San Francisco Faces Economic Headwinds, Credit Outlook Downgraded

San Francisco’s economic stability is on shaky ground, with S&P Global Ratings recently modifying the city’s debt outlook to “negative.”

Jordan B. & Han-Gwon Lung

April 25, 2024

Together with

Good morning. San Francisco’s economic stability is on shaky ground. Plus, the U.S. hotel industry reported its first YoY decline in revenue per available room (RevPAR) since the end of the pandemic

Looking to buy an apartment building or refinance an existing investment? CBRE has you covered. Get a quote today for your multifamily property.

Market Snapshot

|

|

||||

|

|

*Data as of 4/24/2024 market close.

PROPERTY REPORT

San Francisco’s Debt Dilemma: Credit Outlook Dips Amid Economic Struggles

San Francisco’s economic stability is on shaky ground, with S&P Global Ratings recently modifying the city’s debt outlook to “negative.”

What happened: The city reported an unprecedented office vacancy rate of 22%, substantially exceeding the national average of 13% and a drastic climb from its pre-pandemic low of 7%. In the tourism front, hotel occupancy has plummeted to 63% from a robust pre-COVID figure of over 80%, indicating a severe slowdown in one of the city’s key economic drivers.

Fiscal Challenges: Forecasts reveal a daunting financial future for San Francisco with an estimated $245 million budget deficit this year, escalating to $555 million next year. Projections suggest this could balloon to over $1 billion by 2027 if current trends persist. The city’s financial documents reveal that rising personnel costs, notably salaries and benefits, are the primary contributors to these fiscal challenges.

Adding to the problem: The shift towards remote work over the past four years has played a significant role in the downturn of downtown San Francisco. This shift, compounded by ongoing quality of life and safety concerns since the pandemic began, has stifled growth in property and business tax revenues, further complicating the city’s economic recovery.

➥ THE TAKEAWAY

What they are saying: S&P has expressed concerns over San Francisco’s ability to implement necessary budget cuts to regain financial equilibrium within the current outlook horizon. Without significant adjustments, there’s potential for further rating pressures, especially if the city’s general fund reserves begin to deplete rapidly. Despite this, S&P has maintained a AAA long-term rating on the city’s outstanding general obligation debt, highlighting the strength of the city’s reserves but also the need for substantial revenue recovery or corrective fiscal action to prevent a weaker credit profile.

TOGETHER WITH CBRE

Achieve the best financing terms available for your asset and capital stack strategy.

CBRE leverages long-term, established relationships with diverse capital sources worldwide to provide commercial real estate owners of all property types with creative and strategic financial solutions to meet their investment needs.

Find innovative options for any capital requirement with our unique combination of robust lender relationships, leading deal volume and proprietary technology.

Please support our sponsors. It helps keep CRE Daily free.

✍️ Editor’s Picks

-

Exit of Noncompetes: The FTC’s final ruling to ban noncompete clauses could reshape the commercial real estate industry by heightening competition for talent across all levels.

-

Economic shifts: U.S. private sector growth cooled in April, with PMI dropping to 50.9, while the eurozone, Japan, India, and Australia showed accelerated growth.

-

Tulip Tower: A Turkish developer unveils plans for a 902-foot-tall Miami tower with a hotel, condos, and office space, set for completion in 2027. It will mark the tallest in Florida.

-

Insurance insights: Moody’s analyzes current insurance market challenges and offers some potential solutions in 2024, including leveraging the latest catastrophe models.

🏘️ MULTIFAMILY

-

Remaking Maine: The northernmost U.S. state faces an affordable housing crisis with billions in federal funds needed to renovate 7K outdated units with an average age of 47 years.

-

Resi rush: New state legislation pushes NYC landlords towards office-to-residential conversions, with SL Green (SLG) expecting 20–40MSF of conversions.

-

Reinsdorf-backed: Michigan Avenue Real Estate Group plans a 91-unit apartment building in Libertyville, a suburb of Chicago, and is seeking feedback on a prime downtown parcel.

-

Policy update: Pennsylvania House passed a tax abatement initiative to convert shopping malls into mixed-use housing developments.

-

Troubled tides: Tides Equities is facing foreclosures on three Fort Worth properties in May, amid struggles with its troubled multifamily portfolio.

-

Prolonged slowdown: The multifamily sector is seeing declining deal volumes thanks to a 17-month dry spell, with Q1 sales down 25% YoY to $20.6B.

-

On sale: Abacus Capital Group acquires a multifamily property in Sherman Oaks, LA, for $72.5 million, securing a 10.5% discount.

🏭 Industrial

-

Storage surge: The U.S. industrial outdoor storage market reported a drop in port capital inflow, but rising inland demand offers new buying opportunities.

-

Data dilemma: Growing AI demand is fueling a feverish data center frenzy, with tech firms facing major supply shortages for parts and power, creating bottlenecks worldwide.

-

At the bottom: San Diego’s industrial market shows stability despite rising vacancies at 4.6% and net absorption at -354KSF.

-

Grand gateway: Greystar completed a 1.07MSF portion of its first 1MSF+ industrial project in Mesa, AZ. Gateway Grand will be 2.1MSF upon completion.

🏬 RETAIL

-

Distressed trends: Distressed appraisal valuations are showing steep declines in retail properties, with malls and hotels seeing mixed trends while office valuations keep falling.

-

Merger meltdown: After merging, Foxtrot Market and Dom’s Kitchen will close dozens of locations and leave countless storefronts empty in Chicago, impacting local suppliers.

-

Retail reshuffle: Greenberg Gibbons acquired Cool Springs Pointe in Brentwood, TN, a fully leased retail center with high foot traffic for $34.5M.

🏢 OFFICE

-

Making Nashville move: Oracle (ORCL) relocates its HQ to Nashville, citing ties to the healthcare industry. Larry Ellison is planning a “huge campus” in Music City.

-

Auction action: Starwood Property’s (STWD) LNR Partners unit purchases 90.5KSF Hewes Building for $6.6M at auction, or around $72PSF.

-

Profitable purchase: YMP Real Estate Management bought a Miramar office portfolio at a sweet 45% discount for, coincidentally, $45M, or around $120PSF.

US HOTELS

US Hotels Report First Decline in Revenue per Available Room of the Post-Pandemic Era

In March, the U.S. hotel industry reported its first YoY decline in revenue per available room (RevPAR) since the end of the pandemic, dropping by 2.2%.

A cooling trend: The U.S. has seen a year-long decline in hotel occupancy rates, dropping 2.5% from March 2023, with weekend travel tapering off first, followed by weekday stays. Although ADRs initially helped offset these declines, their growth slowed to just 0.4% over the past year.

Diverging markets: The industry’s downturn is felt unevenly across different classes and markets. Luxury to upscale segments saw some weekday occupancy growth, contrasting with more significant losses in economy to midscale classes. Geographically, the top 25 U.S. markets fared better, benefiting from stronger corporate and group travel demand, while smaller markets struggled.

Zoom in: Notably, the top 25 U.S. hotel markets showed resilience, growing across all performance metrics with a robust 8.4% RevPAR increase in 2023. However, the smaller 147 markets struggled, with a modest 2.3% RevPAR increase and continued declines in occupancy. The success in top markets is largely attributed to stronger corporate and group travel demand, which smaller markets failed to capture.

➥ THE TAKEAWAY

Pricing challenges: As 2024 progresses, the increasing economic burden on consumers, evidenced by rising credit card debt and delinquency rates, is making travelers more selective and price-sensitive. This shift is impacting lower-tier hotels and smaller markets more significantly, challenging hoteliers to maintain pricing power amidst softening demand.

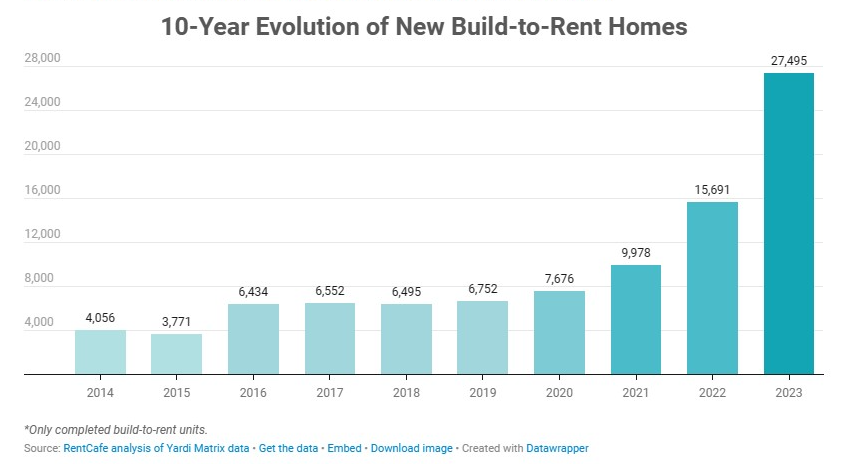

📈 CHART OF THE DAY

Over the past decade, the number of completed build-to-rent (BTR) units has gone up exponentially. With relatively little growth from 2014 to 2019, the pandemic and post-pandemic years saw a rapid rise in completion volumes, from 7,676 units in 2020 to 27,495 units in 2023, or 777.88% growth in 10 years.

You currently have 0 referrals, only 1 away from receiving B.O.T.N Multifamily Deal Screener .

What did you think of today’s newsletter? |