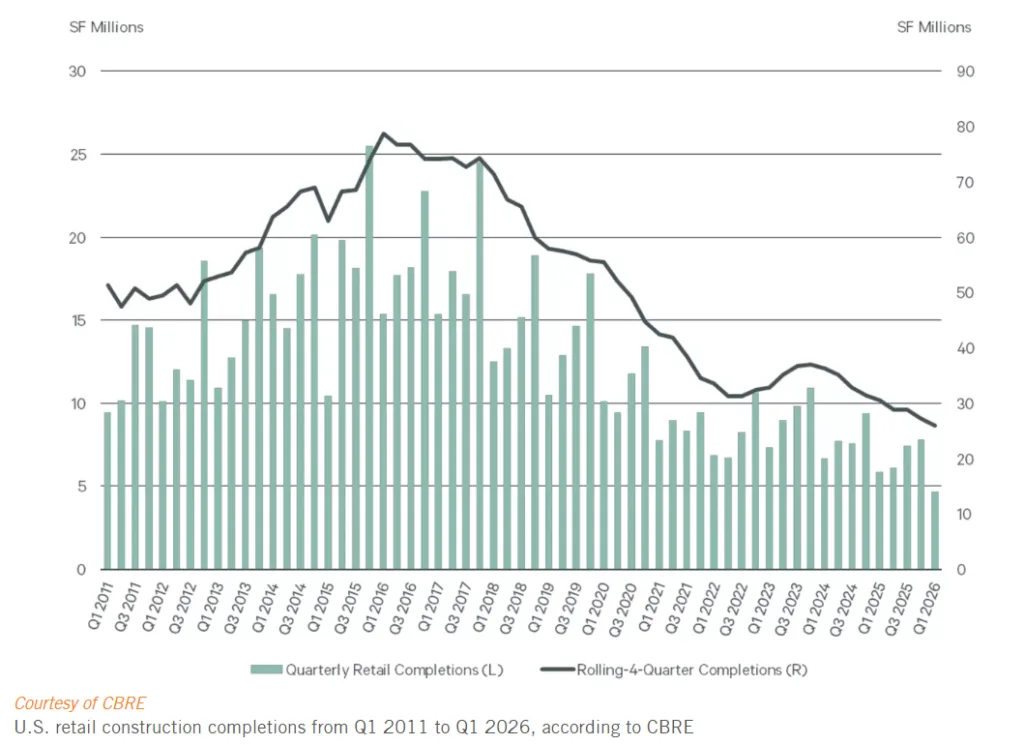

- US retail construction completions fell to 4.7M SF in Q1 2026, marking the lowest quarterly delivery volume in two decades, according to CBRE.

- High construction costs and labor shortages continue to limit new retail development, while bankruptcies from major retailers added available space back into the market.

- Institutional investors are increasing allocations to retail assets as tight supply and stable fundamentals make the sector more attractive relative to other property types.

According to Bisnow, US retail construction completions fell to their lowest level in at least 20 years during Q1 2026, underscoring how little new supply is entering the market even as investor appetite for retail assets accelerates. CBRE reported just 4.7M SF of retail deliveries nationwide last quarter, down sharply from the sector’s modern peak of more than 25M SF in Q4 2015.

The slowdown reflects a retail market still grappling with elevated development costs and a constrained labor pool, even as fundamentals remain relatively stable. At the same time, institutional capital continues flowing into the sector, drawn by limited supply and resilient tenant demand.

Why Retail Construction Keeps Shrinking

CBRE attributed the historic decline in retail construction completions to persistently high building costs and ongoing labor shortages across the construction industry. Those pressures have made ground-up retail development increasingly difficult to pencil, particularly outside high-growth Sun Belt markets.

Despite the lack of new inventory, the national retail availability rate still rose 10 basis points quarter-over-quarter to 4.9% in Q1 2026. The increase came as a wave of retailer bankruptcies and store closures returned space to the market faster than tenants absorbed it.

The Details

The US retail sector posted 1.7M SF of positive net absorption during Q1, according to CBRE’s latest national retail report. Neighborhood, community, and strip centers led performance with 641K SF of absorption, excluding freestanding retail assets.

Power centers were the only retail segment to record negative absorption. CBRE linked the weakness to continued distress among big-box retailers, including Saks Global and Eddie Bauer.

Saks Global filed for bankruptcy in January 2026 and announced plans to close 62 stores. Eddie Bauer followed in February with plans to shutter roughly 150 locations, marking the company’s third bankruptcy filing since 2003.

Retail development activity remained concentrated in the Sun Belt. Phoenix led all US markets with 744K SF of retail deliveries in Q1, followed by Dallas, San Antonio, Houston, and Bakersfield, California.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Institutional Investors Pile Into Retail

Even with store closures weighing on absorption, institutional investors have become increasingly bullish on retail real estate. According to Newmark, nationwide retail sales volume reached $66.8B in 2025, up 35% year-over-year as larger investors targeted stabilized retail properties.

Apollo Global Management announced in March that it would invest $1B for a 49% stake in a joint venture with Realty Income focused on single-tenant net lease retail assets. During the same month, Nuveen raised $330M for its US Cities Retail Fund targeting grocery-anchored retail centers in affluent markets.

Investor demand has broadened beyond necessity retail into multiple formats as buyers search for stable cash flow and sectors with limited new competition.

Why It Matters

Retail’s supply pipeline has effectively stalled at a time when many other CRE sectors continue dealing with oversupply concerns. That dynamic is helping support occupancy and rent growth for existing retail assets, particularly grocery-anchored centers and well-located neighborhood retail. The slowdown also mirrors broader construction pullbacks across commercial real estate, where developers are scaling back new projects amid elevated financing and labor costs.

The combination of low new supply and renewed institutional demand is reshaping retail’s investment profile. After years of skepticism tied to e-commerce disruption, many investors now view retail as a relative safe haven compared to office and certain multifamily markets.

“Retail is on fire,” Newmark President of Capital Markets Chad Lavender said during Bisnow’s First Draft Live event on May 2.

What’s Next

Retail construction activity is unlikely to rebound meaningfully in the near term unless financing conditions improve and development costs moderate. With construction pipelines still thin across most markets, landlords could gain additional pricing power if tenant demand remains steady through 2026.

Investors will also be watching whether retailer bankruptcies continue accelerating. Additional closures could push availability rates higher even as constrained development keeps overall supply growth muted.