- US apartment occupancy climbed to 95.2% in April 2026, marking four straight months of improvement after bottoming out at the end of 2025.

- Sun Belt markets including Austin, Denver, Phoenix, and Charlotte continued to post steep annual rent cuts as new supply outpaced absorption.

- Coastal tech hubs such as San Francisco and San Jose led national rent growth, signaling a widening divide between supply-heavy Sun Belt metros and constrained coastal markets.

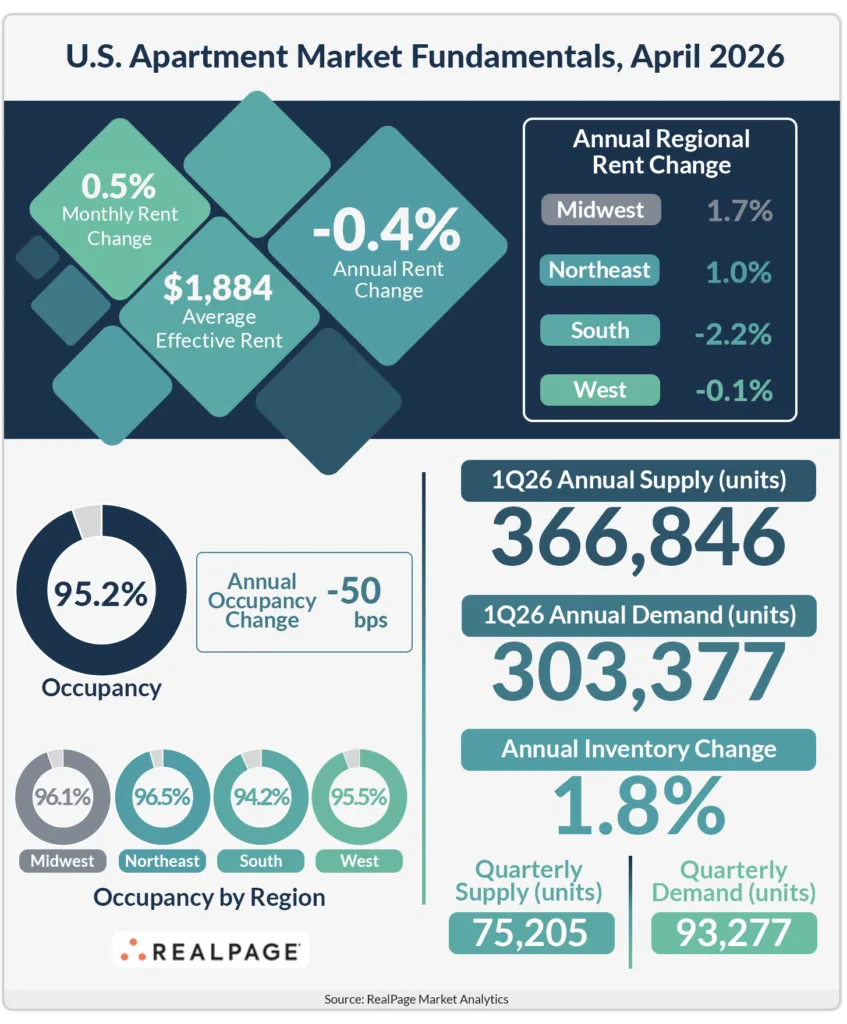

The US apartment market posted another month of incremental improvement in April, with occupancy returning above the 95% threshold for the first time since late 2025. According to RealPage Market Analytics, occupancy rose 20 basis points month over month to 95.2%, extending a four-month recovery that began after the market hit a cyclical low at the end of last year.

Rents also continued to stabilize, though pricing power remained limited in many major markets. Effective asking rents increased 0.5% in April, marking the fourth consecutive monthly gain. Even so, national rents remained down 0.4% year over year as operators continued to work through elevated supply levels across key Sun Belt metros.

A Slow But Steady Rebound

The latest data suggests the apartment sector is regaining footing after a difficult second half of 2025, when occupancy drifted lower amid record multifamily deliveries. While the national occupancy rate now sits above the “essentially full” benchmark of 95%, RealPage noted that the market remains roughly 50 basis points below year-ago levels.

The recovery has largely been driven by steady renter demand rather than aggressive rent growth. Monthly rent increases have stayed within a narrow range of 0.2% to 0.5% since January, indicating landlords are still prioritizing occupancy and concessions over pricing gains in highly competitive markets.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

Supply pressure remained concentrated in the South and parts of the West, where multifamily construction pipelines continue to weigh on fundamentals. RealPage reported that the South region has now gone nearly three years without annual rent growth.

Among the nation’s 50 largest apartment markets, Austin and Denver recorded the steepest annual rent declines, each falling more than 6% year over year as of April 2026. Phoenix and Charlotte also ranked among the weakest performers nationally due to rapid inventory growth and elevated new deliveries.

Several Sun Belt metros still posted strong absorption despite pricing weakness. Markets such as Dallas, Austin, Phoenix, and Charlotte continued attracting renters, but new units entered the market faster than demand could absorb them, forcing operators to maintain concessions and discounting strategies. That dynamic comes as developers pull back on new multifamily projects in several major metros, which could help ease supply pressure and stabilize rent growth over the next few quarters.

Tourism-heavy metros including Tampa, Nashville, and Las Vegas also showed softer apartment performance. RealPage tied some of that weakness to slowing discretionary travel spending and broader economic uncertainty affecting consumer behavior in 2026.

Tech Hubs Regain Momentum

Coastal technology markets continued separating themselves from the broader national apartment market. San Francisco led the country with annual effective asking rent growth of 9.6% in April, according to RealPage Market Analytics. San Jose followed with 5% annual growth, while Virginia Beach posted gains of 4.6%.

The strength in tech-centric markets reflects renewed hiring tied to artificial intelligence and high-wage technology jobs, trends that have helped support renter demand even as affordability challenges persist. Unlike many Sun Belt metros, several coastal markets also face more constrained supply pipelines after years of slower multifamily development activity.

Midwestern apartment markets posted more modest but stable growth. Milwaukee, Chicago, Minneapolis, St. Louis, and Cincinnati all recorded annual rent gains between 1.8% and 3.1%, supported in part by limited new supply deliveries.

Why It Matters

The apartment market’s gradual rebound highlights how demand fundamentals remain intact despite elevated construction activity and broader economic uncertainty. National occupancy moving back above 95% suggests renters are continuing to absorb a historically large wave of multifamily supply.

At the same time, the sharp divide between oversupplied Sun Belt metros and supply-constrained coastal markets underscores how local development pipelines are increasingly shaping apartment performance. According to RealPage Market Analytics, markets with the largest inventory growth continue to face the steepest rent pressure, even when leasing demand remains healthy.

For operators and investors, that divergence is becoming central to underwriting decisions in 2026. Markets with slowing construction starts could recover pricing power faster once current deliveries stabilize, while heavily supplied metros may continue facing elevated concession activity through the near term.

What’s Next

Apartment fundamentals are likely to improve gradually through the remainder of 2026 as multifamily completions begin slowing from peak delivery levels reached over the past two years. Industry analysts will closely watch whether demand can continue absorbing existing inventory without triggering another wave of rent cuts in major Sun Belt markets.

Coastal tech markets could remain outperformers if AI-related hiring and office leasing momentum continue supporting high-income renter demand. Meanwhile, operators in supply-heavy metros will likely stay focused on occupancy preservation and concession management until construction pipelines normalize.