Real Property Captive Overview

Real Property Captive (RPC) is a turnkey captive insurance platform that allows mid-market commercial and multifamily real estate owners to access the benefits of self-insurance without building and operating their own insurance company. Captive insurance structures, widely used by large institutions and over 90% of Fortune 500 companies, enable participants to retain underwriting profits and better align insurance costs with actual risk.

RPC brings this model to the middle market by aggregating portfolios across multiple owners, creating institutional-scale buying power while maintaining participant ownership of results. The platform also addresses key inefficiencies in traditional insurance, where premiums rise regardless of performance and strong operators subsidize weaker risks.

Designed for disciplined owners with diversified portfolios and at least ~$400,000 in annual premiums, RPC provides a scalable path to captive ownership. The program currently represents approximately $8.2 million in premiums across participating firms, with plans to expand significantly over time.

Our Take On Real Property Captive

Best for mid-sized real estate owners ($350K–$4M in annual premiums) with diversified portfolios and strong loss histories who want greater control over insurance costs.

Real Property Captive offers a structured path into captive insurance for property owners who may not have the scale or resources to form a standalone captive.

Pros

Pros- Access to institutional buying power and wholesale pricing

- Retention of underwriting profits and insurance float

- Turnkey implementation (~30 days)

- Reduced brokerage and administrative costs

- Purpose-built for real estate portfolios

Cons

Cons- Requires a strong underwriting profile (sub-35% loss ratio)

- Minimum premium thresholds limit accessibility

- Limited liquidity due to regulatory reserve requirements

Pros Explained

Access to Institutional Buying Power and Wholesale Pricing: Real Property Captive aggregates risk across a diversified group of property owners, creating the scale that individual operators cannot achieve on their own. This aggregation unlocks wholesale pricing on fronting, reinsurance, and administrative services—benefits typically reserved for institutional portfolios. It also improves negotiating leverage with carriers and reinsurers, helping stabilize pricing over time.

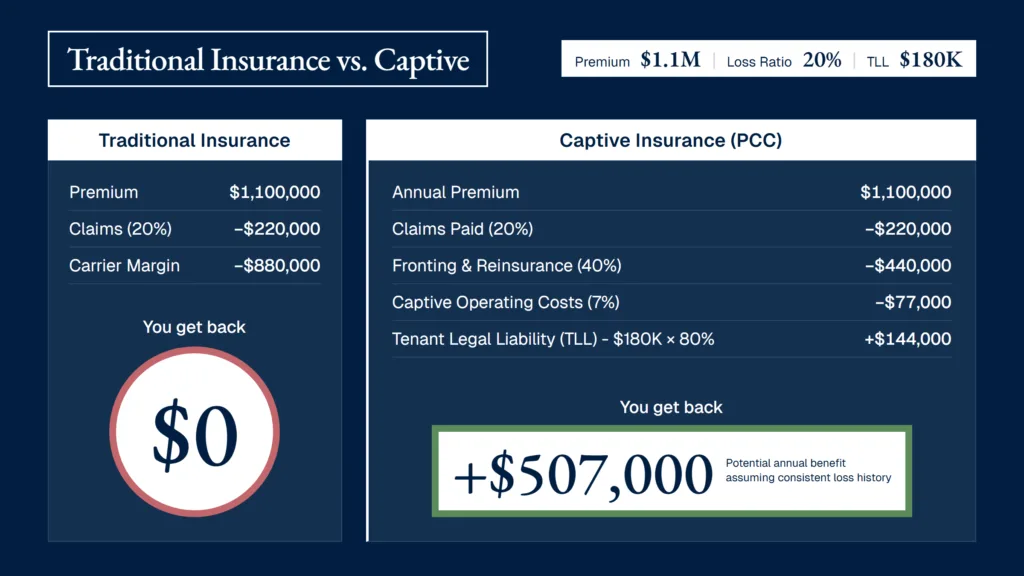

Retention of Underwriting Profits and Insurance Float: Unlike traditional insurance, in which carriers retain profits from favorable loss performance, Real Property Captive allows participants to keep those economics. Unused premiums remain within the captive and can be returned as dividends, while also generating investment income (“float”) in low-risk instruments. Over time, this can meaningfully offset insurance costs.

Turnkey Implementation (~30 Days): Real Property Captive offers a pre-built, fully operational infrastructure, allowing participants to onboard in approximately 30 days. This is a significant advantage over standalone captives, which can take 6–12 months to establish and require extensive coordination across legal, actuarial, and regulatory stakeholders.

Reduced Brokerage and Administrative Costs: By minimizing reliance on traditional brokerage layers and consolidating services within a single platform, Real Property Captive reduces frictional costs embedded in conventional insurance structures. This streamlined approach ensures more premium dollars go toward actual coverage and retained earnings rather than intermediary fees.

Purpose-Built for Real Estate Portfolios: The platform is specifically designed for real estate risk, accounting for the nuances of property portfolios, including geographic exposure, asset concentration, and lender requirements. This specialization results in more relevant underwriting, better-aligned coverage structures, and a more efficient operating model compared to generalist captive solutions.

Cons Explained

Requires a Strong Underwriting Profile (Sub-35% Loss Ratio): Real Property Captive targets disciplined operators with consistent loss histories. Owners with higher or volatile claims may not qualify, limiting accessibility to best-in-class portfolios.

Minimum Premium Thresholds Limit Accessibility: With a typical minimum annual premium of ~$400,000, smaller portfolios may not achieve the scale needed to benefit from the captive structure.

Limited Liquidity Due to Regulatory Reserve Requirements: Capital must remain in the captive to cover prior-year claims, even after exit, creating liquidity constraints that require long-term planning.

Real Property Captive Key Features

Group Captive & Protected Cell Structure

Real Property Captive offers both a group captive model and protected cell structures, providing flexibility based on participants’ size and sophistication. In the group model, members share a portion of risk while still maintaining individual loss reserves, benefiting from diversification across the broader pool. Larger participants can opt for protected cells, where their capital, underwriting results, and risk are legally segregated, allowing for full economic ownership without exposure to other members’ performance.

Participant Ownership & Governance

Unlike traditional insurance, participants are not just policyholders—they are owners. Each member holds equity in the captive and typically has voting rights on key decisions, including new member admission, vendor selection, and overall program governance. This structure ensures alignment across participants and creates accountability within the ecosystem, as only high-quality risks are admitted into the pool.

Fronting Carrier & Lender-Compliant Coverage

To meet lender and regulatory requirements, policies are issued through AM Best-rated fronting carriers. These carriers provide admitted insurance paper while reinsuring the risk back to the captive. This structure allows participants to maintain full compliance with financing requirements while still capturing the economic benefits of self-insurance.

Reinsurance Optimization Through Scale

Reinsurance is one of the largest cost drivers in property insurance. By aggregating portfolios across multiple operators, Real Property Captive improves diversification and underwriting confidence, leading to more favorable reinsurance terms. This reduces pricing volatility and minimizes the impact of individual portfolio concentration on overall costs.

Insurance Float & Dividend Distribution

Premiums paid into the captive are allocated toward loss reserves, operating costs, and reinsurance. Any unused capital—known as insurance float—is invested in low-risk assets, generating additional yield. Over time, surplus capital can be distributed back to participants as dividends, creating an additional return stream beyond cost savings.

Direct Distribution Model (Reduced Intermediation)

Real Property Captive minimizes traditional brokerage layers by enabling direct access to the program. This reduces commissions and administrative inefficiencies typically embedded in insurance placements, ensuring that more premium dollars are allocated toward coverage and retained earnings rather than intermediary fees.

Integrated Claims & Third-Party Administration

Claims are handled by licensed third-party administrators (TPAs), ensuring professional and standardized claims processing. Because TPAs are selected and overseen by the captive’s governance structure, they are directly accountable to participants—often resulting in better service and alignment compared to traditional insurance carriers.

Diversification-Driven Risk Efficiency

The platform is designed to reward portfolios with strong diversification across assets and geographies. By pooling risk across many properties, the captive reduces the likelihood of catastrophic loss concentration, which in turn lowers reinsurance dependency and improves long-term economics for participants.

Streamlined Onboarding & Underwriting Process

The onboarding process mirrors a traditional insurance renewal but is enhanced with deeper underwriting analysis. Participants submit standard documents—such as rent rolls (SOV), five-year loss runs, and current policies—and typically receive a decision within 30–60 days. Once approved, the captive is capitalized, and coverage can be activated quickly, minimizing disruption to operations.

Implementation Process

Joining the Real Property Captive program follows a structured, multi-step process that mirrors a traditional insurance renewal while incorporating deeper underwriting due diligence.

Initial Evaluation

Prospective participants begin with an introductory discussion to review their portfolio, insurance spend, and overall risk profile. This step helps determine whether the program is a strong fit based on scale, diversification, and historical loss performance.

Document Submission

Participants then provide standard underwriting materials, similar to what is required by a traditional insurance broker. These typically include:

- Property schedule or statement of values (SOV)

- Five-year loss runs

- Current insurance policies or lender requirements

Underwriting Review

Actuaries and captive consultants evaluate the submitted materials to assess eligibility, pricing, and required capital contributions. This process generally takes 30 to 60 days and focuses heavily on loss history, portfolio composition, and reinsurance considerations.

Capitalization and Onboarding

If approved, participants contribute capital as determined by the actuary and formally enter the captive structure. Coverage is then activated through fronting carriers, and the participant begins operating within the program—retaining underwriting economics while maintaining lender-compliant insurance coverage.

Claims & Risk Structure

Claims within Real Property Captive are managed through a licensed third-party administrator (TPA), mirroring the structure of traditional commercial insurance programs. Participants submit claims directly to the TPA, which handles evaluation, processing, and payout coordination based on the policy terms.

From an operational standpoint, the claims experience is largely unchanged for the policyholder. The key distinction lies in the economics behind the coverage. Rather than profits and losses accruing to a third-party insurer, all underwriting results—both favorable and adverse—flow back to the captive. This structure aligns incentives, as participants directly benefit from strong risk management and disciplined claims performance over time.

Cost Considerations

Captive programs like Real Property Captive are designed to deliver long-term economic advantages rather than immediate cost reductions. Savings are typically driven by several key factors, including reduced brokerage and administrative costs, better alignment between premiums and actual loss performance, investment income earned on insurance reserves, and the ability to retain underwriting profits within the captive.

That said, total insurance costs in the early years may be comparable to traditional policies. This is because pricing still relies on industry-standard underwriting models and reinsurance markets. The primary difference lies not in the initial premium but in who benefits from favorable outcomes.

Over time, participants with significant loss experience can realize meaningful savings through retained earnings and investment returns, making the captive structure increasingly advantageous over the long term.

Alternatives

Traditional Commercial Insurance

Most CRE owners rely on traditional insurance carriers due to ease of use and familiarity. While straightforward to implement, this model offers no participation in underwriting profits and often includes layered brokerage and administrative costs that reduce overall efficiency.

Standalone Captives

Large institutional owners may form single-parent captives to fully control their insurance strategy. Although this approach provides maximum flexibility and ownership, it requires significant capital, time, and operational infrastructure—making it impractical for most mid-sized portfolios.

Operator-Led Group Captives

Some real estate owners partner to form informal group captives. While these can offer shared risk benefits, they often lack standardized infrastructure and require substantial coordination across members, vendors, and service providers to operate effectively.

FAQs

A captive insurance platform that allows real estate owners to pool risk, retain underwriting profits, and access institutional insurance infrastructure.

Owners with $100M–$2B portfolios and $350K+ in annual premiums with strong loss histories.

Typically 30–60 days from submission to activation.

Yes. Policies are issued through rated fronting carriers.

Capital remains in place for a defined period to cover prior-year claims.

By aggregating risk, eliminating brokerage layers, and allowing participants to retain underwriting profits.

How We Evaluated Real Property Captive

When evaluating Real Property Captive, we examined several factors, including:

- Product and service offerings: We reviewed RPC’s captive structure and how its platform allows CRE owners to access captive insurance economics.

- Pros and Cons: We analyzed the potential advantages and limitations of participating in a captive compared with traditional insurance programs.

- Ease of implementation: We examined onboarding requirements, underwriting timelines, and operational complexity.

- Support infrastructure: We reviewed the program’s vendor network, including captive management, actuarial services, and claims administration.

- Cost considerations and transparency: We evaluated how RPC’s structure compares with standalone captives and traditional insurance markets.

Summary of Real Property Captive

Real Property Captive represents a significant evolution in CRE insurance, bringing institutional-grade captive structures to the middle market. By aggregating risk and centralizing infrastructure, it enables qualified operators to reduce costs, gain transparency, and participate in underwriting profits.

While the platform is still in its early stages, the underlying captive model is well established within corporate risk management. For property owners with significant insurance spend, diversified portfolios, and strong loss histories, programs like RPC may offer a path toward greater control over insurance costs and long-term risk management.

Disclaimer

This page may contain affiliate links. If you make a purchase or investment through these links, CRE Daily LLC may receive a commission at no extra cost to you. These recommendations are based on our direct experience with these companies and are suggested for their usefulness and effectiveness. We advise only purchasing products that you believe will assist in reaching your business objectives and investment goals. Nothing in this message should be regarded as investment advice, either on behalf of a particular security or regarding an overall investment strategy, a recommendation, an offer to sell, or a solicitation of or an offer to buy any security. Advice from a securities professional is strongly advised, and we recommend that you consult with a financial advisor, attorney, accountant, and any other professional who can help you understand and assess the risks associated with any real estate investment. For any questions or assistance, feel free to contact [email protected]. We’re here to help!