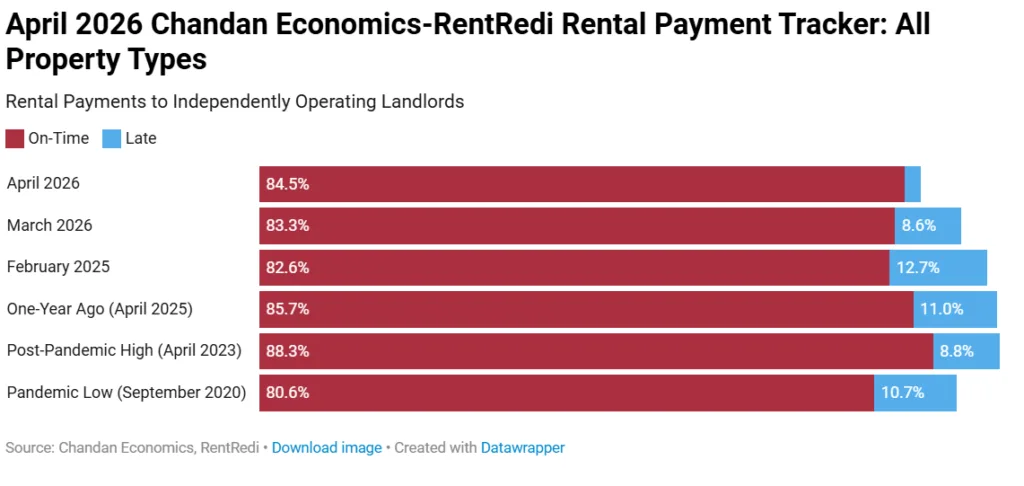

- On-time payments rose to 84.5% in April 2026, sixth monthly gain in seven months.

- Annual declines persist but are easing; on-time collections are 119 bps below April 2025.

- Full-payment rates improved to 97.2%, the highest since May 2025.

- Late-payment rates remain elevated, though slightly improved and regionally varied.

Independent Landlord Rental Performance Trends

On-time payment rates for independent landlord rentals continued to recover in April 2026. They reached 84.5%, marking the sixth increase in seven months. Data from RentRedi, tracked by Chandan Economics, shows improving resilience across the sector. The market has steadily rebounded since its low point in September 2025. Seasonal factors, including spring tax refunds, are likely supporting payment performance. However, the broader trend suggests a more sustained recovery is underway.

Despite this progress, the nature of improvement is uneven. Full-payment rates are up, indicating more missed payments are eventually resolved, but late payment pressure remains stubbornly high. This presents ongoing cash-flow management challenges for non-institutional landlords.

Annual Trends and Macroeconomic Context

April 2026’s 84.5% on-time payment rate remains 119 basis points below April 2025, making it the 33rd straight month of year-over-year collection declines. However, the pace of these annual setbacks has moderated notably since 2025, when deficits exceeded 300 basis points. Recent data suggests a gradual rebuilding of rental performance as 2026 progresses, extending the steady gains seen earlier in the year as collections began to stabilize after late-2025 weakness.

This improvement comes against a mixed economic backdrop. While US households have shown resilience, rising energy prices and cost-of-living concerns continue to threaten rental payment recovery, particularly among more financially strained tenants.

Resolution Rates and Late Payments

The forecast full-payment rate for April rose to 97.2%, the strongest since May 2025, signifying that many late or missed payments are eventually rectified. For all of 2025, the average full-payment rate was 96.0%—between 2023’s 96.6% and 2024’s 95.3% averages—highlighting relatively solid final incomes for landlords despite continued timing issues.

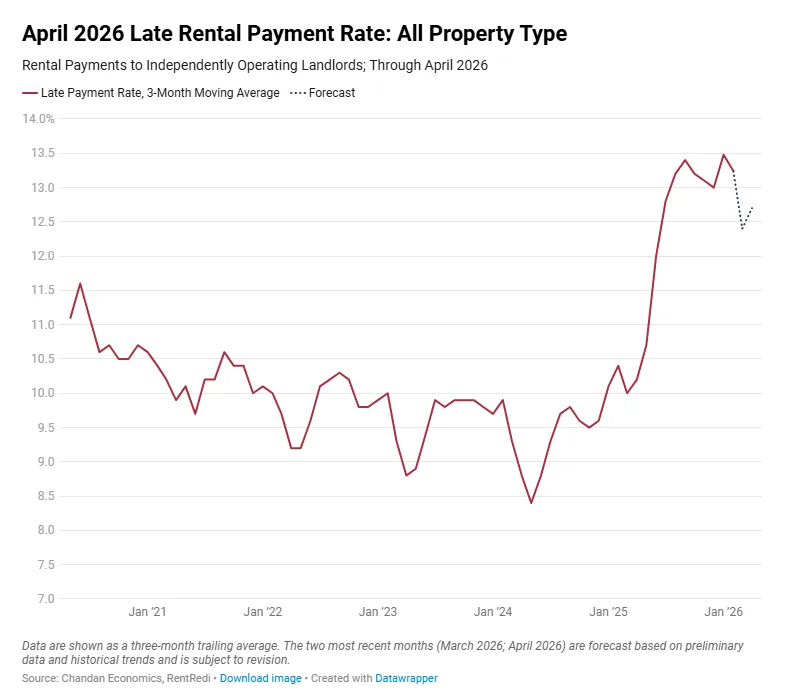

Late payments, however, persist at elevated levels. After climbing to a recent high of 13.5% in January 2026, late payments stabilized at 12.7% in April. Although many of these eventually resolve, persistent lateness limits prospects for further improvement in on-time rates and stresses landlord operations.

Performance by Property Type and Region

A performance gradient remains between property types. In April, 2–4-family rentals led at 85.3% on-time payments, followed by single-family rentals (84.6%) and multifamily properties (83.7%). All categories showed month-over-month improvement, confirming broad-based recovery, especially among smaller properties.

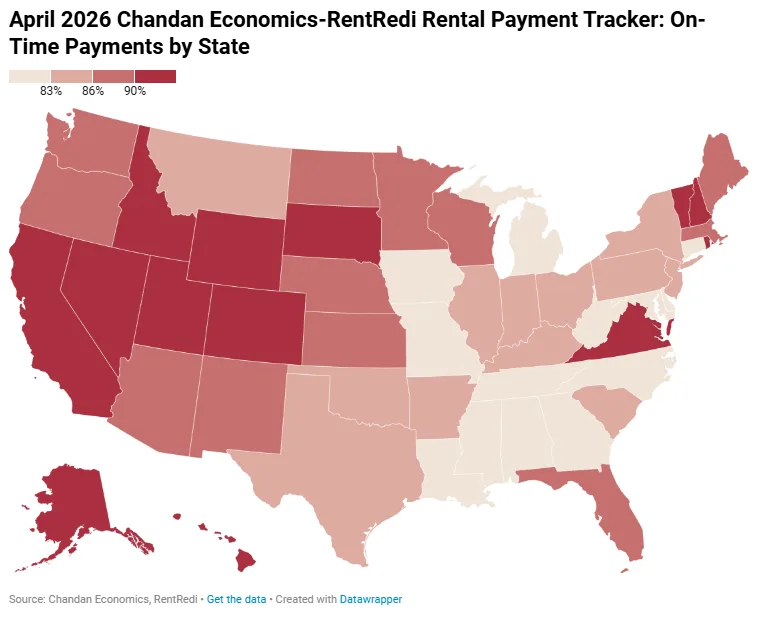

Regionally, Western and Mountain states continue to outperform, with Alaska (96.0%), Utah (93.1%), and Colorado (91.9%) among the leaders. Southeastern and select Mid-Atlantic states, including Mississippi (75.1%) and Maryland (78.3%), lag behind, reflecting variations in local economies and tenant financial health.

Why This Data Matters

The Independent Landlord Rental Performance report, based on over 65,000 units managed through RentRedi, is a key benchmark for the state of non-institutional rental housing. For operators, investors, and policymakers, these findings offer actionable insight on cash-flow stability and evolving risks in the independent rental sector as conditions shift through mid-2026.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes