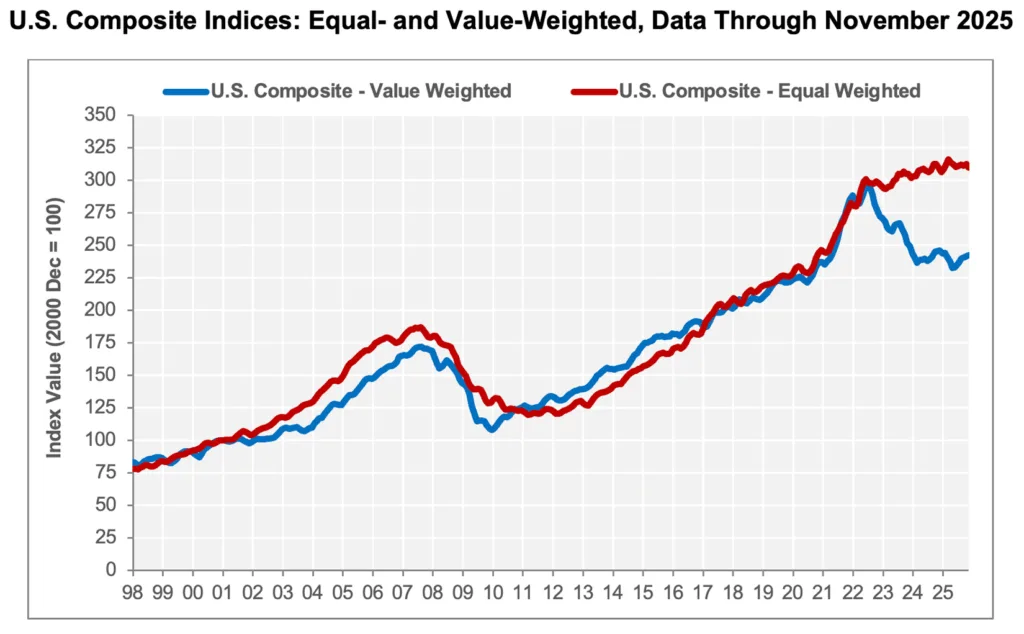

- High-value assets kept gaining value, with the value-weighted index up 0.4% in November—marking six straight months of growth. Prices for smaller assets fell 0.9%.

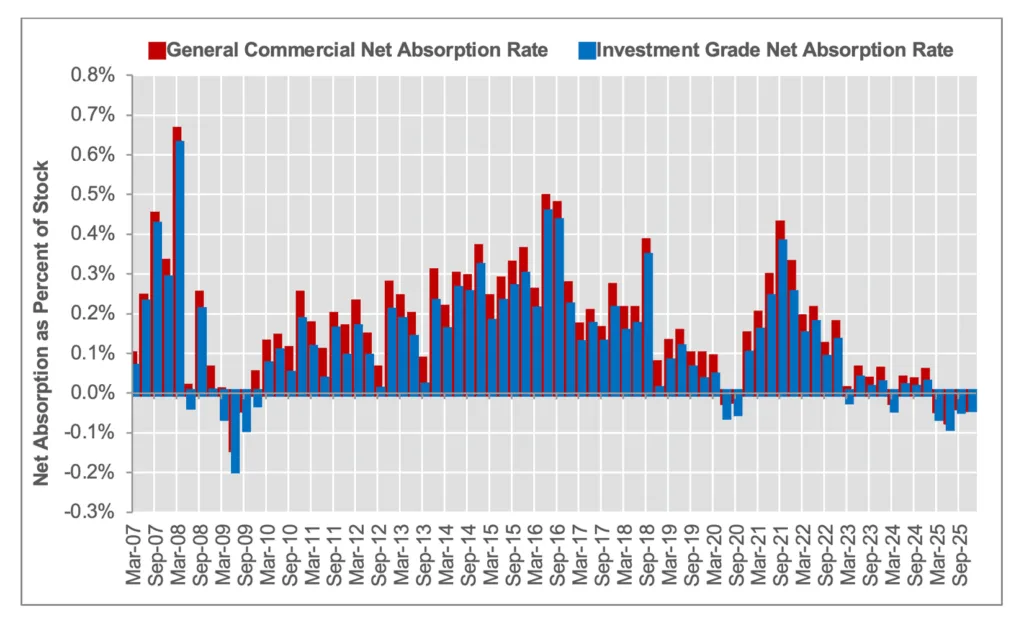

- Demand remains weak, with net absorption expected to fall by 100M SF this year. But quarterly losses are easing.

- Distressed sales stayed level, making up 4% of repeat trades in November.

High-End CRE Prices Keep Rising

The US commercial real estate market continued to split into two tiers in November. According to CoStar’s latest Commercial Repeat Sale Indices (CCRSI), high-value properties in core markets saw stronger pricing. The value-weighted index rose 0.4% from October and gained 1.1% over the last quarter. However, it remained 1.3% below November 2024.

In contrast, the equal-weighted index, which tracks smaller and more frequent sales in secondary markets, fell 0.9% in November. The index stayed flat year-over-year and dropped 0.7% over the quarter.

Institutional buyers remain active in core markets. They’re driving demand for large, premium assets. Meanwhile, smaller landlords and investors are seeing weaker pricing in less prominent areas.

Construction Pipeline Slows to a Crawl

Developers are hitting the brakes. Deliveries across office, retail, and industrial sectors are expected to total just 486.3M SF in 2025. That’s down 34.2% from last year and marks the lowest total since 2013.

Quarterly completions dropped below 100M SF for the first time in over a decade. Investment-grade buildings made up most of the deliveries, totaling over 408M SF. General commercial deliveries totaled just under 78M SF.

These deliveries represent only 0.2% of total inventory. For general commercial space, that share is less than 0.1%.

Absorption Still Negative, But Improving

Demand is still in the red. Net absorption for 2025 is projected to drop by 100M SF—the largest annual loss since 2009. Yet, there are signs of improvement.

In the third and fourth quarters, demand losses slowed. Investment-grade properties lost 55.5M SF in 2025. General commercial space gave back 44.4M SF. Some residential segments, like student housing and mid-tier apartments, are starting to show modest leasing improvements, offering a contrast to broader commercial softness.

Both segments remain negative, but quarterly figures suggest the worst may be over.

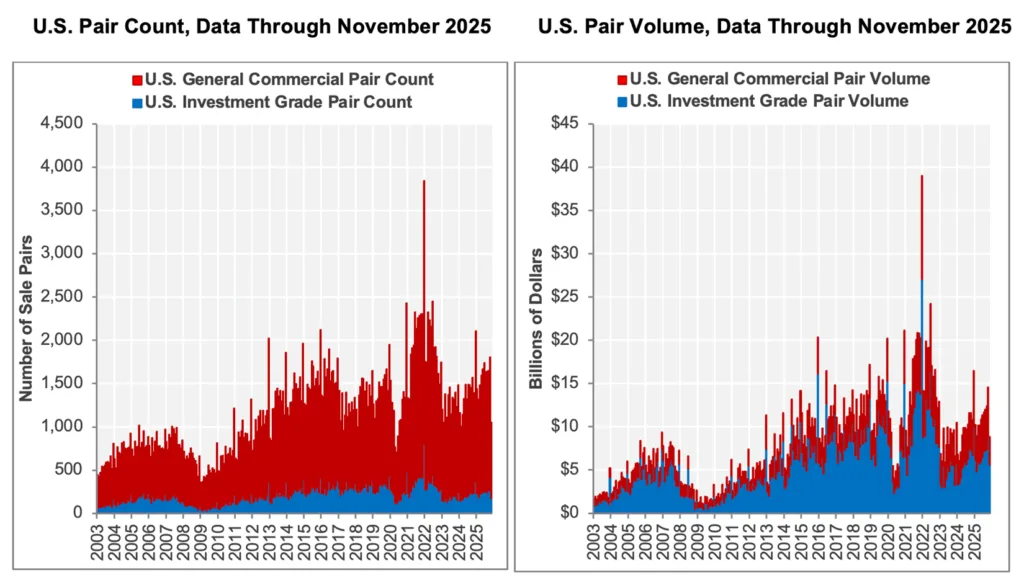

Sales Activity Cooled After Strong October

After a strong October, repeat sales activity fell in November. Sales volume dropped 41.8% month-over-month, with just 1,049 trades totaling $8.9B. That’s down from $14.5B in October.

Investment-grade sales totaled $5.7B in November, falling 35.9%. General commercial trades dropped 44% to $3.2B.

Still, total transaction volume over the last 12 months hit $138B. That’s up 21.5% from the year before. Investment-grade assets made up nearly 64% of that volume.

Distress Levels Hold Steady

Distressed deals remained stable. In November, 42 of the 1,049 repeat sales (4%) were distressed. The investment-grade segment had 10 distressed trades, or 5.7% of the total. General commercial had 32 distressed sales, or 3.7%.

These levels are in line with recent months. There’s no clear sign of a spike in forced selling.

Why It Matters

CRE markets are at a turning point. Capital is flowing back into top-tier assets thanks to lower interest rates, but supply is shrinking and demand remains soft. The Federal Reserve has cut rates three times since September, pushing borrowing costs to their lowest since 2022. That shift has helped revive institutional buying.

Smaller assets, however, continue to struggle. Developers are pausing projects, which could lead to tighter supply in future years if demand recovers.

What’s Next

The final weeks of December will reveal more about Q4 trends. CoStar’s Chad Littell says many deals are still closing. “There should be a lot of deals coming to light in the final days of December,” he noted. “We won’t know the full story until late January.”

As borrowing costs stabilize and construction slows, pricing could strengthen. But for now, the recovery remains concentrated in high-value, investment-grade properties in major markets.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes