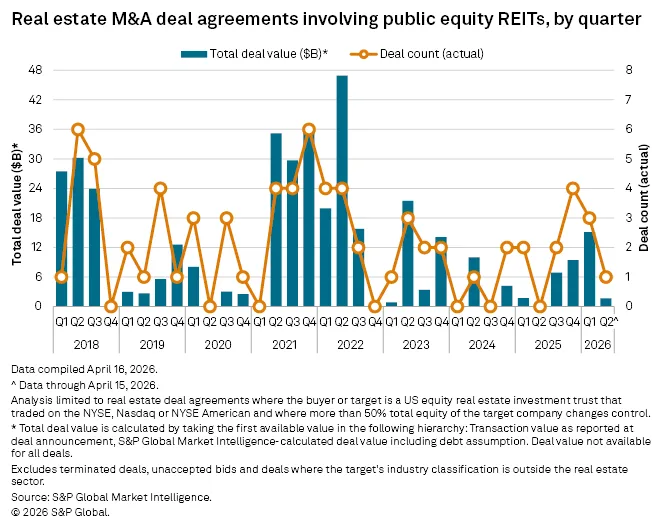

- US publicly traded equity REITs logged four M&A deals worth nearly $16.8B through April 15, with privatizations dominating the activity.

- Buyers targeted REITs trading at sizable discounts to net asset value, including Whitestone REIT, Veris Residential, Peakstone Realty Trust, and National Storage Affiliates Trust.

- The deal wave signals growing confidence among institutional investors and private equity firms that public REIT valuations remain disconnected from property fundamentals.

US REIT M&A activity continued to gain momentum through the first quarter and into April 2026 as institutional investors and larger REITs capitalized on depressed public market valuations. Four announced transactions totaling approximately $16.77B were recorded through April 15, according to S&P Global Market Intelligence data.

The deals included three take-private transactions and one public-to-public merger, underscoring how both private capital and strategic buyers are increasingly targeting undervalued REITs. The acquisitions span multiple property sectors, including shopping centers, self-storage, multifamily, and diversified commercial real estate.

Discounted REIT Valuations Fuel Acquisitions

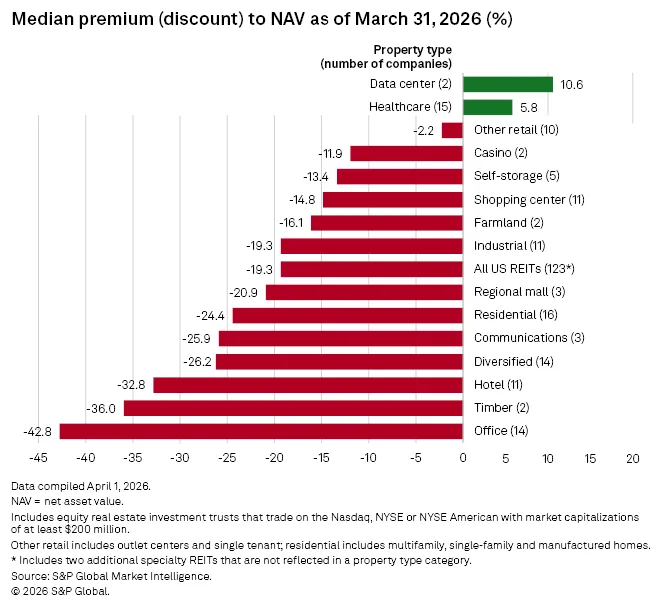

A major catalyst behind the recent surge in REIT M&A activity is the persistent discount between public REIT share prices and underlying net asset values. According to S&P Global Market Intelligence, US REITs with at least $200M in market capitalization traded at a median 19.3% discount to consensus NAV estimates at the end of Q1 2026.

Office, hotel, and timber REITs posted some of the widest valuation gaps, creating opportunities for buyers with long-term capital and higher risk tolerance. The disconnect has allowed private equity firms and larger REITs to pursue acquisitions at pricing levels well below estimated replacement costs and private-market valuations.

The Details

The largest transaction announced so far this year came on March 16, when Public Storage agreed to acquire National Storage Affiliates Trust in an all-stock deal valued at roughly $10.5B. National Storage shareholders will receive 0.14 shares of Public Storage common stock for each share owned, implying a value of $41.68 per share based on Public Storage’s March 13 closing price.

That offer represented a roughly 34.7% premium to National Storage’s prior closing price. Investors responded positively to the transaction, with National Storage shares climbing 36.4% through April 16 while Public Storage shares gained 1.4%.

Private equity buyers have also been active. On April 9, Ares Management announced plans to acquire Whitestone REIT in a $1.67B all-cash deal priced at $19 per share. The offer represented a 12.2% premium to Whitestone’s April 8 closing price and a 26.5% premium to its share price before Reuters reported in March that the REIT had hired advisers to explore strategic alternatives.

Earlier in the year, Veris Residential agreed to sell itself to a consortium led by Affinius Capital Advisors, Vista Hill Partners, and GIC Real Estate in a $3.4B transaction. The investor group offered $19 per share in cash, representing a 23.2% premium to Veris’ unaffected share price on Feb. 4, according to company disclosures.

Brookfield Asset Management also entered the mix in February, announcing plans to take Peakstone Realty Trust private in a deal valued at approximately $1.2B. Brookfield agreed to pay $21 per share in cash, a 34.4% premium to the REIT’s Jan. 30 closing price.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Private Capital Steps Back Into REIT Deals

The recent wave of transactions marks a notable shift after muted REIT M&A activity in 2023 and 2024, when elevated interest rates and financing uncertainty slowed acquisitions. Improving capital market conditions and stabilizing property fundamentals have reopened the door for strategic buyers. The rebound also aligns with broader expectations that commercial real estate dealmaking will accelerate in 2026 as buyers regain confidence and pricing gaps narrow.

Private equity firms, sovereign wealth funds, and institutional investors appear increasingly willing to acquire public REITs at discounts they believe public markets are overstating. Multifamily and self-storage assets, in particular, continue to attract strong investor interest due to relatively resilient operating fundamentals and long-term demand drivers.

At the same time, larger public REITs are using consolidation to scale portfolios and strengthen market share. Public Storage’s acquisition of National Storage Affiliates expands its footprint during a period when self-storage fundamentals remain comparatively stable versus other commercial property sectors.

Why It Matters

The pickup in REIT M&A activity could signal a broader repricing cycle across commercial real estate equities. Public REIT valuations have lagged private market pricing for much of the post-pandemic period, especially as higher interest rates pressured investor sentiment and increased financing costs.

For private equity firms and institutional capital providers, the current environment offers opportunities to acquire stabilized portfolios at discounts to replacement cost and intrinsic asset value. According to S&P Global Market Intelligence’s Q1 2026 data, the median REIT discount to NAV remains historically elevated, suggesting additional acquisition targets could emerge throughout the year.

What’s Next

Investors will likely watch whether additional REIT sectors see consolidation accelerate during the second half of 2026. Office REITs remain among the most discounted sectors, though operational uncertainty and refinancing risk could limit buyer appetite outside select high-quality assets.

Meanwhile, sectors with stronger fundamentals — including self-storage, multifamily, and necessity-based retail — may continue attracting both strategic acquirers and private capital. If REIT share prices remain disconnected from underlying property values, analysts expect the current M&A wave to extend deeper into 2026.