US Industrial Sees Lowest Q1 Absorption in 10 Years

Early data from CoStar Group suggest a significant downturn in US industrial net absorption

Jordan B. & Han-Gwon Lung

March 12, 2024

Together with

Good morning. The U.S. industrial sector faces its weakest Q1 performance in a decade due to excess space. Meanwhile, a new report shows the disparity in rent premiums across 100 metropolitan areas.

Today’s issue is brought to you by Matheson Capital.

👉️ Enjoy reading CRE Daily? Share the newsletter with friends, family, and colleagues and unlock deal screeners, financial models, and more.

Market Snapshot

|

|

||||

|

|

*Data as of 3/11/2024 market close.

INDUSTRIAL MARKET

US Industrial Faces Weakest Q1 Absorption in a Decade

The industrial sector is nearing its worst Q1 performance in more than 10 years, with early CoStar data indicating a major drop in US industrial net absorption.

Demand downturn: The current slump can be attributed to a decrease in demand from third-party logistics companies. Demand from these companies had previously surged during the early pandemic era due to a spike in e-commerce and the need for additional inventory storage. As the global supply chain stabilizes, these companies are scaling back, leading to an increase in sublease offerings.

Between the lines: Similarly, economic pressures have forced major retailers like Home Goods and Home Depot to close large amounts of distribution centers, complicating the leasing landscape for large single-tenant spaces.

Challenges for small biz: The industrial market’s shift has left smaller businesses in a bind, with a noticeable lack of new constructions suited to their needs. This scarcity is most acute for blue-collar industries, leading to a rapid lease-up of available small-bay spaces and further widening the gap with the big-box segment.

➥ THE TAKEAWAY

Looking ahead: Despite the downturn in demand and absorption, industrial has also shown resilience. The Federal Reserve’s Beige Book highlighted strong demand for industrial and manufacturing spaces, indicating a shift to these property types. Ongoing growth in online shopping continues to drive the need for more industrial spaces, as manufacturers continue to onshore operations.

PRESENTED BY Matheson Capital

Proven Value-Add Multifamily Investment Opportunity w/ 2.95% Loan Assumption

Matheson Capital is thrilled to present its latest investment offering, Residences at St. George, a 248-unit multifamily community located in Savannah, GA.

-

2.95% fixed rate loan with 8+ years of term remaining

-

Acquisition price of $156k/unit is below comparable sales from Q423

-

Proven value-add upside provides a clear path for NOI growth.

-

Savannah, GA is experiencing population and employment growth.

To learn more about this investment opportunity, click here.

Based in Charleston, SC, Matheson Capital specializes in Southeastern US real estate, with a proven track record of 15 acquisitions and seven exits since 2018 with an average LP IRR of 40%**.

*See the sponsor’s disclosures at the boom on the newsletter.. Please support our sponsors. It helps keep CRE Daily free.

✍️ Editor’s Picks

-

Missing millions: Investors like TPG Angelo Gordon and LibreMax Capital are shocked by a $164M holdback from a failed bond deal organized by Goldman Sachs back in 2021.

-

Suds over everything: Despite higher prices, car washes are booming in the U.S. with subscription models, and towns like Streetsboro, Ohio, are pushing back against oversaturation.

-

Sound stage showdown: The movie industry isn’t what it used to be yet, yet finance giants are continuing to bet billions on Hollywood sound stages.

-

Skid Row revamp: California’s Gavin Newsom speeds up the $2B Fourth & Central project, adding 1.5K homes, 410KSF of office, and a 68-room hotel in downtown LA.

🏘️ MULTIFAMILY

-

Real estate ethics: Slate Property Group bought a Manhattan apartment building for $120M and immediately raised rents, prompting mixed reactions.

-

Downsizing dreams: New construction homes are shrinking in size due to affordability constraints, with the median size now just 2.18KSF, down 4%.

-

Rethinking Queens: Slate Property Group and Grobman Gross secured $97M to refinance a luxury 166-unit Queens apartment building with retail.

-

Phoenix rising: Phoenix, AZ sees a surge in population growth due to its climate, affordability, and job market, enjoying a 1.6% annual growth rate.

-

Serving those who serve: The Michaels Organization (MIK) will invest $500M in a military housing portfolio of seven army installations nationwide, financed via a $305M bond issuance.

🏭 Industrial

-

Regulatory storm ahead: Virginia faces a wave of proposed legislation limiting data center growth, raising uncertainty for developers in a crucial market.

-

Equus expands: Equus Capital Partners expands its industrial presence in North Carolina, adding 1.4MSF for $124M, fully leased to key tenants.

-

Rivian revamp: Rivian’s (RIVN) $5B Atlanta plant project has been officially paused. The plant had been expected to employ 7.5K workers and produce 400K EVs yearly.

🏬 RETAIL

-

World Cup wonder: American Dream, near MetLife Stadium, faces financial challenges despite $553M in sales as it aims to attract future World Cup visitors.

-

District danger: D.C. faces a surge in violent crime, with homicides at a 26-year high, carjackings nearly doubling, and property crime up significantly.

🏢 OFFICE

-

Skyscraper standstill: Miami’s tallest tower, One Brickell City Centre, struggles to fill space, reflecting the cooling office market.

-

Building in a bind: 205 West Randolph in Chicago filed for foreclosure amid record vacancies, with $17M unpaid principal sought and just $100K in 2023 net cash flow.

Rent Premiums

A Snapshot of Rental Market Disparities

A recent analysis of the U.S. rental market unveils a clear divide: while renters in 21 out of 100 major metropolitan areas are locking in apartments at rates below the long-term average, others are contending with stiff premiums.

Discounts in select markets: Renters in at least 21 metro areas are benefiting from discounted rates, signaling favorable conditions for tenants. Boise City, ID leads the pack with a 5.45% discount on typical rental units, followed by Austin (3.27%), Phoenix (3.15%), Las Vegas (2.88%), and Spokane (2.62%). These cities saw rapid population growth and an influx of multifamily development.

Tight markets, premium rates: Certain markets exhibit tight housing conditions, resulting in premium rental rates for tenants. Cities like Springfield, MA (7.45% premium), Knoxville (7.18%), Madison (6.90%), New Haven (6.84%), and Syracuse, NY (6.71%) saw high demand coupled with limited supply. Local governments have their hands full trying to address the rental crisis.

Rental market paradox: South Florida, known as the “epicenter of the nation’s affordability crisis,” presents a paradoxical situation with a blend of holdover premiums and new discounts. Despite a slight rent drop in Miami in February, renters still face a 5.4% premium compared to projections. The affordability gap persists, with typical households needing a six-figure salary to avoid financial strain due to housing.

➥ THE TAKEAWAY

Challenges persist: The current rental market landscape offers a mixed bag of opportunities and challenges for U.S. renters. While some cities present discounted rates, making them attractive for renters, others grapple with high premiums due to inadequate housing development. Particularly in areas like South Florida, the affordability crisis continues to be a significant hurdle, affecting the livelihoods of many residents.

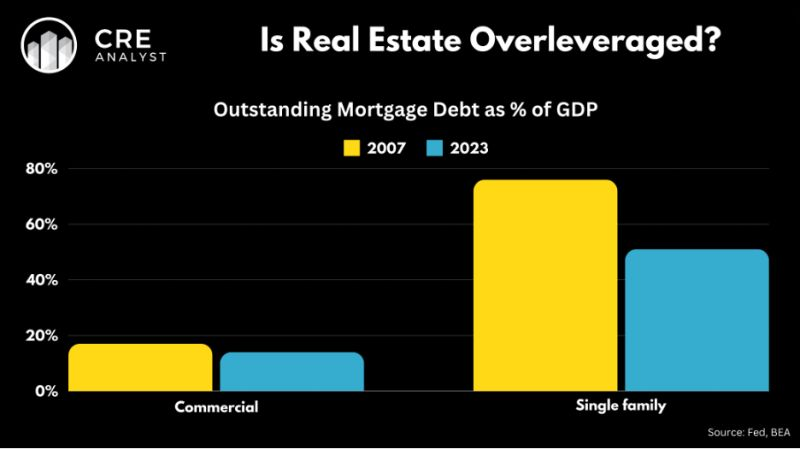

📈 CHART OF THE DAY

Is U.S. real estate overleveraged? According to CRE Analyst, not yet. Outstanding CRE and single-family residential mortgage debt levels are still below 2007 levels as a percentage of GDP. This disparity is most obvious in single-family properties, where outstanding mortgage debt hit nearly 80% of GDP before the GFC.

What did you think of today’s newsletter? |

* Financial metrics are projections and/or forward-looking statements, and not guarantees of profit. See risk factors and disclosures in Private Placement Memorandum for more details.

**LP IRR is based on the weighted average of seven realized sales.