single-family rentals at 84.6%. Multifamily properties lagged at 83.3%.

Regional performance also remained highly uneven. Western and Mountain states dominated the top rankings, with Alaska (93.5%), Hawaii (93.4%), New Hampshire (93.1%), Washington, DC (92.7%), and Colorado (92.6%) posting the nation’s strongest on-time payment rates.

At the other end of the spectrum, Mississippi recorded the weakest performance at 66.3%, followed by Michigan (77.4%), West Virginia (78.3%), Illinois (79.7%), and Maryland (79.9%).

According to Chandan Economics, those disparities likely reflect differences in local labor markets, renter income profiles, and regional cost burdens.

Why It Matters

The report offers one of the clearest looks into the financial health of renters and small landlords outside the institutional apartment sector. Unlike large multifamily REITs and institutional operators, independent landlords often have less access to capital and fewer operational buffers when rent payments arrive late.

The latest data suggest renter finances are improving incrementally, but not enough to fully normalize collection patterns. Chandan Economics warned that broader macroeconomic pressures — including rising energy prices and renewed inflation concerns — could slow further improvement if household budgets tighten again later this year.

That risk is especially important for workforce housing operators and small-scale investors concentrated in lower-income renter markets, where payment volatility tends to hit first.

What’s Next

The key question heading into the second half of 2026 is whether late-payment rates finally begin to decline more meaningfully. Chandan Economics noted that sustained improvement in on-time collections will likely require a sharper reduction in late payments, not just stronger eventual payment resolution.

Investors and operators will also be watching whether inflationary pressures and weakening consumer credit conditions begin spilling further into rental performance data during the summer and fall leasing seasons.

For now, the direction of travel remains positive. But for independent landlords, the recovery still looks more like stabilization than a full return to normal.