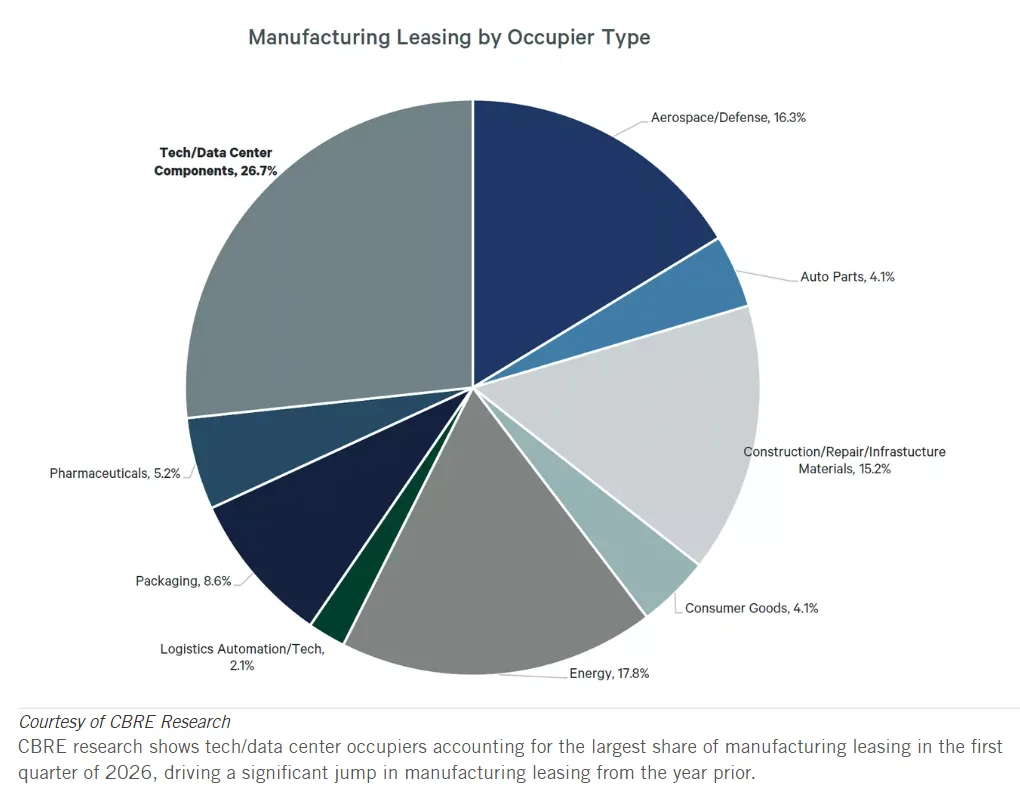

- Data center suppliers accounted for 27% of US manufacturing leasing activity in Q1 2026, according to CBRE, making the sector the largest driver of industrial demand growth.

- Manufacturers producing switchgear, cooling systems, semiconductors, and prefab components are expanding facilities across markets including Texas, Nebraska, Tennessee, and Minnesota.

- Industrial landlords and logistics operators increasingly view digital infrastructure as a long-term demand engine rather than a short-term construction cycle tied only to AI hype.

According to Bisnow, the AI infrastructure race is no longer just reshaping data center development. It is rapidly becoming one of the biggest growth drivers in US industrial real estate.

As hyperscale operators and tech firms race to build digital infrastructure, the ripple effects are spreading through manufacturing plants, warehouse networks, and prefab construction hubs designed to support the data center supply chain. CBRE’s Q1 2026 industrial data suggests the shift is already materially influencing leasing activity nationwide.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

AI Infrastructure Expands Beyond Server Farms

Nvidia’s announcement last week that it will partner with Corning to develop three manufacturing facilities in North Carolina and Texas underscored how deeply AI investment is reaching into industrial sectors. The facilities will produce optical connectivity equipment used in data centers, reinforcing domestic supply chains tied to digital infrastructure.

Nvidia CEO Jensen Huang framed the initiative as an opportunity to “reinvigorate American manufacturing and supply chains,” while Corning CEO Wendell Weeks called AI “a manufacturing story” happening in the US.

The announcement adds to a growing pipeline of industrial projects linked directly to data center demand. Siemens opened a $190M manufacturing hub in Fort Worth in 2025 to produce electrical equipment for data centers, while Eaton began construction this year on a $30M Nebraska switchgear plant. Cooling-system manufacturers nVent and Aaon also launched new facilities in Minnesota and Tennessee over the past six months.

At the high end of the supply chain, semiconductor fabrication projects continue to reshape industrial investment patterns. Elon Musk said this month he is evaluating a site near College Station, Texas, for a proposed “Terafab” chipmaking campus that could become the largest private business investment in Texas history. Semiconductor fabs from companies including Intel and TSMC already rank among the most expensive industrial projects globally, often carrying price tags approaching $100B.

The Numbers Behind Manufacturing Leasing Growth

According to CBRE’s Q1 2026 industrial research, manufacturing leasing activity increased 28% year over year in the first quarter. After reviewing leasing trends tenant by tenant, CBRE found companies tied to the data center and technology supply chain represented the largest share of manufacturing occupiers, accounting for 27% of signed deals.

CBRE Global Head of Industrial Research James Breeze said the findings confirmed that data center growth is now materially influencing industrial absorption trends.

Importantly, much of the demand is not tied solely to one-time construction activity. Instead, industrial occupiers are increasingly producing servers, cooling systems, switchgear, and replacement IT equipment that require continuous upgrades throughout a data center’s operating lifecycle.

That distinction matters for landlords and developers. Long-term replacement cycles create more stable industrial demand than temporary construction booms, particularly as hyperscale operators expand AI computing capacity nationwide.

The logistics side of the market is seeing similar momentum. Prologis said during its April earnings call that data center suppliers now account for 10% of new industrial leases, up from 5% a year earlier. The company described digital infrastructure as a “new structural driver” of logistics demand.

New entrants are also emerging to target the niche directly. Logistics real estate firm The Blev Group launched this month with a strategy focused on acquiring last-mile warehouses and outdoor storage properties positioned near expanding data center corridors.

Prefab Manufacturing Reshapes Logistics Real Estate

Another major trend boosting industrial demand is the rise of prefabricated data center construction.

Instead of assembling every component onsite, contractors increasingly build electrical skids, cooling systems, and structural modules at regional prefab facilities before shipping them to hyperscale campuses for installation. The process shortens delivery timelines and helps developers cope with labor shortages and supply chain delays.

DPR Construction alone has developed more than 1.5M SF of prefab facilities nationwide, according to the company. Some operate in leased warehouse space, while others are purpose-built industrial properties.

The model is also blurring the lines between logistics and manufacturing real estate. Facilities often combine assembly operations with warehousing and distribution functions under one roof.

DPR is currently producing modular systems for Oracle and OpenAI’s Stargate campus in West Texas and Meta’s Hyperion megacampus in Louisiana from a 330K SF Houston facility. The company describes the strategy as a “hub-and-spoke” model, selecting industrial sites based on transportation access, labor availability, and trucking efficiency rather than proximity to the data center itself.

That flexibility is broadening the geographic reach of data center-related industrial demand.

New Industrial Winners Emerge

While major hyperscale markets continue to benefit, secondary industrial cities are increasingly capturing spillover demand.

According to Avison Young, Columbus, Ohio recorded 13M SF of net industrial absorption in 2025, trailing only Dallas and Phoenix. The firm attributed much of that growth to data center expansion and semiconductor manufacturing activity in the region. The momentum mirrors broader demand shifts reshaping emerging industrial hubs as occupiers expand beyond traditional gateway markets in search of power, land, and supply chain capacity.

Silicon Valley also ranked as the third-largest manufacturing leasing market last year, per CBRE, driven partly by the concentration of AI research and development activity nearby.

At the same time, industrial projects tied to the digital infrastructure supply chain are appearing in markets not traditionally associated with hyperscale development, including Nebraska, Minnesota, and Tennessee. That dispersion suggests the economic footprint of AI infrastructure extends far beyond the handful of metros hosting large server campuses.

Why It Matters

Industrial real estate spent much of the past two years navigating slower warehouse leasing and normalization after the pandemic-era logistics boom. Data center infrastructure is now emerging as a meaningful new demand driver across manufacturing, warehousing, and distribution assets.

The trend also reflects how AI investment is reshaping physical infrastructure, not just digital systems. As cloud operators, chipmakers, and contractors scale up, they are creating an industrial ecosystem that supports everything from semiconductors to cooling equipment and prefab assembly.

For landlords, that creates a potentially durable source of demand tied to long-term computing growth rather than cyclical consumer spending patterns.

What’s Next

The next phase of growth will likely center on regional supply-chain hubs supporting hyperscale campuses under development across Texas, Louisiana, Ohio, and other emerging AI corridors.

Developers and industrial investors will also be watching whether semiconductor manufacturing and prefab construction continue scaling nationally. If AI-related infrastructure spending remains elevated through 2026 and beyond, data center supply chains could become one of industrial real estate’s most important leasing catalysts for the rest of the decade.