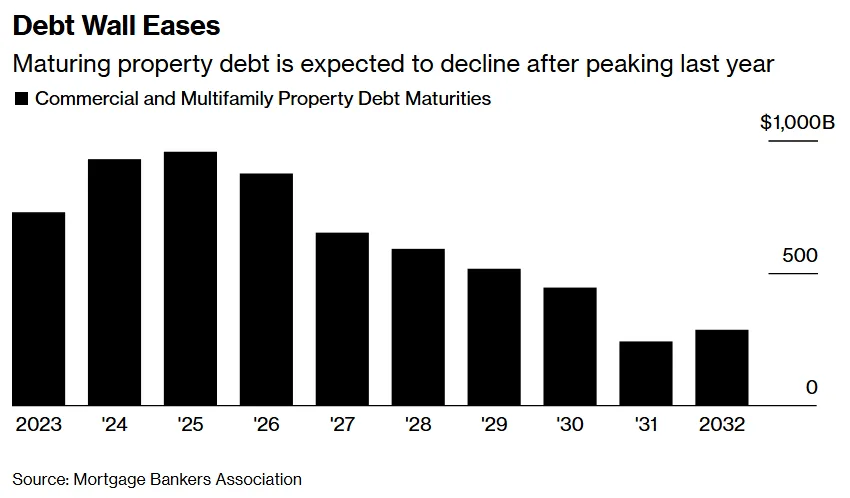

- Property debt maturities for commercial and multifamily are projected to drop 9% to $875B in 2026.

- Loan originations are set to rise 27% to $805B, signaling renewed lender activity.

- $167B in office loans will still mature in 2026, underscoring sector-specific risks.

- The improved lending environment comes amid forecasts for a gradual economic slowdown.

Debt Wall Recedes

According to Bloomberg, the long-anticipated ‘maturity wall‘ in US property debt is starting to shrink. The Mortgage Bankers Association (MBA) projects that commercial and multifamily real estate debt maturities will decline 9% to $875B in 2026, down from last year’s $957B. This marks the beginning of a steady trend, with maturities expected to recede further each year through 2031.

Lending and Originations Recover

Lenders are showing renewed willingness to originate new commercial real estate debt. The MBA forecasts $805B in new originations this year, a 27% increase from 2025. The multifamily sector will see $399B in lending, representing a 21% year-over-year rise. Much of the activity is driven by refinancings and acquisitions as borrowers seize relatively favorable financial terms. That rebound in activity builds on momentum seen earlier this year, when quarterly data showed a sharp jump in commercial mortgage volume as capital markets began to thaw.

Persistent Office Debt Risks

Despite the easing maturity wall, $167B in office mortgages remain set to mature in 2026, with another $123B coming due in 2027. While the volume is expected to decrease to $76B by 2028, risk remains concentrated in this challenged sector as delinquencies could increase for older loans.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Broader Economic Context

Cautious optimism prevails among industry experts. Projections by MBA’s economists indicate that GDP growth will slow to 1.9% this year and unemployment will rise modestly. The outlook suggests only a single federal funds rate cut in 2026, with Treasury yield curve steepening anticipated due to persistent fiscal pressures.