Q1 2026 Burns + CRE Daily Fear and Greed Index

The CRE market is inching forward, though investors remain cautious about deploying capital.

Nina Dale

March 10, 2026

Together with

Good morning. Thank you to everyone who contributed to the Q1 2026 Burns + CRE Daily Fear and Greed Index. This quarter’s report shows investors remaining cautious and largely on pause, as oversupply concerns grow and improving capital conditions have yet to translate into stronger deal activity.

Today’s issue is sponsored by InvestNext—if LP reporting means spreadsheets and constant double-checking, there’s a better way to run your workflows.

🚨Join CRE Daily + JBREC for a free webinar this Thursday, 3/12, breaking down the Q126 Fear and Greed Report. We’ll unpack what’s driving investor sentiment, where capital’s flowing, and what to watch next.

CRE Trivia 🧠

What word originally appeared at the end of the Hollywood Sign when it was built in 1923?

(Answer at the bottom of the newsletter)

Market Snapshot

|

|

||||

|

|

*Data as of 3/9/2026 market close.

Investor Sentiment

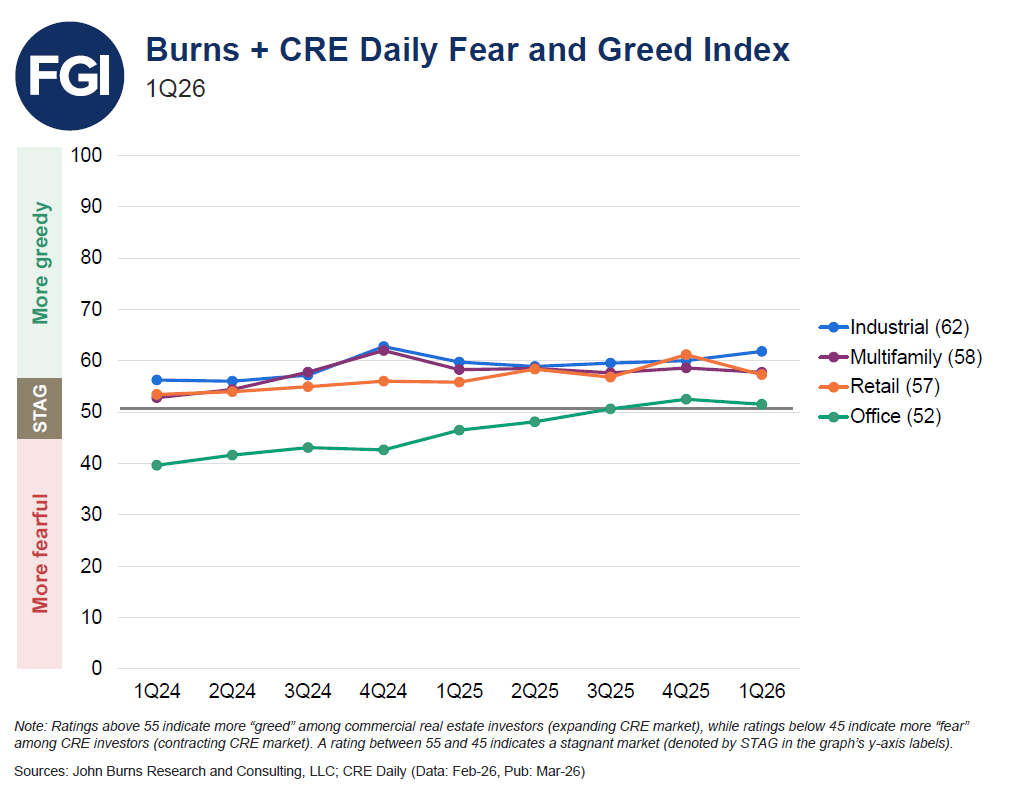

Q1 2026 Burns + CRE Daily Fear and Greed Index

The latest Q1 2026 JBREC + CRE Daily Fear and Greed Index is in, offering a fresh look at investor sentiment across 450+ sector responses.

By the numbers: The Fear & Greed Index came in at 57, signaling mild expansion but slipping slightly from last quarter’s reading. Investor activity remains subdued: 72% of investors kept their exposure unchanged in Q1, the highest share in the survey’s history. Meanwhile, just 38% plan to increase exposure over the next six months, the lowest level ever recorded.

For context: Index values below 45 indicate a contracting commercial real estate (CRE) market, while those above 55 suggest expansion. Values between 45 and 55 reflect a market that is balanced between buyers and sellers.

Sector check-in:

-

Industrial led all sectors at 62, maintaining its position as CRE’s strongest asset class.

-

Multifamily followed at 58, though investor sentiment softened amid supply concerns.

-

Retail landed at 57, supported by steady fundamentals and improving capital access.

-

Office reached 52, improving slightly but still lagging the other sectors.

Valuations mixed: Valuations diverged across property types. Multifamily values fell about 5% YoY, the steepest decline among major sectors, while office values dropped roughly 3% but showed signs of stabilizing. Meanwhile, industrial and retail values rose about 3% YoY and are expected to post modest gains ahead.

Uneven capital recovery: Capital access is improving, but unevenly across sectors. Industrial and retail investors report better conditions, while multifamily and office still face tighter financing. Still, many expect relief ahead, with more investors anticipating lower borrowing costs and Treasury yields.

➥ THE TAKEAWAY

Big picture: CRE sentiment remains cautiously positive, but conviction is thin. Investors see opportunity ahead—especially if rates fall—but for now most are staying on the sidelines, waiting for clearer signals on pricing, demand, and capital costs before putting money back to work.

Want the full breakdown? 📥Download the complete Q1 2026 Fear & Greed Index Report for sector deep dives, sentiment shifts, and exclusive investor insights.

TOGETHER WITH INVESTNEXT

You & Your LPs Deserve Better

You’ve built your firm on trust and execution.

If you are seeing any of these red flags:

-

Your most important workflows still depend on spreadsheets,

-

Constant double-checking,

-

Manual workarounds,

It is time for a better foundation.

*This is a paid advertisement. Please see the full disclosure at the bottom of the newsletter.

✍️ Editor’s Picks

-

ICSC+PROPTECH: The event created for CRE tech and marketing leaders takes place during ICSC LAS VEGAS, the world’s largest CRE event, May 18th – 20th. (sponsored)

-

Balance returning: CRE fundamentals are beginning to stabilize in 2026 as leasing improves and rent declines ease.

-

Default reckoning: PIMCO says private debt could face a broad default cycle as higher rates pressure overleveraged borrowers.

-

Capital rotation: Private credit fundraising fell nearly 50% from its early-2025 peak as capital rotated toward real estate vehicles, with Blackstone REIT raising $786M in Q3.

-

Oil paralysis: Rising oil prices are adding inflation risk and keeping developers and the Fed in a cautious wait-and-see mode.

🏘️ MULTIFAMILY

-

Enforcement ripple: Immigration enforcement could pressure distressed apartments as tenant instability complicates operations and loan performance.

-

Supply crest: LA apartment deliveries will peak in 2025 before construction drops sharply, easing supply pressure.

-

GenZ magnets: Gen Z renters and buyers are clustering in Sun Belt and Midwest metros with more attainable housing.

-

Suburban premium: Atlanta’s outer suburbs may soon cost more than the city as housing prices shift across the metro.

🏭 Industrial

-

Factory tailwind: Industrial demand could accelerate as U.S. reindustrialization drives new manufacturing and supply chain investment.

-

Megawarehouse deal: An Amazon partner signed a 1M SF warehouse lease in Chicago’s suburbs, one of the region’s largest recent industrial deals.

-

Portfolio purchase: BGO paid $270M for a 1M SF industrial portfolio, expanding its logistics footprint.

🏬 RETAIL

-

Sale signals: Whitestone REIT hired bankers after attracting takeover interest from Blackstone and TPG.

-

Discount retreat: Grocery Outlet is closing three dozen U.S. stores, marking a rare pullback among discount grocers.

-

Traffic chill: Retail foot traffic fell sharply at the end of February, signaling weaker momentum heading into an uncertain March.

🏢 OFFICE

-

Maintenance backlog: The U.S. government faces roughly $50B in deferred maintenance across its sprawling property portfolio.

-

Wynwood vision: Pitbull is planning a “Mr. 305” music-themed office building in Miami’s Wynwood district.

-

Westwood trades: Multiple Westwood deals include a land sale, Varda Space Industries’ expansion, and new leases from Bathhouse and Amoeba Records.

-

Agency conversion: A former TSA HQ in D.C. is slated for conversion as part of a slate of new local real estate deals.

🏨 HOSPITALITY

-

Miami debut: MaryAnne Gilmartin’s MAG Partners is eyeing a 1M SF mixed-use project for its Miami debut.

-

Capex climb: Rising renovation needs and brand standards are pushing hotel owners to increase capital expenditures across aging properties.

A MESSAGE FROM ARBOR REALTY TRUST

Discover Arbor's Industry-Leading CRE Insights

From in-depth reports to impactful articles, Arbor Realty Trust and Chandan Economics partner to deliver exclusive content on key trends shaping investment in commercial real estate markets, including multifamily, single-family rentals, and affordable housing.

*This is a paid advertisement. Please see the full disclosure at the bottom of the newsletter.

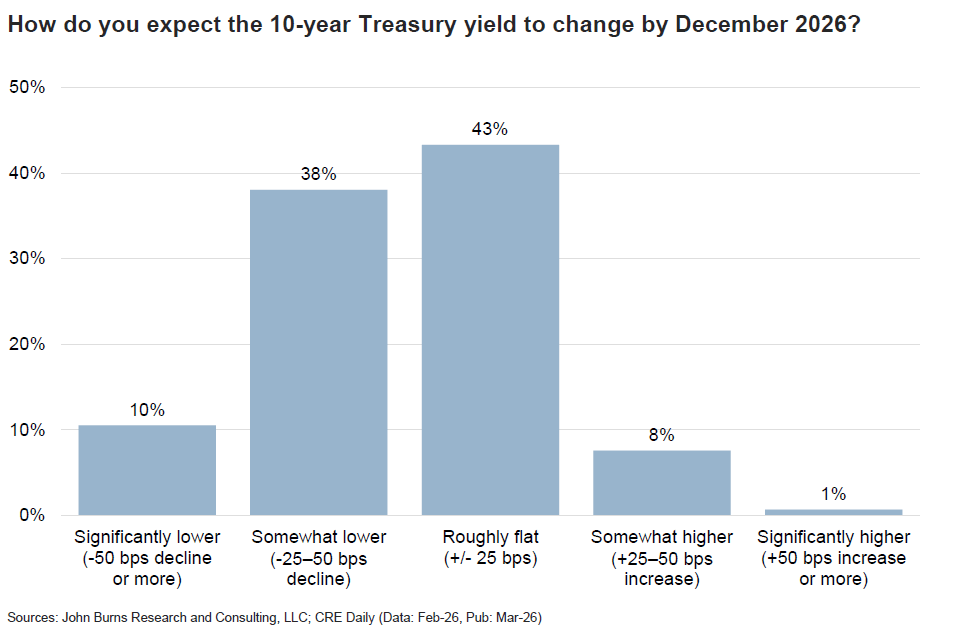

📈 CHART OF THE DAY

48% of investors expect the 10-year Treasury yield to decline at least 25 basis points by year-end 2026.

CRE Trivia (Answer)🧠

The sign originally read “Hollywoodland” to advertise a new hillside real estate development in LA.

More from CRE Daily

-

📬 Newsletters: Stay ahead of the market with local insights from CRE Daily Texas and CRE Daily New York.

-

🎙️Podcast: No Cap by CRE Daily delivers an unfiltered look at the biggest trends—and the money game behind them.

-

🗓️ CRE Events Calendar: The largest searchable calendar of commercial real estate events—filter by city or sector.

-

📊 Market Reports: A centralized hub for brokerage research and market intelligence, all in one place.

-

📈 Fear & Greed Index: A fully interactive sentiment tracker on the pulse of CRE built in partnership with John Burns Research & Consulting.

You currently have 0 referrals, only 1 away from receiving Multifamily Stress Test Model.

What did you think of today's newsletter? |