- LightBox tracked 1,163 major CRE deals totaling $24.1B for January 2026.

- Multifamily, retail, office, and industrial collectively made up 87% of all transactions.

- January’s average deal size was $26.5M, with pricing showing mixed appreciation and discounts.

- Investor demand stayed diverse across geographies and asset types, signaling steady market momentum.

Steady Start for Major CRE Transactions

Commercial real estate deal activity launched 2026 with solid momentum, according to LightBox. January’s tally of 1,163 major CRE deals, representing $24.1B in total volume, kept pace with the year-end rally—though below December’s traditional spike in closings. Institutional capital remained engaged, recording 49 transactions above $100M and another 96 in the $50M–$100M range.

Lending Environment and Capital Flows

Lending levels rebounded in 2025 and capital availability remains strong entering 2026. Most lender categories—except office—are now on par with pre-pandemic activity. Debt markets saw tight spreads, and ample dry powder continues to support transaction flow as regional banks steadily re-enter the market, intensifying competition among lenders for high-quality CRE loans as financing activity picks up.

The 10-year Treasury near 4.15% has improved refinancing feasibility. Capital is targeting high-quality, durable assets as lenders maintain disciplined underwriting amid an uneven sector recovery.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Asset Class Breakdown: Even Competition

Deal activity in January was nearly evenly split among the four primary CRE sectors. Multifamily led with 24% of transactions, retail followed at 23%, office at 21%, and industrial at 19%—reflecting persistent investor confidence across the major food groups.

- Multifamily: Still a top choice despite oversupply, with performance varying by metro. High costs for homeownership continue to support rental demand. Refinancing pressures and oversized expenses are key risks for 2026.

- Retail: Investment targets remain concentrated in high-income areas and open-air centers, buoyed by low vacancy, limited supply, and healthy absorption. Delinquencies remain low, and valuation trends upward.

- Office: Deal flow rose to 21% of January volume, with renewed investor interest. Distressed sales still command deep discounts, while high-end and trophy assets attract competitive bidding amid gradual rent stabilization.

- Industrial: Vacancy has started to stabilize post-pandemic as rent growth moderates. Smaller bay assets near cities see the strongest fundamentals, with demand driven by e-commerce and logistics needs.

Deal Pricing: Wide Dispersion Remains

January’s transactions ranged widely in size and pricing outcome, from a $300,000 retail sale in North Carolina to a $1B New York City self-storage portfolio. Excluding the mega-portfolio, average deal size was $26.5M.

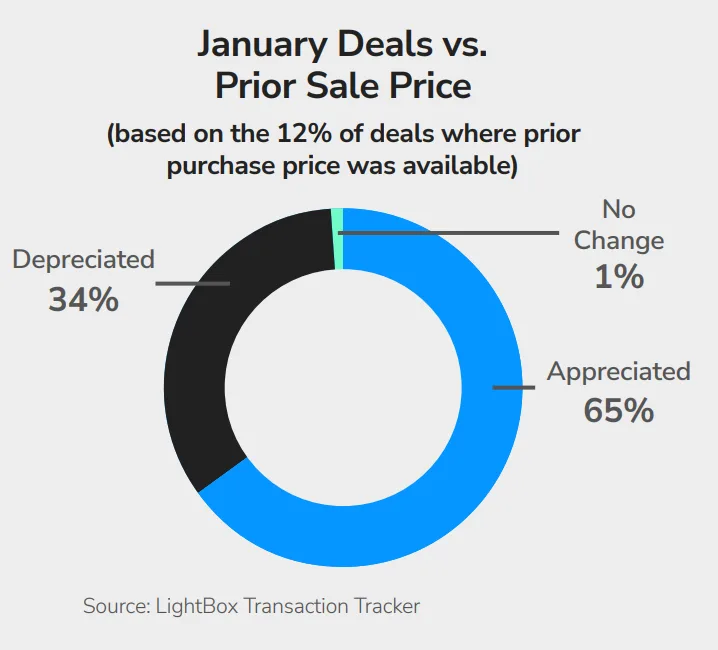

Among deals with available prior sale data, 65% appreciated while 34% sold at a discount—mostly in the office sector. The largest price gain was a Florida industrial property sold $55M above its 2021 price; the biggest office resale climbed from $48.6M to $103M.

Buyers Stay Active—and Varied

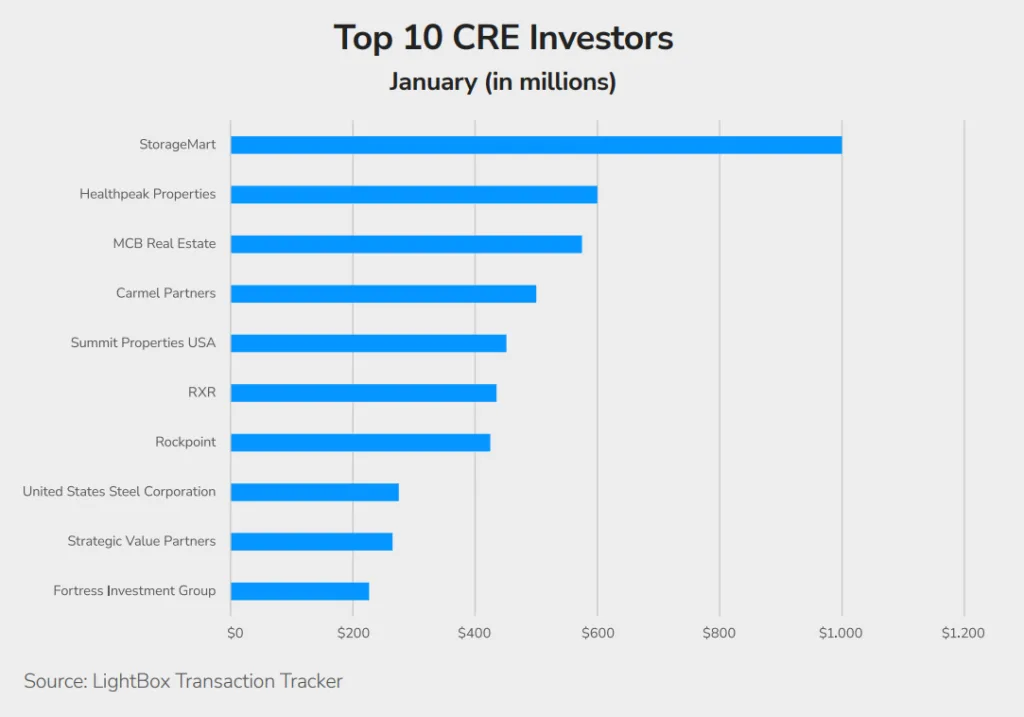

January data shows a broad and diverse buyer pool. Major CRE investors included public REITs, private equity, credit funds, and operating partners. The top ten deals featured three large portfolios and assets across New York, California, and Sun Belt markets, reinforcing both Manhattan’s deal volume and interest in life sciences, logistics, and growth geographies.

Strategic investors like Healthpeak, StorageMart, and Fortress were among those deploying capital, with structured and minority-stake moves signaling more creativity in capital stacks. The market’s disciplined but confident tone continues into 2026.

Outlook: Discipline and Steady Improvement

January volume signals a solid foundation for the year ahead in major CRE. Available debt, active equity capital, and steady refinancing are expected to drive continued deal flow. The market outlook is one of cautious optimism—returns will be income-driven, with underwriting, asset management, and tenant retention in sharper focus. Unless macro volatility worsens, the LightBox Transaction Tracker points to sustained, disciplined momentum for major CRE deals in 2026.