- Upper Midwest apartment markets posted steady rent growth and strong occupancy in Q1 2026, benefiting from manageable new supply and resilient renter demand.

- Chicago emerged as the region’s standout performer, while Minneapolis-St. Paul and Milwaukee improved as construction pipelines moderated.

- The region’s lower-volatility profile is increasingly attractive to multifamily investors navigating uneven national apartment fundamentals.

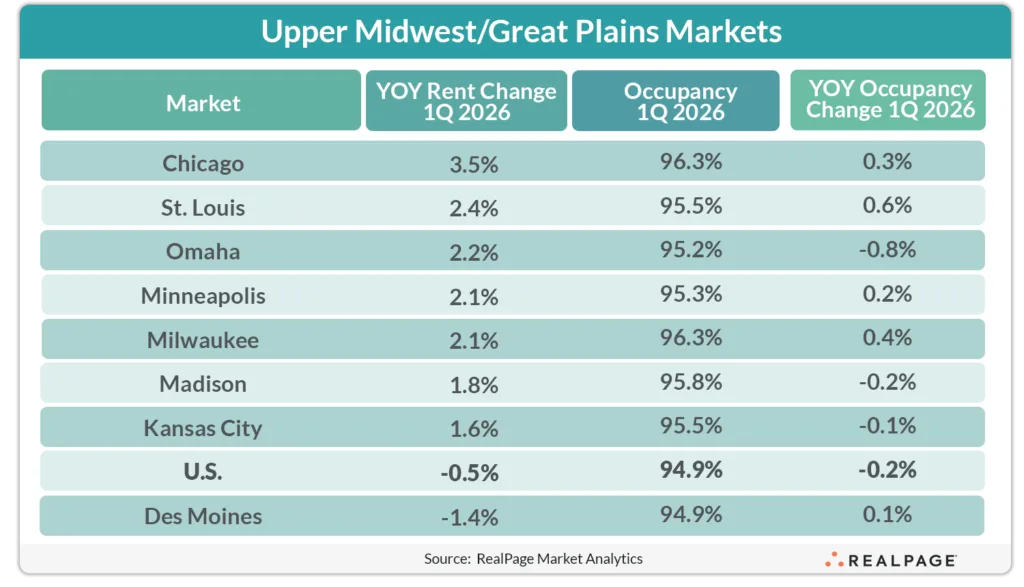

Most apartment investors chasing growth headlines tend to overlook the Upper Midwest and Great Plains. But in Q1 2026, those markets quietly delivered some of the country’s healthiest multifamily fundamentals, according to RealPage Analytics. Across the region, slower supply growth and stable renter demand helped keep occupancy tight and rents moving upward despite broader economic uncertainty.

Chicago led the pack, while Milwaukee, Minneapolis-St. Paul, and Kansas City also posted solid performance. Even smaller metros like Omaha, Des Moines, and St. Louis showed resilience, though each faced localized labor and supply pressures.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Chicago’s Urban Core Rebounds

Chicago emerged as one of the strongest-performing apartment markets in the country during the year-ending first quarter, per RealPage Analytics. The city benefited from a sharp pullback in new deliveries alongside strong renter retention and renewed demand in urban neighborhoods. Those dynamics helped tighten occupancy and support rent growth even as national apartment markets remained uneven.

The recovery is notable given Chicago’s muted multifamily performance earlier in the post-pandemic cycle. Urban Class A properties, which struggled with elevated vacancy in 2021 and 2022, have regained traction as renters return to centrally located housing near transit and employment hubs.

The Details

Milwaukee and Minneapolis-St. Paul also gained momentum as construction starts slowed and previously elevated supply pipelines began normalizing. RealPage noted that improving occupancy trends offset relatively modest job growth in both metros.

Kansas City continued to reinforce its reputation as one of the country’s steadiest multifamily markets. The metro avoided the extreme rent swings seen in high-growth Sun Belt cities, maintaining consistent occupancy and measured rent gains. Meanwhile, Omaha, Des Moines, and St. Louis posted more mixed results as labor market softness and supply timing created pockets of pressure.

The broader region benefited from one key advantage: manageable inventory growth. Unlike Sun Belt metros that absorbed record deliveries over the past two years, Upper Midwest apartment markets generally maintained more disciplined construction pipelines.

A Lower-Volatility Investment Play

The performance shift comes as multifamily investors increasingly prioritize stable cash flow over aggressive growth projections. According to CBRE’s 2026 multifamily outlook, investors have shown renewed interest in Midwest markets with durable occupancy and less exposure to oversupply risk.

That dynamic is helping reposition Midwest apartment rents as a defensive investment story rather than a high-growth one. Investor demand has also strengthened as capital rotates away from volatile coastal luxury markets toward steadier multifamily fundamentals in the Midwest. While rent gains in the region remain moderate compared to coastal or Sun Belt boom markets, operators are benefiting from steadier expense growth, stronger retention, and fewer concessions.

Chicago’s rebound is especially important because institutional capital has historically approached the market cautiously due to taxes, governance concerns, and slower population growth. Sustained apartment demand could help narrow that perception gap if fundamentals continue improving through 2026.

Why It Matters

The Upper Midwest’s performance underscores how supply discipline has become one of multifamily’s biggest competitive advantages. Markets that avoided excessive post-pandemic construction are now seeing tighter occupancy and healthier pricing power as national apartment absorption stabilizes.

For investors, the region offers a counterweight to high-volatility Sun Belt markets still digesting elevated deliveries. According to RealPage Analytics, many Midwest metros entered 2026 with occupancy levels and rent trends outperforming broader national averages despite slower economic growth.

What’s Next

The biggest question for Upper Midwest apartment markets centers on demand durability if job growth slows in late 2026. So far, fewer deliveries have supported fundamentals. However, weaker labor markets in smaller metros could reduce absorption if hiring declines.

Still, the near-term supply pipeline looks favorable. Multifamily starts continue slowing nationwide, which limits future competition. As a result, Midwest operators could benefit from constrained supply through 2027. That setup may support another year of stable apartment performance across the region.