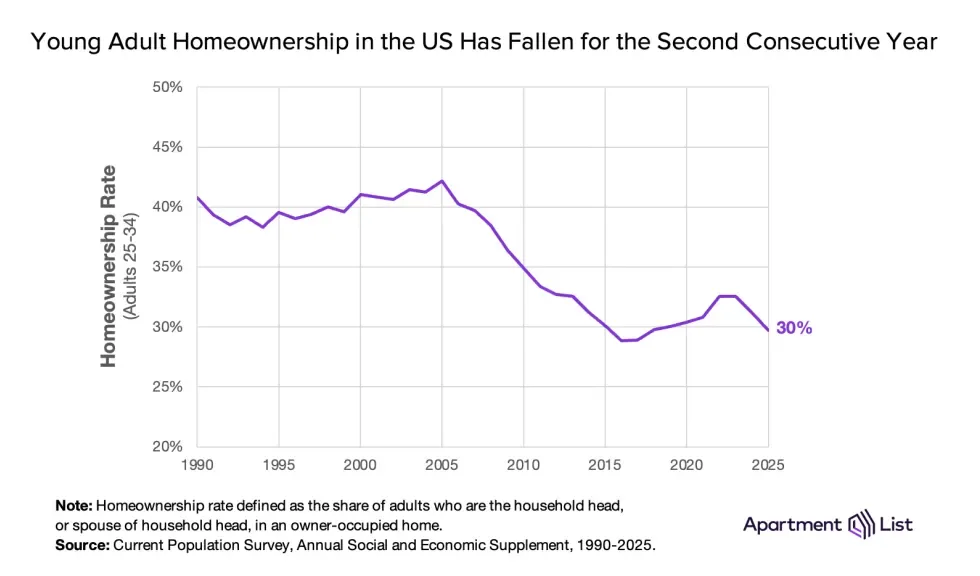

- Young adult homeownership dropped to 30% nationwide, with adults ages 25–34 seeing the steepest decline of any age group over the past two years.

- Rising mortgage costs, insurance premiums, and rents have left many young adults priced out of both buying and renting, pushing millions to live with parents or other family members.

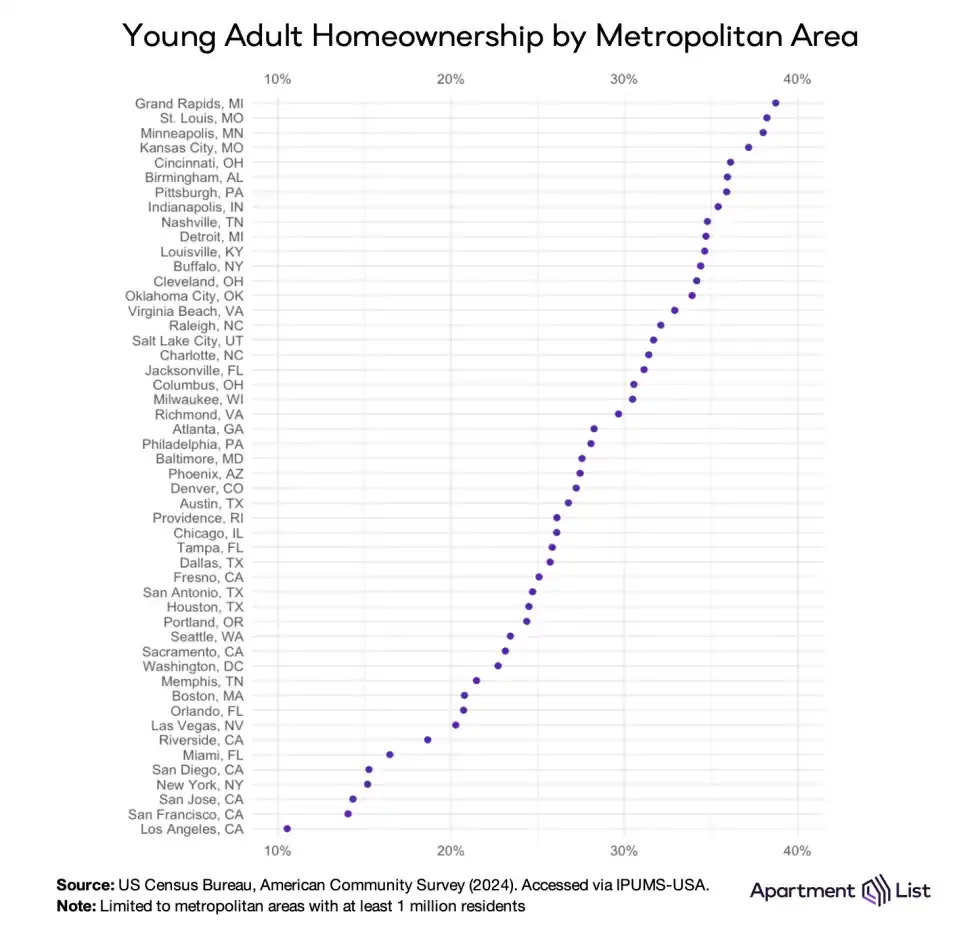

- Expensive coastal metros like Los Angeles, San Francisco, and Miami continue to post the lowest young adult homeownership rates, while Midwest and Southern markets remain comparatively accessible.

Young adults are increasingly caught in a housing gray zone: unable to afford homeownership, but also struggling with rising rents. A new analysis from Apartment List found the homeownership rate for Americans ages 25 to 34 has fallen to just 30%, erasing much of the progress made between 2017 and 2022.

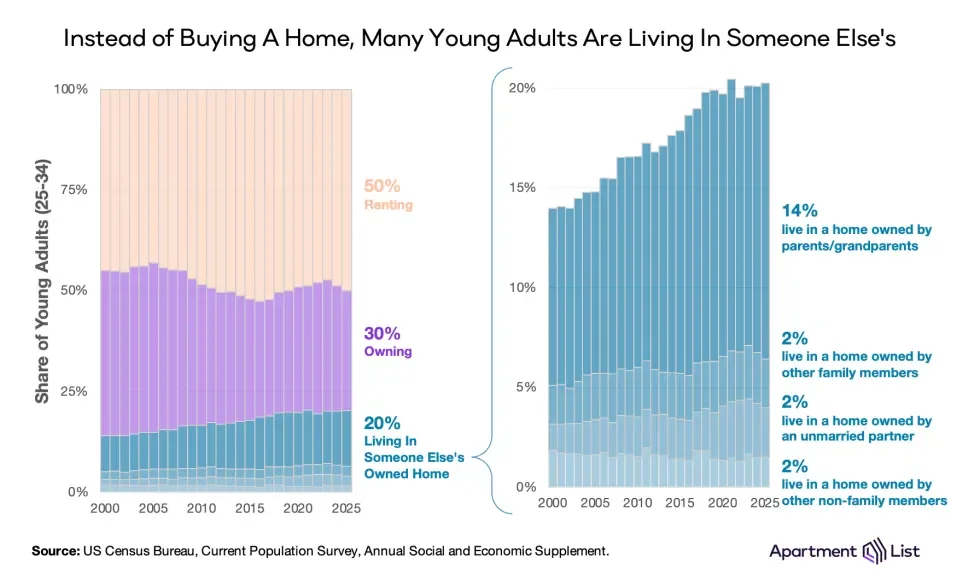

The affordability squeeze has accelerated since 2023 as elevated home prices, higher mortgage rates, and rising ownership costs widened the gap between renting and buying. According to Apartment List’s May 2026 analysis, roughly 9M young adults now live in someone else’s owned home instead of renting or owning themselves.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Affordability Crunch Deepens

The housing market has thrown several financial obstacles at first-time buyers over the past five years. Home prices surged during the pandemic-era buying frenzy in 2020 and 2021, while mortgage rates climbed rapidly beginning in 2022. Even as home price growth cooled, monthly ownership costs continued rising because of higher borrowing costs, insurance premiums, utilities, and property taxes.

Apartment List found the nationwide homeownership rate declined nearly a full percentage point between 2023 and 2025. For adults ages 25 to 34, however, the decline was much steeper at 2.9 percentage points—more than triple the national drop. The report noted that older age groups experienced far smaller declines during the same period.

The data suggests affordability challenges are disproportionately affecting first-time buyers at a stage traditionally associated with household formation, marriage, and family growth. The current 30% ownership rate among young adults is now approaching the post-Great Financial Crisis low recorded in 2017.

The Details

The economics increasingly favor renting—at least comparatively. Apartment List reported that monthly housing costs for new homeowners are now more than $1,000 higher than for renters on average nationwide. In some markets, homeowners spend more than twice as much on housing each month compared to renters.

But renting is hardly cheap either. Inflation-adjusted median rents for recent movers have climbed 30% since 2010, according to the report. As a result, many younger Americans are delaying both renting independently and purchasing homes altogether.

Today, 20% of adults ages 25 to 34 live in someone else’s owned home, up from 14% in 2000. Apartment List estimates that 6.3M young adults currently live with parents or grandparents, an all-time high. Another roughly 3M live in homes owned by other relatives, friends, or unmarried partners.

Interestingly, the number briefly declined during the pandemic homebuying boom, suggesting some young adults used temporary living arrangements to save for down payments before affordability conditions deteriorated again.

California Remains the Toughest Market

The nation’s most expensive housing markets continue to post the weakest young adult ownership rates. Los Angeles ranked last among major metros, with just over 10% of adults ages 25 to 34 owning homes.

Other California metros also posted low ownership rates, including San Francisco and San Jose at 14%, San Diego at 15%, Riverside at 19%, and Sacramento at 23%. High-cost coastal markets such as New York, Miami, Boston, Washington, DC, and Seattle also ranked near the bottom.

Meanwhile, more affordable Midwest and Southern metros continue outperforming the national average. Grand Rapids posted the highest young adult homeownership rate at 39%, followed by St. Louis and Minneapolis at 38%, Kansas City at 37%, and Cincinnati, Birmingham, and Pittsburgh at 36%.

The geographic divide underscores how local affordability conditions increasingly shape household formation patterns and migration trends. Lower-cost metros appear to offer younger adults greater flexibility to choose between renting and buying rather than delaying both options.

Why It Matters

The decline in young adult homeownership carries broader implications for the housing market, multifamily demand, and long-term wealth creation. Homeownership has historically served as the primary wealth-building mechanism for middle-income households, particularly younger families entering the market early.

For multifamily owners, sustained affordability pressure has helped support renter demand even amid elevated apartment supply. The rental market has absorbed a historic wave of new deliveries partly because many would-be first-time buyers remain sidelined.

At the same time, the rise in multigenerational living reflects mounting pressure on household budgets. According to Apartment List, millions of young adults are effectively postponing independent household formation altogether because neither renting nor ownership feels financially attainable. That shift is also reshaping rental demand patterns as more young adults delay moving into apartments of their own and remain in shared or family housing longer.

That trend could have downstream effects on consumer spending, housing turnover, and demographic growth patterns in expensive metros already grappling with affordability concerns.

What’s Next

There are early signs the for-sale housing market may slowly improve for buyers, though affordability remains far from healthy. Apartment List cited the Case-Shiller Home Price Index, which showed national home price growth slowing from 6% in 2024 to roughly 1% today.

Several high-construction markets—including Dallas, Phoenix, and Denver—have already posted year-over-year home price declines of roughly 2%. Active listings are also gradually increasing, potentially giving buyers more negotiating power.

Still, softer price growth alone is unlikely to close the affordability gap quickly. Mortgage rates remain elevated, ownership costs continue rising, and labor market uncertainty has limited wage growth for many workers outside top income brackets.

For young adults hoping to transition from renters—or from their parents’ homes—into ownership, the path remains challenging. Without meaningful affordability improvements, the share of Americans stuck between renting and owning may continue climbing.