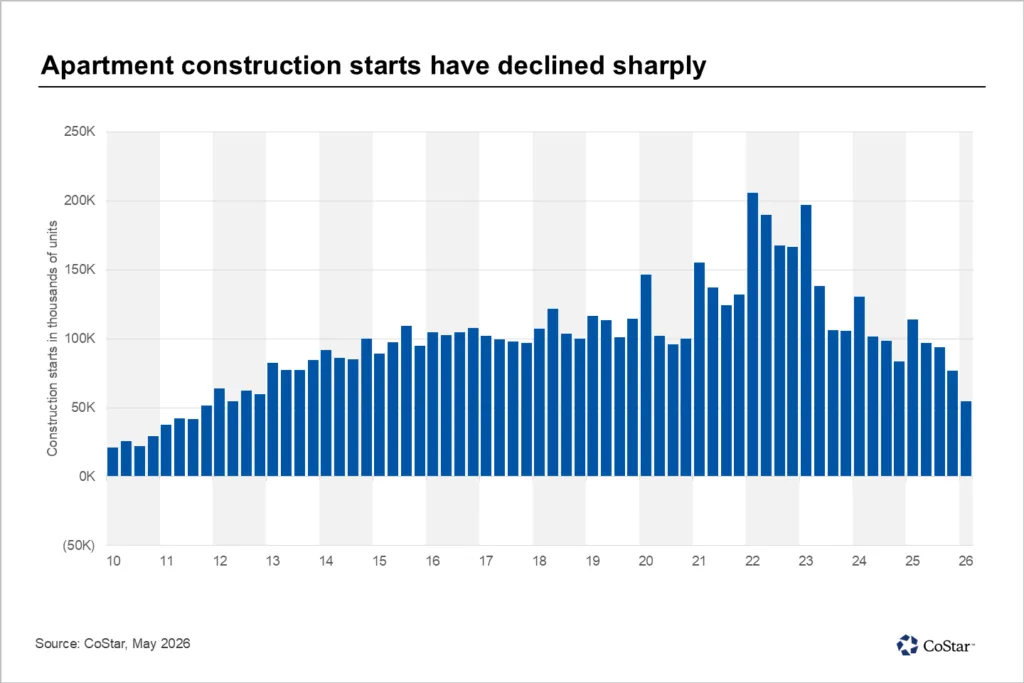

- US apartment construction starts fell to roughly 55,000 units in Q1 2026, marking the lowest quarterly level since 2011, according to CoStar and Apartments.com.

- The national multifamily pipeline shrank to about 579,000 units under construction, down more than 50% from its 2023 peak as developers pull back on new projects.

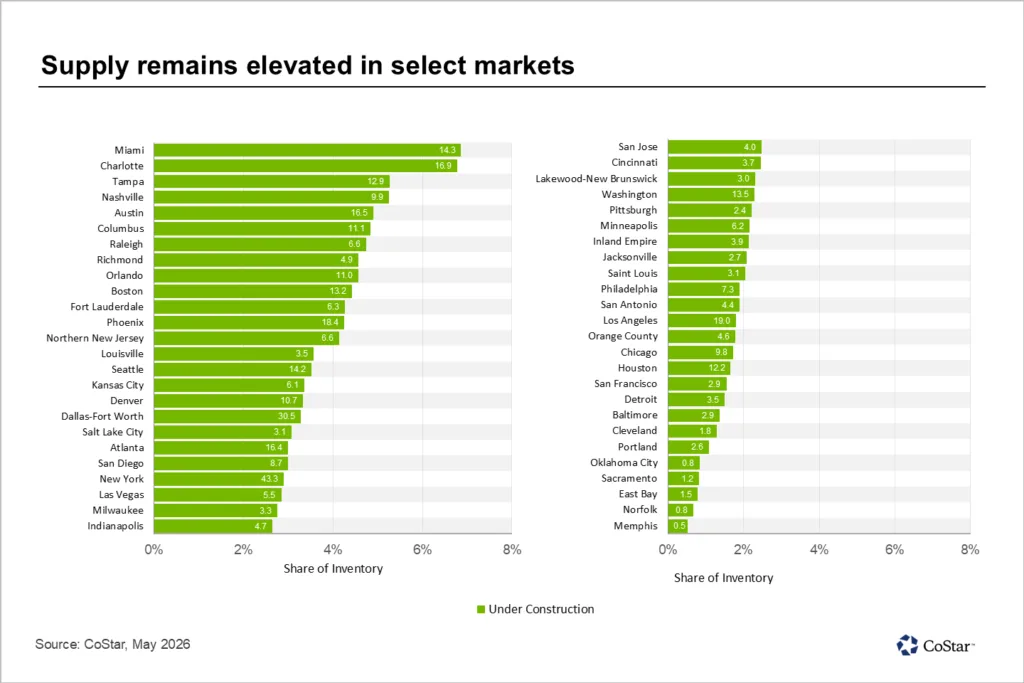

- Markets in the South and Mountain regions still face elevated supply pressure, but the shrinking pipeline could help rebalance apartment fundamentals over the next several years.

BusinessWire reports that apartment developers are continuing to hit the brakes as financing costs, slower rent growth, and elevated construction expenses weigh on new project feasibility. According to a Q1 2026 multifamily construction update from Apartments.com and CoStar, US apartment construction starts fell to approximately 55,000 units nationwide during the quarter, the lowest quarterly level since 2011.

The sharp slowdown marks a 73% decline from the sector’s peak construction activity in early 2022. At the same time, the national apartment construction pipeline has contracted significantly as fewer projects move forward.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Dramatic Multifamily Reset

The multifamily sector spent the past several years working through one of the largest apartment supply waves in decades. Developers aggressively launched projects during the post-pandemic rent boom, supported by strong occupancy, rapid rent growth, and relatively accessible financing conditions.

That environment shifted quickly beginning in 2023 as interest rates climbed and rent growth softened across many Sun Belt markets. Higher insurance, labor, and material costs also pushed development budgets higher, making many ground-up projects financially unworkable.

“Developers have pulled back sharply as weaker rent growth and higher financing costs weigh on project feasibility,” Grant Montgomery, national director of US multifamily analytics at CoStar Group, said in the report.

The Construction Pipeline Keeps Shrinking

The number of apartment units under construction nationwide declined to roughly 579,000 units in Q1 2026, down more than 50% from its peak in early 2023, according to CoStar. Current pipeline levels are now broadly aligned with the mid-2010s development cycle.

While new starts continue to fall, deliveries remain relatively elevated because projects financed earlier in the cycle are still coming online. CoStar reported that annual apartment deliveries peaked in 2024 and have declined approximately 26% over the past four quarters.

Regional supply pressures remain uneven. The Mountain region currently has the highest construction exposure relative to inventory, with roughly 3.3% of apartment stock under construction. The South follows closely at 3.2%.

At the metro level, New York City maintains the nation’s largest absolute multifamily pipeline, followed by Dallas-Fort Worth. Miami and Charlotte lead the country in construction concentration relative to existing inventory, with more than 6% of apartment stock under construction in both markets.

Sun Belt Supply Pressures Remain Elevated

Several high-growth Sun Belt markets are still absorbing an outsized wave of new supply that broke ground during the peak development years of 2021 and 2022. Markets including Austin, Nashville, Charlotte, and Miami have experienced softer rent growth and rising concessions as deliveries outpaced near-term demand growth. That slowdown aligns with broader industry forecasts calling for weaker apartment rent gains throughout 2026 as elevated supply continues pressuring fundamentals in several major metros.

According to CoStar’s Q1 2026 analysis, developers in many of these markets have sharply reduced new starts in response to weakening fundamentals. The pullback suggests supply-demand conditions could begin stabilizing over the next few years as fewer projects enter the pipeline.

Gateway markets, meanwhile, continue to attract large-scale development activity despite higher barriers to entry. New York City’s leading pipeline position reflects both persistent housing demand and the long timelines associated with urban multifamily development.

Why It Matters

The construction slowdown represents a major shift for the multifamily sector after years of record supply growth. For owners and investors, the shrinking pipeline could eventually support stronger rent growth and occupancy once the current delivery wave clears.

The slowdown also reflects broader capital market challenges across commercial real estate. Elevated interest rates and tighter lending standards continue to limit development activity across most property types, particularly projects requiring significant construction financing.

For renters, the near-term impact will vary by market. Supply-heavy metros may continue seeing concessions and slower rent increases through 2026, while markets with limited new development could tighten more quickly once deliveries taper off.

What’s Next

Multifamily developers are expected to remain cautious through the rest of 2026 unless financing conditions improve materially. Most industry forecasts point to continued declines in starts before activity stabilizes closer to long-term historical averages.

As the current supply wave gets absorbed, market fundamentals could improve heading into 2027 and beyond, particularly in high-demand metros where new development has slowed sharply. Investors will be watching leasing trends, concession levels, and capital markets closely for signs that the next apartment development cycle is beginning.