- Coworking model footprint grew 16.5% year-over-year, reaching 164M SF nationally.

- Medical office projects rose in share of new construction as general office starts declined.

- National office vacancy rate dropped to 17.8% in March, with significant market variation.

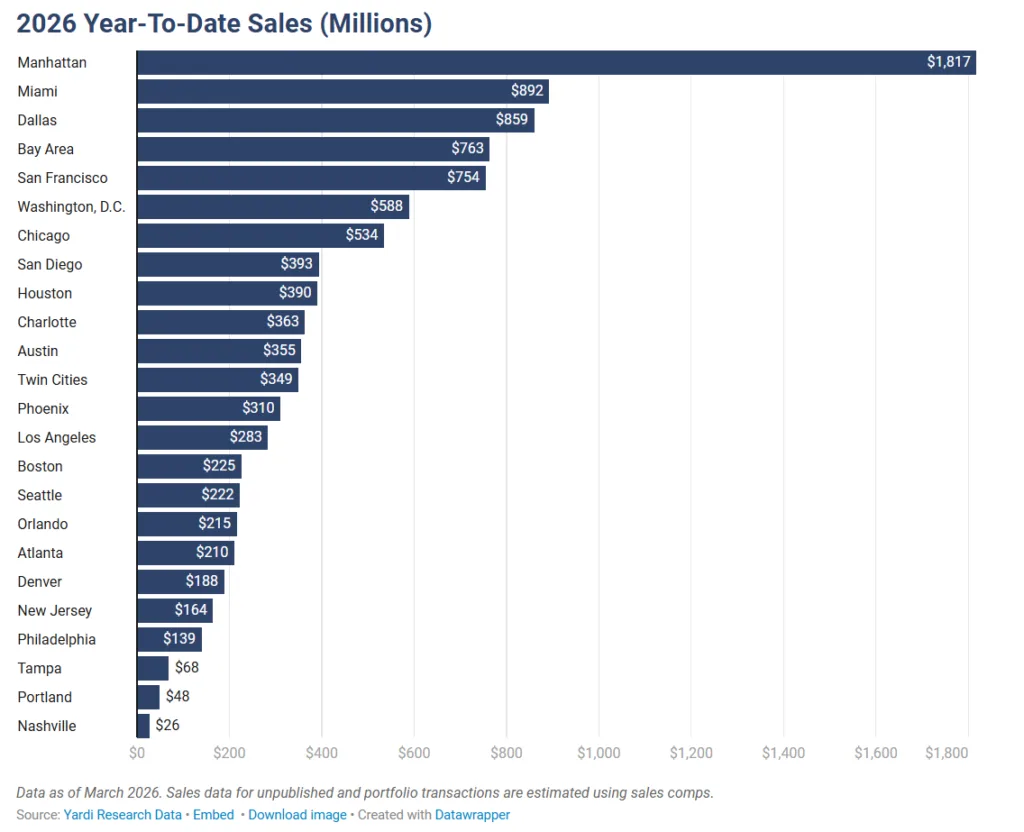

- Manhattan, Miami, and Dallas led office sales volume so far in 2026.

Flexibility Fuels Coworking Model Growth

CommercialCafe reports that coworking model demand is accelerating as tenants seek flexibility and property owners adapt to changing office needs. The sector now makes up 2.3% of total US office inventory, with the coworking footprint increasing to 164M SF—a 16.5% jump year-over-year.

Leasing trends indicate ongoing preferences for short-term, amenity-rich, and flexible arrangements. Owners are offering concessions that resemble coworking terms, including shorter leases, adaptable spaces, and partnerships with coworking providers. This evolution is in part a response to physical office attendance stabilizing around 55% since the pandemic, with hybrid work patterns persisting.

Medical Office Projects Gain Share

The medical office sector is expanding its share of office construction amid falling groundbreakings for general office developments. Of the 21.6M SF in new office starts last year, 25.8% were medical office—up from 10.9% in 2020. This steady demand is attributed to job growth in health care and the sector’s resistance to remote work disruptions. At the same time, capital continues to rotate toward more resilient office formats as investors look for stability across a shifting sector.

As of March, 29M SF of office projects are under construction nationwide, with 4.3M SF delivered in the first quarter of 2026. Developers are increasingly targeting medical and life sciences properties where fundamentals remain strong.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Divergent Office Market Trends

The national office vacancy rate reached 17.8% in March after a 210 basis point annual improvement, but market conditions vary widely. Miami (12.5%) and Manhattan (13.1%) posted the lowest vacancy rates among major US metros, while Austin and San Francisco remain elevated above 23%.

Listing rates also diverge by region. Manhattan tops the nation at $69.80 PSF, followed by San Francisco ($62.73 PSF) and Miami ($59.10 PSF). Midwestern and Southern markets, such as Detroit ($21.02 PSF) and Houston ($28.19 PSF), are among the most affordable.

Investment, Construction, and Outlook

Sales volume in the office sector totaled nearly $12.8B in the first quarter, paced by Manhattan ($1.8B), Miami ($892M), and Dallas ($859M). Notably, Los Angeles saw the majority of transactions close at a discount, with distressed pricing remaining commonplace.

New York and Boston lead the nation in office development pipelines, while Texas markets anchor new projects in the South. As hybrid and flexible models gain wider adoption, strategies will likely continue shifting toward coworking-inspired offerings and medical office development to match tenant demand.