- Grocery-anchored retail loans made up 28% of transactions but just 11.7% of retail issuance by dollar value since June 2025.

- Most grocery-anchored capital flowed into major gateway MSAs, with notable activity in select mid-tier markets.

- The sector’s broad, distributed footprint contrasts with luxury retail’s high-value, concentrated deals.

- This trend underscores a K-shaped market split by necessity-driven versus discretionary retail demand.

Consistent Issuance Across Diverse Markets

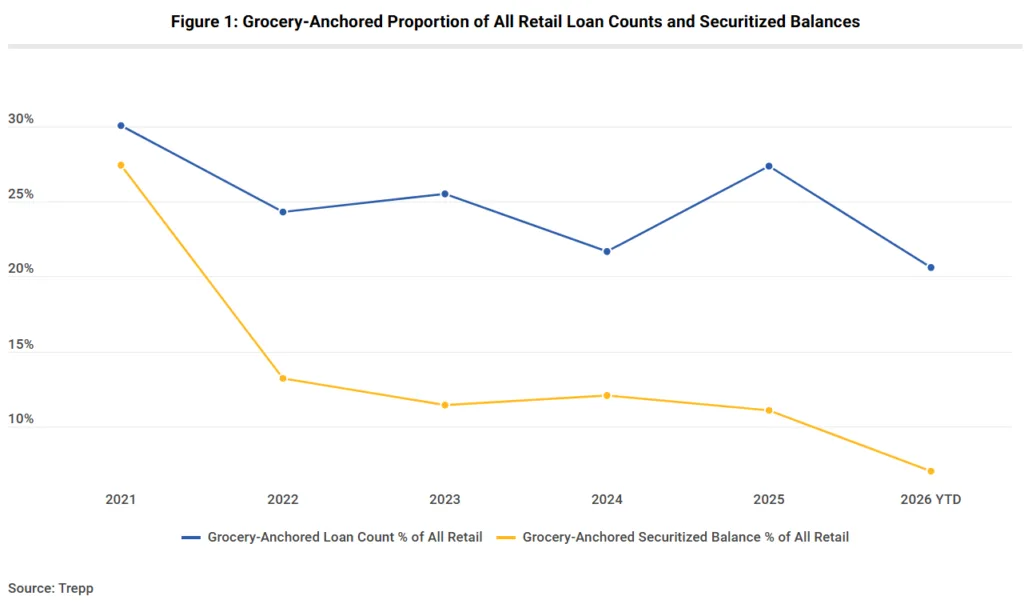

According to Trepp, grocery-anchored retail continues to capture steady investor attention, with 61 securitized loans totaling $1.4B closed since June 2025. While the sector accounts for only 11.7% of total retail loan balances, it represents 28% of all retail loan transactions, emphasizing smaller average deal sizes compared to other retail segments.

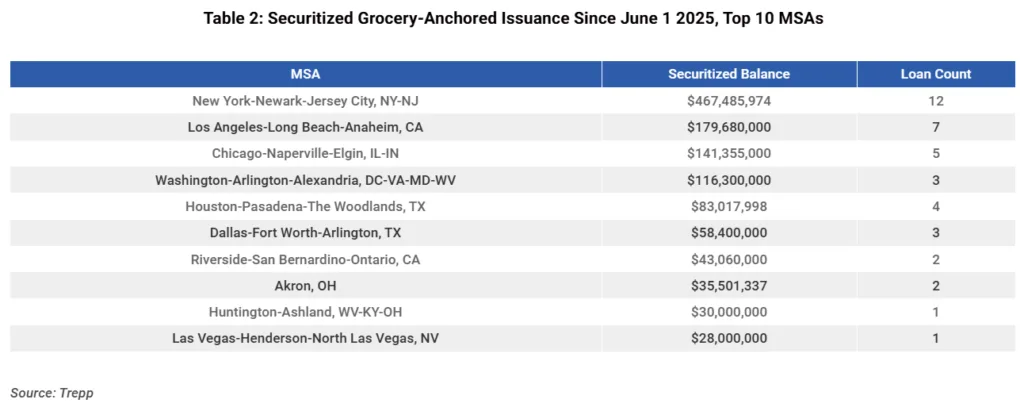

This capital deployment covers a geographically diverse mix, extending into mid-tier metros that often see little wider retail issuance. Large gateway MSAs remain dominant, but select working-class regions have drawn new investment in grocery-anchored assets as well.

K-Shaped Retail Market Dynamics

The period’s largest retail securitization was the $2.42B deal for Hawaii’s Ala Moana Center. It accounted for about 20% of retail issuance since June 2025. By comparison, grocery-anchored loans totaled roughly $1B less. They spread across many smaller deals rather than one large transaction. This gap reflects a K-shaped market. Luxury assets attract large, concentrated capital. Meanwhile, grocery-anchored retail sees broader but lower-value activity, driven by necessity spending.

Distinct Market Segments Emerge

Top markets for grocery-anchored issuance align with major metros like New York, Los Angeles, and Dallas. These cities remain core hubs for institutional retail capital. At the same time, the sector expanded into mid-tier cities like Akron, OH, and Huntington-Ashland, WV-KY-OH. This broader spread reflects how necessity-based retail continues to attract capital even as other CRE segments show uneven demand patterns across markets. These markets rarely appear in luxury or experiential retail rankings. Instead, they benefit from steady demand for everyday consumer essentials.

Sun Belt cities appear less prominently in the grocery-anchored space relative to other retail segments. The dichotomy underscores the K-shaped trend: necessity retail supports consistent activity across diverse markets, while luxury and experiential deals gravitate toward high-growth, affluent regions.

Why It Matters

Grocery-anchored retail’s measured but consistent securitized issuance illustrates a resilient, necessity-driven submarket within retail real estate. Its broad, distributed reach stands in contrast to the concentrated, flagship deals shaping the other side of the market. This trend reinforces the relevance of grocery-anchored assets for investors seeking stability amid shifting consumer patterns and market bifurcation.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes