- Multifamily investment conditions improve in 2026 as capital markets stabilize and development slows sharply.

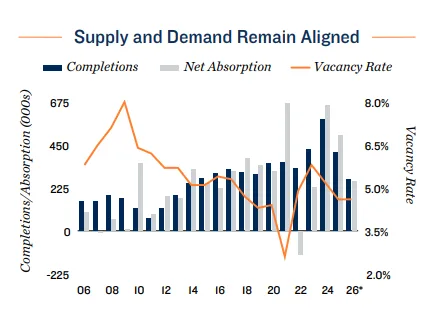

- National vacancy rates are steady, and supply growth is at its lowest since 2014, supporting occupancy and rent growth.

- Demographics, migration, and barriers to homeownership continue to drive resilient rental demand across most markets.

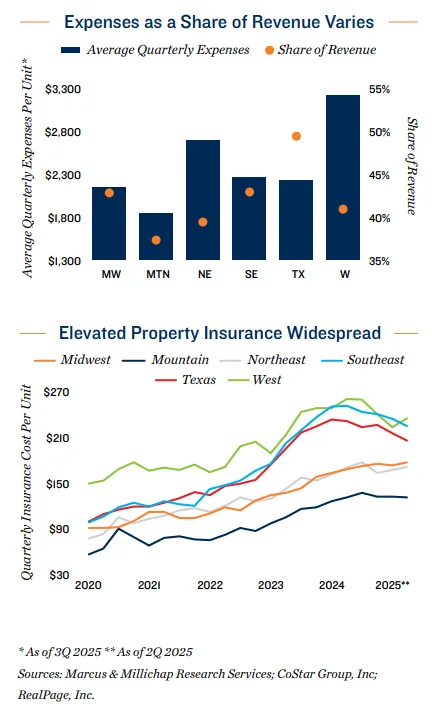

- Risk remains for lower-quality assets in labor-sensitive markets, but overall sector outlook is defensive and stable.

Investor Momentum Builds

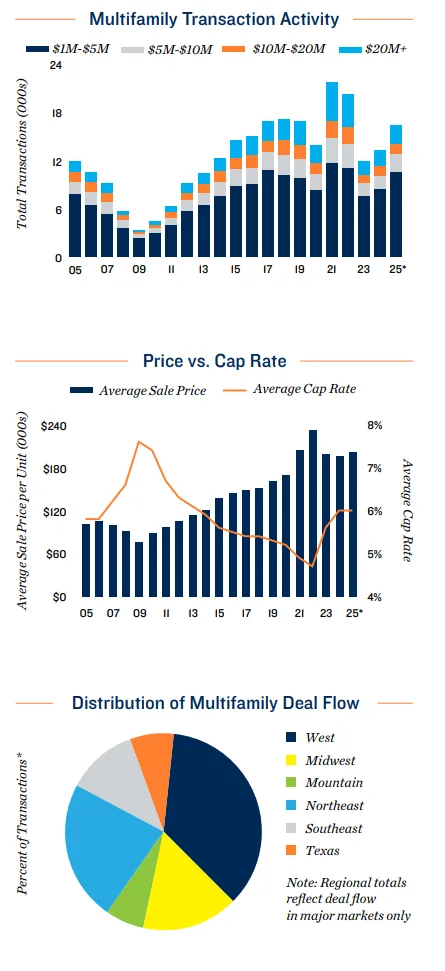

According to Marcus & Millichap, the 2026 multifamily investment outlook points to renewed momentum for rental housing investors. Improving capital markets, a sharp slowdown in new construction, and continued demand for rental units underpin the positive sector sentiment. Both private and institutional buyers are more active, many acquiring properties below original asking prices as lending activity rebounds and dry powder is deployed.

Why It Matters

National vacancy sits just below the long-term average, with urban and suburban rates closely aligned. Around 270,000 new units are slated for completion in 2026, marking the slowest supply growth in over a decade. This contraction comes as permit and construction activity fall across every region, supporting stable to rising occupancy. High barriers to homeownership and constrained for-sale housing further support multifamily demand, especially for Class A assets.

Capital Markets Rebound

Banks and government agencies have expanded multifamily lending capacity, with Fannie Mae and Freddie Mac each increasing caps to $88B for the year. Commercial real estate borrowing costs have eased moderately after Federal Reserve rate cuts, with agency debt available in the high-4% range. The Mortgage Bankers Association expects multifamily lending volume to rise by more than 10% compared to last year. Distress remains minimal and localized, while cap rates have stabilized to support positive leverage for many buyers.

Demographic Drivers in Focus

Demographic shifts are reshaping multifamily investment patterns. Modest immigration and higher young adult unemployment have delayed household formation, but long-term demand remains intact. The 65+ renter population is expanding rapidly, and dual-income households now comprise nearly half of all married couples, both trends supporting renewal rates and ongoing rental demand. Key in-migration metros like Dallas-Fort Worth, Phoenix, and Atlanta continue to attract investor attention due to robust population gains.

What’s Next

With new development at multi-year lows and capital availability on the rise, the US multifamily sector is positioned for a busy investment year. Risks persist for lower-tier assets subject to labor market volatility, but supply-demand fundamentals are generally healthy. The multifamily investment outlook for 2026 remains among the most defensively attractive in US commercial real estate.

Urban core markets like NYC and LA are expected to see a resurgence in deliveries after a subdued pipeline in recent years, reinforcing the focus on gateway cities even as Sun Belt metros attract investor attention.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes