- Multifamily investment activity is picking up, with more deals projected in 2026 than last year.

- Debt capital availability is improving, helped by agency lenders and renewed liquidity.

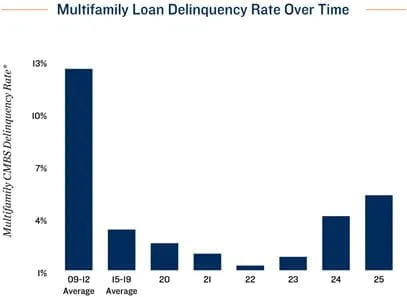

- Lenders are accelerating distressed asset resolutions, ending ‘extend and pretend’ strategies.

- Sun Belt oversupply and slower job growth remain watchpoints amid a broadly optimistic outlook.

Investor Momentum Builds

Investment activity and optimism in the multifamily sector were apparent at the 2026 National Multifamily Housing Council (NMHC) Conference. Marcus & Millichap reports that investors are expanding acquisition targets, anticipating a better market climate this year. Institutional and major funds expressed heightened confidence, with many planning to increase transaction volumes compared to 2025.

Despite fewer syndicators attending, those present represented established operators with strong performance records. However, ongoing supply issues in Sun Belt markets and slower job growth were identified as headwinds that could weigh on multifamily trends throughout 2026.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Debt Capital Access Expands

Attendees noted a rebound in debt capital availability, particularly from agency lenders and private sources. Fannie Mae and Freddie Mac have increased lending allocations by 20 percent, contributing to improved financing conditions for multifamily trends. While expectations are for modestly lower interest rates, uncertainty remains part of the outlook.

A notable shift is underway in lender behavior. Banks and lenders are addressing distressed loans more proactively, moving assets to market rather than continually extending loan terms. This approach is poised to bring discounted multifamily assets to market, providing opportunities for investors and clarity for lenders.

Why It Matters

The NMHC Conference signaled renewed momentum for multifamily trends heading into 2026. Improved access to debt, a potential turnover of distressed assets, and growing institutional participation all point to the early stages of a healthier investment cycle. Even as supply challenges persist, the overall sentiment is one of cautious optimism for the sector’s near-term performance, echoing the broader recovery in investor confidence observed across commercial real estate entering 2026.